| Name | Daily Close | Daily Change | Daily Change (%) |

|---|---|---|---|

| Dow | 46,912.30 | -398.7 | -0.84% |

| S&P 500 | 6,720.32 | -75.97 | -1.12% |

| Nasdaq | 23,053.99 | -445.8 | -1.90% |

| VIX | 19.5 | 1.49 | 8.27% |

| Gold | 3,991.30 | 0.3 | 0.01% |

| Oil | 59.71 | 0.28 | 0.4 |

OVERVIEW OF THE US MARKET

Wall Street ended lower on November 6, 2025, as concerns over high valuations in tech stocks and signs of a cooling labor market rattled investors. The S&P 500 fell 1.1% to close at 6,720.32, marking its second decline in three days and pulling back from recent highs. The Nasdaq Composite dropped 1.9% to 23,053.99, hit hard by losses in AI-related names, while the Dow Jones Industrial Average shed 0.8% to 46,912.30. Nvidia led megacap declines with a 3.7% drop, Tesla also slid, and the UBS US AI Winners Index tumbled nearly 3%, underscoring the market’s heavy reliance on artificial intelligence themes that have driven much of the year’s gains.

Private sector data highlighted labor market fragility amid the ongoing government shutdown, which has delayed official economic reports. Challenger, Gray & Christmas reported 153,074 job cuts in October, the highest for that month since 2003 and nearly triple last year’s figure, driven by tech and warehousing sectors. Revelio Labs showed a net loss of 9,100 nonfarm jobs, reinforcing skepticism about hiring reacceleration. These figures amplified worries that the Federal Reserve might need to ease policy further, though comments from officials like Cleveland Fed President Beth Hammack emphasized inflation risks over employment weakness.

Corporate earnings provided mixed signals. Qualcomm delivered an upbeat forecast but disappointed investors, while Snap surged 9.7% on strong revenue and a Perplexity AI partnership. DoorDash plunged 17.5% after missing profit expectations due to higher investments, and Elf Beauty sank 35% on weak guidance. EchoStar reported a massive impairment charge, and CarMax terminated its CEO amid sales woes, sending shares down sharply. Broader market sentiment was dented by volatility, with the VIX briefly topping 20, as traders digested Fed speakers’ unease about rate cuts without fresh inflation data.

The ongoing shutdown added uncertainty, with FAA flight capacity cuts at 40 airports potentially disrupting travel and commerce. President Trump’s tariff discussions with China and drug price deals with Eli Lilly and Novo Nordisk offered some relief, slashing costs for weight-loss drugs in exchange for import duty grace periods. However, these positives were overshadowed by economic jitters. Strategists at JPMorgan noted strong retail flows could support stocks into year-end, while Morgan Stanley’s team viewed AI concerns as overblown, maintaining a bullish long-term outlook. Investors eye Nvidia’s upcoming earnings as a potential catalyst, but for now, the pullback reflects a needed reality check after AI-fueled exuberance.

OVERVIEW OF THE AUSTRALIAN MARKET

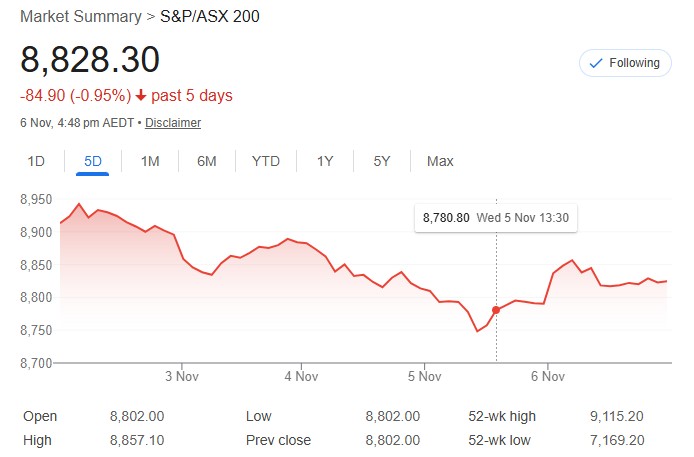

The Australian share market edged higher on November 6, 2025, snapping a two-session slide as mining stocks provided support amid commodity strength, though gains were modest amid lingering investor caution. The S&P/ASX 200 rose 0.3% to 8,827.9, while the All Ordinaries added 0.3% to 9,098.2. The index opened strongly, up nearly 70 points, but pared gains in the afternoon, reflecting uncertainty over global growth and rate paths. Resources led with a 1.4% advance, buoyed by gold miners as spot prices edged to US$3,989/oz, and iron ore giants like BHP, Rio Tinto, and Fortescue each up over 1.6% despite futures dipping to US$104.20/tonne.

Sector performance showed rotation dynamics, with Materials up 1.4% and Energy gaining 0.8% on LNG futures spiking to four-month highs, supporting Woodside and Santos. This offset weakness in high P/E areas: Information Technology fell 0.3%, Consumer Discretionary dropped 0.4%, and Financials slipped 0.1%. NAB dragged banks lower, down 3.3% after an underwhelming profit, while Westpac fell 1.2%; ANZ and CBA gained modestly. Moomoo’s Michael McCarthy noted mining strength tied to better-than-expected growth potentially averting commodity falls, amid no RBA rate cut signals.

Top performers included Light & Wonder, up 8.2% on solid earnings, and gold plays like Northern Star and Evolution amid sector bids. Caprice Resources surged 19.2% on drilling news, Toubani Resources rose 18.9% on Mali updates, and Santana Minerals gained 7.9% after a mining permit. Domino’s Pizza jumped 4.7% on debt facility commitments. Laggards featured James Hardie, down 12.7% post-MSCI index removal and merger scrutiny, Droneshield tumbling 11.7% amid defence sector froth concerns (down 50% from October highs but up 335% YTD), and Neuren Pharmaceuticals falling 10.4% despite record sales.

Trade data showed a widened September surplus to A$3.938 billion, below polls but driven by gold exports, with exports up 7.9% and imports rising 1.1%. The AUD/USD held above 0.65 at 0.651, supported by risk-on tones. Investors eye AGMs for Nine and Qantas, plus Macquarie results. Broader sentiment reflects fund flows from growth to cyclicals, with HSBC, Morgan Stanley, and UBS maintaining bullish views on earnings and AI, though tariff resolutions with the US and EU temper prior boosts.