| Name | Daily Close | Daily Change | Daily Change (%) | |

|---|---|---|---|---|

| Dow | 37,645.59 | -320.01 | -0.84% | |

| S&P 500 | 4,982.77 | -79.48 | -1.57% | |

| Nasdaq | 15,267.91 | -335.35 | -2.15% | |

| VIX | 52.33 | 5.35 | 11.39% | |

| Gold | 2,996.70 | 6.5 | 0.22% | |

| Oil | 57.57 | -2.01 | -3.37% |

US MARKET

Another day and another day of massive intra-day swings. Upon open, the gap up in the S&P 500 was apparently one of the highest ever on recorded. On open, the S&P 500 had surged 4.1%, the Dow Jones 3.5%, and the Nasdaq 4%. Then the indices headed south. At the close, the S&P 500 finished down 1.6% (now in Bear Market territory), the Nasdaq 100 1.8%, and the Dow Jones Industrial Average -0.8%. All three indices were quite a bit lower but there was buying into the close.

Headlines reminding investors that the cost of Chinese imports is set to double in less than 12 hours (effective rate of 104%) seem to have put a damper on sentiment on Wall Street. On the topic of swings, the VIX ended up above 50 after dipping as low as 36.5. Regarding the dip buying, what on earth are those buyers seeing that the vast majority of other participants aren’t?? ‘Cheap valuations’? – see below. Calling Trump’s bluff? Short covering?

By definition, if markets are volatile, and volatility currently is the only known, then we can expect up and down days. Or more to point currently, up and down intra-days. Wise not to read too much into a positive day move. Because . . . . in order to make a definitive move, you need to know the end-game and the problem currently no one knows what the end-game is. But we do know volatility is here to stay. Both the Fed put (rates) and the Trump put (fiscal) have been removed. This was confirmed by Jerome Powell based on his comments on Friday and by Scott Bessent and co by comments over the weekend. So, it will partly depend on what corporate America says regarding guidance in the upcoming earnings season.

A question now is, if this volatility persists, which leveraged investment strategy blows up first.

At a stock level, and indicative of the mood, after opening strong +5.0% Apple shares closed down more than 5.0% intraday (circa a mere 10% swing on the day!!!), and on track to notch their worst four-day session since 2008. The stock appears to have gotten some downward pressure from Leavitt’s comment that Trump thinks the US has the workforce to make iPhones onshore. Analyst Dan Ives has said that making iPhones in the US would increase the price considerably — to the tune of more than $3,000 per phone — and that moving even 10% of Apple’s supply chain to the US would take at least three years and cost $30 billion. On Mag 7, Tesla is down 45% this year – worth watching in terms of Musk’s loyalty to Trump.

