Australian super funds need to focus in relation to their foreign currency exposure to help mitigate losses from Trump’s trade agenda. Australian super funds currently have an estimated $379 billion invested in overseas shares, of which around 20% is hedged against the US dollar. It used to be 35% a couple of years ago. Temporary phenomenon or a more permanent shift is really the question. Since April 2 the USD/AUD swing has been -10%, clearly adversely impacting US holdings unless hedged.

NAB forecasts the AUD to climb to US70¢ by year-end. Westpac estimates that a 10-percentage point increase in hedging ratios to 30% would add $100 billion in Australian dollar demand. If that happens over five years, the impact is not that much, but if it happens in 18 months, it’s a different story.

As we know May saw widespread gains against the dollar, with the USD falling below key technical levels across multiple pairs. The Taiwan Dollar’s 8.4% surge stood out, but strength was broad, fuelling speculation about a deliberate US devaluation—dubbed a potential “Mar-a-Lago Accord.” Yet today’s dollar plays a different role than during the Plaza Accord era: a large share of US assets is held by foreign investors, who would suffer from sustained dollar weakness, creating destabilizing feedback loops.

Preserving dollar hegemony outweighs trade deficit concerns. Major currency gains hurt foreign holders of US assets via portfolio losses, discouraging future dollar exposure. If the US signalled sustained depreciation, global demand for dollar assets would erode—undermining its financial dominance instead of improving trade balances.

Since April 2’s extreme reciprocal tariffs, the dollar experienced massive outflows creating a rare “triple kill” in stocks, currencies, and bonds. Trump’s renewed threats—50% EU tariffs starting June 1 and 25% on non-US iPhones—pushed the dollar back below 100 despite May agreements with the UK and China. This mirrors 2018-2019 trade war volatility, making short-term confidence restoration nearly impossible.

Combined net speculative long positions in the dollar and euro hedges have collapsed to early 2024 levels, with the dollar twice breaching the critical 100-level since April. Asian rush exports in H1 further pressure dollar demand while market positioning data reveals underlying sentiment remains structurally damaged by policy uncertainty.

Unlike 1985’s Plaza Accord, current dollar holdings are highly diversified, requiring Chinese cooperation despite reduced US export reliance and strategic competitor status. China’s PBOC maintains RMB weakness intentionally, making active collaboration with US dollar depreciation virtually impossible—eliminating the critical partner needed for coordinated intervention.

Deliberate dollar depreciation would reduce overseas willingness to hold dollar assets, undermining America’s fundamental advantage—dollar hegemony. This strategic imperative explains why policy-driven depreciation remains unviable, as maintaining reserve currency status takes priority over trade balance improvements, supporting H2 dollar stabilization expectations.

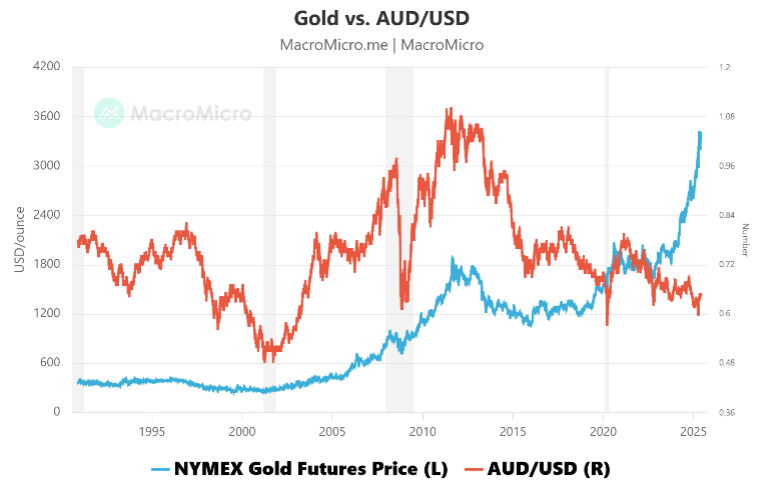

In relation to Figure 2 below, Australia is the 2nd largest producer of gold and the 6th exporter of gold. Gold accounts for 6% of Australia’s overall exports. Historically, AUD and gold price have a correlation coefficient of 0.77 which shows high correlation.

-

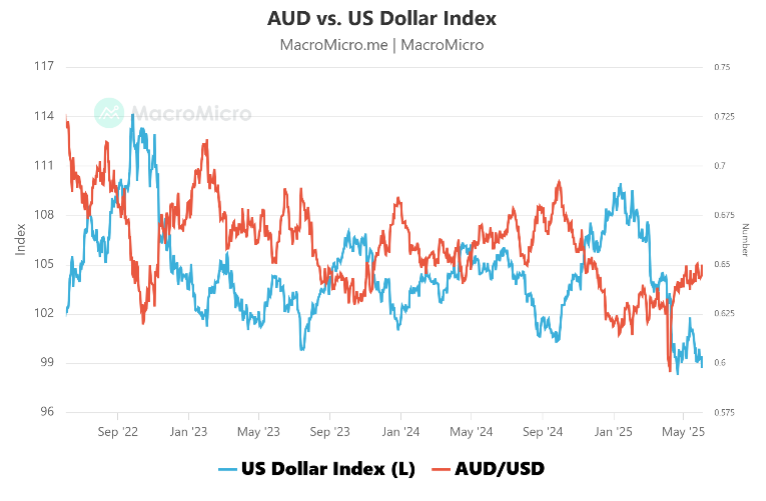

- Figure 7: AUD vs. US Dollar Index

-

- Figure 8: Gold vs. AUD/USD

About YieldReport – Your Income Advantage

YieldReport is Australia’s leading online data and research platform for interest rate markets, securities and products that focus on fixed income and yield generation. YieldReport provides advice, news review, analysis and insights on what’s shaping the yield curve and fixed income markets. It also provides a great source of reference for pricing and performance data on yield-generating investment opportunities, including cash, term deposits, government and semi-government bonds, managed funds, ETFs, corporate bonds, floating rate notes, hybrids as well as other yield instruments. YieldReport insights and analyses are designed to help anyone managing money, whether it be their own or whether they sit on a finance committee, board etc. – to make informed decisions about where interest rates are going and to have access to the best rates and latest performance data available.

Explore more via the website – www.yieldreport.com.au.

Find daily updates on social media platforms such as LinkedIn and Twitter.

For inquiries, please contact contact@yieldreport.com.au or call 0408 266 713.