| Name | Daily Close | Daily Change | Daily Change (%) |

|---|---|---|---|

| Dow | 44,406.36 | -422.17 | -0.94% |

| S&P 500 | 6,229.98 | -49.37 | -0.79% |

| Nasdaq | 20,412.52 | -188.59 | -0.92% |

| VIX | 17.79 | 1.41 | 8.61% |

| Gold | 3,342.30 | -0.5 | -0.01% |

| Oil | 67.68 | -0.25 | -0.37% |

OVERVIEW OF THE US MARKET

Bearish sentiment gripped stocks as escalating trade tensions and uncertainty ahead of the July 9 tariff deadline overshadowed solid economic data. Treasury yields rose, while the dollar steadied. Oil prices held steady amid ongoing Middle East ceasefire talks.

The S&P 500 fell 0.79% to 6,229.98, and the Nasdaq Composite dropped 0.92% to 20,412.52, retreating from recent highs. West Texas Intermediate crude remained around $67.27 a barrel, stabilizing after recent volatility. In after-hours trading, Tesla Inc. saw significant volume but a sharp decline, hinting at profit-taking.

Tech stocks struggled, with Nvidia slipping 0.69% despite high volume, losing ground to Microsoft in market cap rankings. The sector’s pullback reflects caution after a rapid recovery from April’s tariff-driven lows. Investors are closely monitoring trade negotiations, with Canada and the EU still in talks with the Trump administration.

Traders remain focused on Middle East developments, as the Israel-Iran ceasefire holds tenuously. Analysts suggest oil price movements will stay muted unless energy infrastructure is targeted. Federal Reserve Chair Jerome Powell’s recent comments on a cautious approach to rate cuts, amid tariff-related inflation risks, added to market jitters.

The risks to equities persist, with trade uncertainties and geopolitical tensions overshadowing resilience. The S&P 500, now 1% below its record high, faces pressure as the market digests tomorrow’s US jobs report and the tariff deadline.

OVERVIEW OF THE AUSTRALIAN MARKET

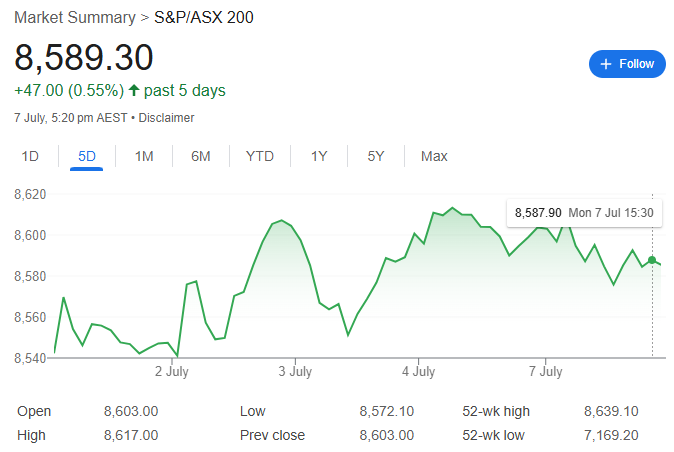

The ASX 200 closed 13 points lower (-0.16%) at 8,590, following Friday’s record close of 8,603, reflecting choppy but bullish price action. The market remains within striking distance of record highs despite consecutive down days, with tomorrow’s RBA decision as a key catalyst.

Market breadth was slightly negative, with 108 S&P/ASX 200 constituents (54%) finishing lower. Heavyweight stocks were mixed, with CBA down 0.11% and BHP off 0.34%, offset by CSL’s 2.1% gain. Utilities surged 3.5%, led by Origin Energy’s 6.5% jump after a Sky News report suggested a potential $14 billion valuation for its Kraken Technologies stake. Healthcare rose 0.9%, buoyed by CSL’s rebound from six-year lows, though no specific news drove the move.

Markets are pricing an 86% chance of a 25-basis-point RBA rate cut on Tuesday to 3.60%, with three more cuts expected by year-end. The focus is on the 1:30 PM AEST announcement, which could shift sentiment given the current proximity to record levels.