By guest contributor Ken Atchison, founder of Atchison Consultants

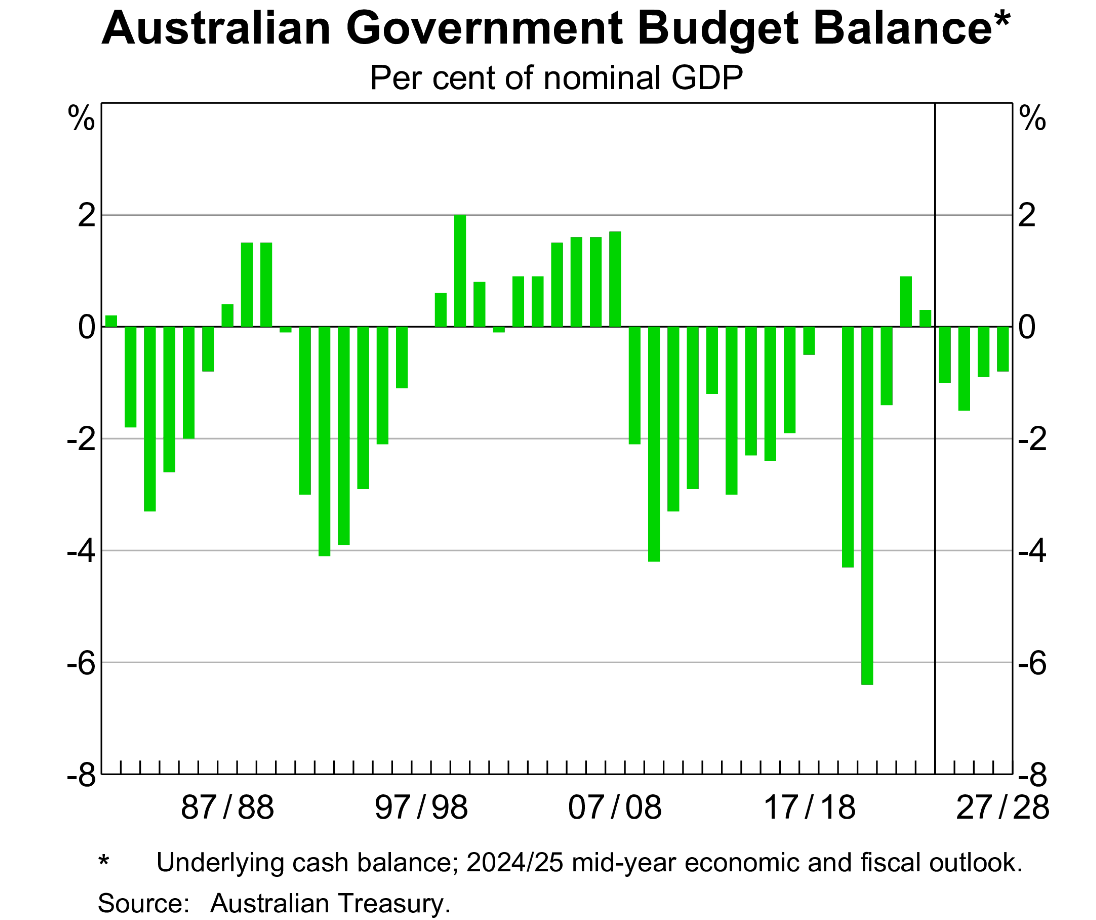

Under the Australian Government elected in 2022, two years of budget surplus were delivered. However, in the future a return to budget deficits is expected as shown in the chart below. This is occurring during a sustained growing economy, so it is not driven by the stabilisers in the budget from items such as unemployment benefits. Rather it is a policy of spending to resolve any policy issue which arises. Also, a very significant increase in public service employment and pay has emerged.

High inflation and high long-term interest rates in Australia are the likely outcome.

Spending other people’s money is the political mindset. At the state level, Victoria is perhaps the most egregious example. Victorian government politicians now believe the rest of Australia, not just Victorians, should pay for their incompetence. Treasurer Pallas has stated “It is wrong that we constantly are the milking cow of the federation. We are constantly subsidising poor-performing states”. This is a sentiment which may be shared by other state treasurers. Factually, it is not correct and is more likely a political plea.

Services which Victorian residents expect from the state government include education, roads, health, transport, judiciary, police and fire services. Delivery of these services is being slashed due to financial strain in the state, a consequence of the lack of competent financial management under the Andrews and Allan governments.

Credit rating downgrades are meaningful. They are the public assessment of the incompetence of state government. Moody’s concluded that Victoria, uniquely in Australia, has a negative outlook which means future living standards are at risk. Former premier Andrews shrugged off concerns from major ratings agencies that rising debt could imperil the Victorian credit rating. Current premier Allan, as far as we know, has the same view as her predecessor.

Queensland is also showing signs of severe state financial strains. There are fewer federal ALP seats of parliament in the state, but the new Queensland government will no doubt pursue any handouts from the federal government if Victorian pleas are successful.

National consequences will be even more severe. Already the Victorian Government is pleading for financial assistance from the national government. With the ALP holding 24 of 39 Victorian federal seats, they will almost certainly promise and perhaps deliver financial support for Victoria. While the Federal Government has no direct responsibility for state financial management, credit assessment of Australia by ratings agencies will take into account the financial status of the states.

The cavalier approach to spending by the Victorian Government is increasingly evident in the Federal Government. Spending has been applied by the Albanese government whenever any issue of substance arises. Accountability for policy is increasingly absent from the national government regarding actions it has taken. This same policy has been adopted in Victoria for the past decade.

Infrastructure Australia reports that significant levels of public investment in priority growth areas such as energy, housing, heavy industry and defence will compete for access to human resources. A labour supply shortage in multiple sectors will increase inflation. It is evident that the Federal Government is following the Victorian government into the financial mismanagement quagmire.

All this spending by state and the federal governments requires funding by increased debt. It is constantly adding to the debt burden on future generations. Living standards for Victorian residents are being reduced. It is possible that this will also occur in Queensland. Of greater concern is that this will occur nationally.

Growing public sector debt in Australia will coincide with rising inflation overseas as a result of government stimulus in the US and China and easy monetary policy in both major economies. Higher short-term interest rates set by the Reserve Bank of Australia will be necessary to contain inflation.

In a global environment where easy monetary policy and significant government spending is occurring in the US and China, inflation will grow. This will prompt higher long-term government bond interest rates. Long-term government bonds at current interest rates are unlikely to be sufficiently rewarding as a premium above inflation will be demanded. Australia will be poorly prepared for this outcome with rising debt and higher interest rate costs unless something changes.