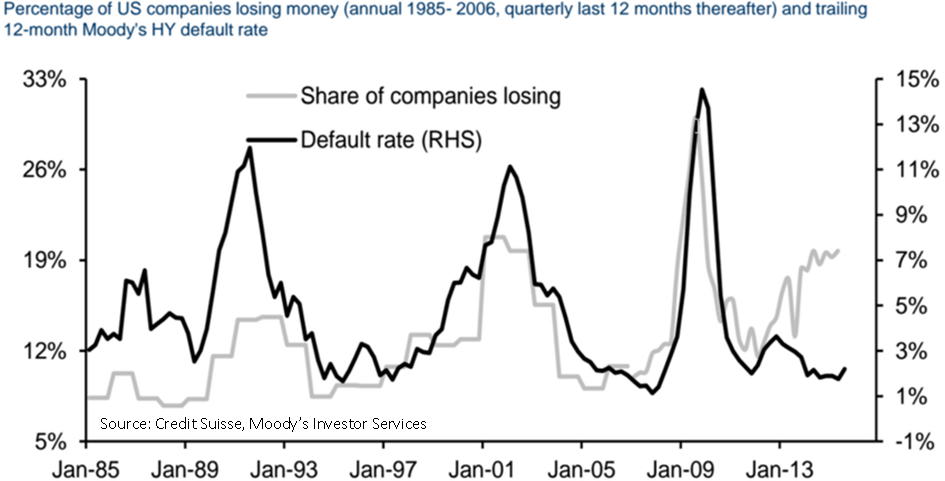

An interesting chart from Credit Suisse in the US looks at the percentage of companies losing money and overlaying this data with the rate of credit defaults. Logic would suggest that there is a strong correlation between these two metrics and the chart essentially shows that. Except for the last two years.

There is presently a very low level of credit defaults in the US and that could be sheeted home to record low interest rates and a slowly improving economy. With credit markets very liquid, companies have been able to tap credit markets to refinance debt at more favourable levels.

What will happen when this liquidity dries up or when the US Fed raises interest rates?

Presently, the majority of the market is of the view that the Fed will raise rates in December. A strong US employment number for October and multiple commentaries from Fed officials suggest that the Fed is keen to move the US economy away from near zero interest rates sooner rather than later. While any rise is likely to be largely symbolic and shallower than previous rate hike cycles – that is, rate rises will occur more slowly than in past cycles – any rate rise could well trigger a rise in credit defaults.

Defaults are close to 30 year lows and debt levels are high. A small interest rate rise might well trigger stress amongst corporate debt holders that might eventually create a flow-on effect in relation to defaults.

The message seems clear; companies should get their debt house in order and prepare for higher rates, while investors should take the opportunity to review their investment portfolios to stress test against higher default rates.

SHARE OF COMPANIES LOSING MONEY POINTS TO HIGHER DEFAULTS?