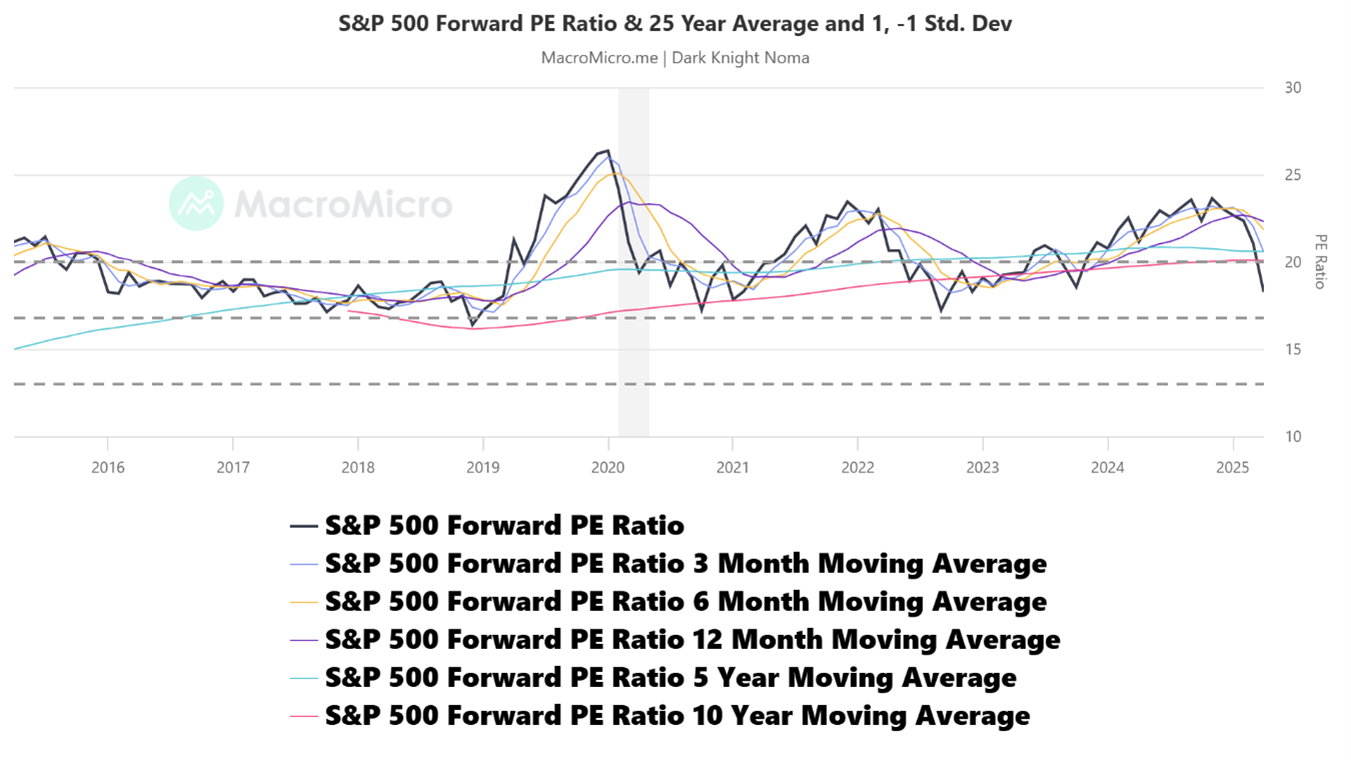

On the topic of market valuations, as at April 4 2025 the S&P 500 Forward PE Ratio was 18.3x. The chart below illustrates the S&P 500 forward PE ratio, the 25 year average, and the -1 and +1 standard deviation of. The previous Friday the forward PE ratio was 21.1x. The S&P 500 Forward PE Ratio 25 Year statistics are: 1 Std. Dev 20.04, -1 Std. Dev 13.45, Average 16.75.

The market is looking cheap, right? Not so fast. Analysts are notoriously slow in reducing earnings estimates. And if we are heading into a tariff induced recession, expect much of the next 12-months at a company level to be characterized by a raft of earnings downgrades. The market is still priced at 15% earnings growth for 2025. So, valuations are a massive risk. But maybe the upcoming earnings season will provide a catalyst. Maybe.

Figure 1: S&P 500 Forward PE ratio & 25 Year Average and 1, -1 Std. Dev

LOCAL MARKET

The S&P/ASX 200 Index rose 2.05% to close at 7,492 on Tuesday, recouping some losses from the previous session amid hopes that major trading partners could reach a deal with the US on tariffs. US Treasury Secretary Scott Bessent said that almost 70 countries, including Japan, have contacted the White House to negotiate tariffs. However, volatility is expected to remain high as Trump threatened China with another 50% tariff on top of existing levies if Beijing does not lift its duties on US imports.

Nine of 11 sectors were in the green, led by technology and healthcare. Buying in index bellwethers Commonwealth Bank and BHP pushed the bourse higher, with the stocks up 1.3% and 1.5%. Mining stocks led the rebound, with notable gains from BHP Group, Fortescue (1.9%), and Northern Star Resources (1.1%). Consumer, technology and financial stocks also advanced, including Wesfarmers (1.7%), Wisetech Global (2.4%), and Macquarie Group (2.4%).

On the topic of commodities, Wall Street investment banks have urged traders to resist the pull of cheaper commodities. Citi strategists have told clients that the increasing likelihood of a recession in the world’s largest economy and a broader global slowdown will hurt oil and base metals – such as copper, aluminium and nickel – and for the longer term. They say any rally this week is an opportunity to sell. All commodities have slumped recently but copper, which is viewed as a barometer for the global economy, has also suffered a violent reversal, with US prices collapsing 20 per cent from its record high in late March, satisfying the definition of a bear market.

The two key Australian sentiment surveys were released on Tuesday.

Confidence among Australian consumers has hit a six-month low after the US’ punitive and wide-ranging tariffs caused a global stock market meltdown, according to the Westpac Consumer Sentiment Index report on Tuesday. The index, which measures confidence compiled from surveying consumers about family finances, the economy and home buying, plunged 6%, down from 95.9 in March, to 90.1 in April. Sentiment was around 10% lower among those surveyed after the US announced its 10% tariff on all nations and reciprocal tariffs on around 60 countries, compared to those surveyed before the announcement. With the situation still deteriorating, there is a clear risk of more significant sentiment declines in the months ahead.

The NAB Monthly Business Survey indicated business conditions were largely unchanged in March and remain a little below average. An uptick in profitability in the month was mostly offset by slightly lower trading conditions and employment. Confidence eased slightly and remains in negative territory. Elsewhere, most survey measures were fairly steady, including price pressures. The survey was taken prior to the significant shift in US trade policy announced in early April, and as such, does not reflect firms’ perceptions of the outlook post tariff. So take the confidence feedback with a massive grain of salt.