Westpac’s New York office recently expanded a previous study of US dollar behaviour around previous Federal Reserve tightening cycles, such as the one the US is expected to experience shortly, into a study looking at various asset classes, including 10 year bonds.

Their conclusion? Previous Fed tightening cycles have been “innocuous”, that is, harmless, for major asset classes. The US dollar, in trade-weighted index terms, “stalls” on average, US equities consolidate, US investment-grade credit spreads typically shrink and commodity prices increase.

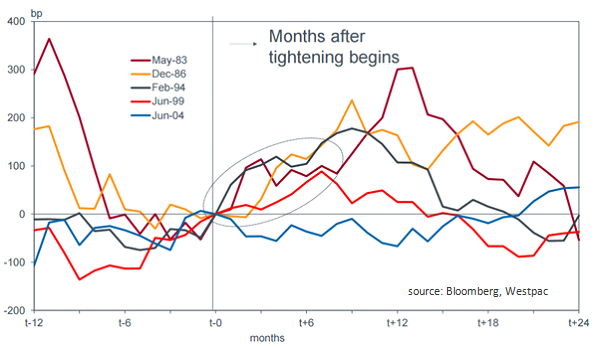

The one exception is in US 10 year bond yields. Readers will see from the diagram below how 10 year bond yields have in the past typically increased in the first six-to-nine months after the commencement of the tightening cycle. The period after 2004 was an exception but, as readers will recall, that ended rather badly. With this mind, Westpac wonders “how Chair Yellen can pull off a “dovish” inaugural hike”, especially when the “infamous”, as Westpac describes them, dot plot interest rate projection indicate Fed members think there will be four lots of 25bps increases in 2016.

Back in September, YieldReport published a short article on “Why US rates are important to Australian bond investors?” What happens in the US tends to end up happening in Australia and that is certainly true when it comes to bond yields. When US short term yields rise, US long term yields will probably follow, as will Australian 10 year yields, although some lag is to be expected.