Summary: GDP up 3.3% in September quarter; better than expected; result “a positive surprise to authorities”; economy still 3.9% smaller than September 2019; “too early to say economy is out of recession”; bounce in consumer spending main driver; “significant upward revision” to RBA’s 2020 growth forecast likely; Westpac chief economist expects consumer spending to be “strong” in December quarter.

Since the “recession we had to have” as the recession of 1990/91 became known, Australia’s GDP growth has been consistently positive, with only the odd negative quarter here and there. However, Australia’s first recession in nearly thirty years was inevitable once governments introduced restrictions which shut businesses and limited people’s movements for an extended period of time. A return to growth was widely expected once restrictions were eased across much of the country.

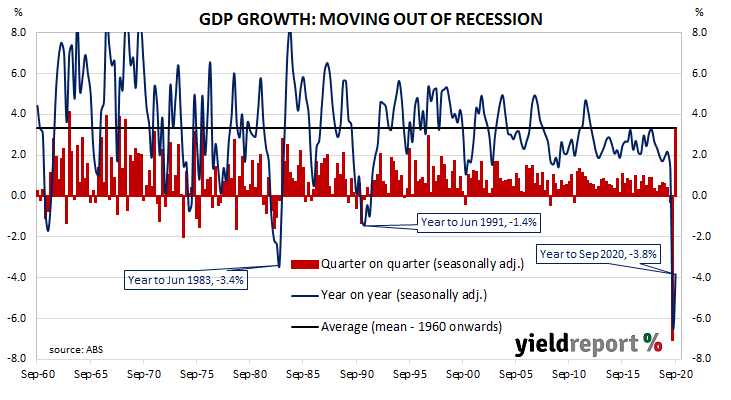

Figures released by the ABS indicate GDP expanded by 3.3% over the September quarter. It was a better result than the 2.4% rise which had been generally expected and in contrast with the June quarter’s -7.0%. However, on an annual basis, GDP still contracted by 3.8%, although this was better than the June quarter’s comparable figure of -6.4% after revisions.

“This result will come as a positive surprise to the authorities,” said Westpac chief economist Bill Evans.

Longer-term Commonwealth bond yields rose noticeably on the day but not as much as their US Treasury counterparts had overnight after news a vaccine and a federal spending package may be closer than previously thought. By the end of the day, 10-year and 20-year ACGB yields had each gained 6bps to 0.98% and 1.62% respectively. The 3-year yield finished 1bp higher at 0.18%, 10bps above the RBA’s target rate.

Longer-term Commonwealth bond yields rose noticeably on the day but not as much as their US Treasury counterparts had overnight after news a vaccine and a federal spending package may be closer than previously thought. By the end of the day, 10-year and 20-year ACGB yields had each gained 6bps to 0.98% and 1.62% respectively. The 3-year yield finished 1bp higher at 0.18%, 10bps above the RBA’s target rate.

ANZ senior economist Felicity Emmett noted September’s GDP figure “still leaves the economy 4.2% smaller than it was prior to the pandemic and 3.9% smaller than a year ago.” She said “it is too early to say the economy is out of recession”, especially when the employment under-utilisation rate was 17.4% at the end of October.

A 7.9% bounce in household spending was the obvious driver of the result, contributing 4.0% to the total increase for the quarter and dwarfing the influences of all other sectors. Imports for the quarter increased but exports fell, subtracting around 1.9%. A smaller reduction in the September quarter inventories added around 0.8%.