Overview

Gold futures have decisively broken prior records, surging past US$3,400 per ounce and extending year-to-date gains beyond 25% as escalating US-China trade tensions and anxieties over reciprocal tariffs ripple through markets. Recent events, such as major corporate warnings (e.g., Nvidia’s $5B potential hit), act as potent catalysts, accelerating the flight to perceived safety and driving gold significantly higher.

This rally reflects a fundamental shift in investor sentiment and positioning, evidenced by Bank of America’s latest survey identifying “long gold” as the most crowded trade (49% respondents)—a title held by tech stocks for two years prior. This conviction is substantiated by robust and sustained inflows into global Gold ETFs since Q1, indicating broad-based demand as investors and central banks actively seek portfolio protection.

Cracks in Confidence? US Treasuries face Scrutiny as Safe Haven

The traditional role of US Treasuries as the primary safe haven has been challenged during recent stress periods, marked by sharp yield spikes (10-year yield previously pushed above 4.5%) occurring even amidst equity downturns. Analyses points to forced deleveraging of highly leveraged basis trades (involving over $800B in net short futures) as the main technical driver behind these dislocations, rather than a fundamental abandonment by major foreign creditors.

Beyond technical pressures, the long-term sustainability of US fiscal policy is increasingly scrutinized, potentially eroding Treasury appeal to marginal buyers. With significant projected deficits adding to the existing debt burden, the critical relationship between Treasury yields (‘r’) and economic growth (‘g’) comes into focus. A scenario where interest costs persistently outpace growth (r > g) signals a heavier debt servicing load, raising fundamental questions about the ultra-safe status of Treasuries for long-term holders compared to real assets like gold.

Official Sector & Institutional Flows Propel Gold Demand

A powerful, structural tailwind for gold comes from consistent net purchases by global central banks, especially within emerging markets seeking to diversify reserves beyond the US dollar and insulate against geopolitical shocks. Steady accumulation by countries like China, India and notable increases elsewhere (e.g., Poland’s +90 tons in 2024) underscore gold’s re-emerging role as a core reserve asset, providing a solid demand floor.

Institutional investors are increasingly adopting this view, allocating strategically to gold as a vital hedge against persistent inflation, geopolitical flare-ups, and potential weakness in traditional financial assets. This shift is driven by factors like low or negative real interest rates, which reduce the opportunity cost of holding non-yielding gold, making it a compelling diversifier in current portfolios.

Gold Reserves Rise as US Debt Held Overseas Falls

The confluence of enduring geopolitical uncertainty, ongoing central bank demand for diversification, and investors actively seeking portfolio insurance paints a constructive backdrop for gold. With global allocations to gold still arguably below historical peaks (e.g., US Gold ETF AUM ~1.6% vs. 7.6% in 2011) and many anticipating it as a top 2025 performer (42% in BofA survey), the strategic case for holding gold appears intact.

Despite the bullish narrative, potential risks loom. Extreme price appreciation could eventually stifle demand or incite large-scale profit-taking. Moreover, a severe financial market liquidity squeeze—a growing concern amidst heightened volatility—could force distressed selling of liquid assets, including gold, regardless of fundamentals. A significant de-escalation in global trade tensions would also naturally reduce its immediate safe-haven appeal.

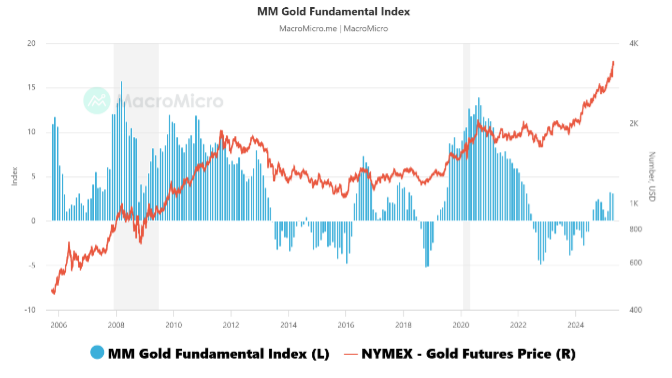

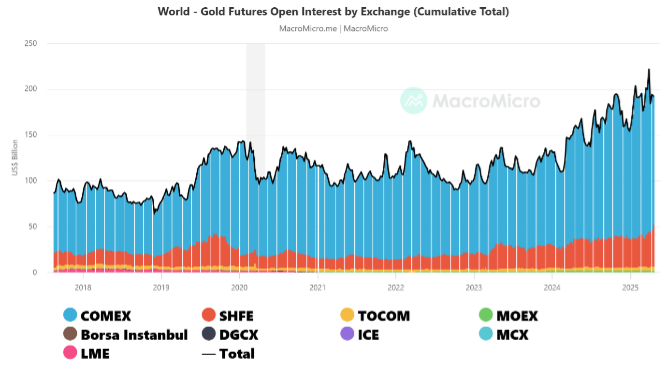

Figure 1: Gold Fundamental Index. Figure 2: World Gold Futures Open Interest

With reference to Figure 1, the MM Fundamental Index for gold is an integral index for gold futures fundamentals. When the index goes up, it means the fundamentals of the gold market are looking good. Components of the MM Gold Fundamental Index include the real interest rate in the US, FedWatch rate hike/cut probability, the Gold COT Index, etc. The weight of each component is adjusted according to the latest gold market conditions.

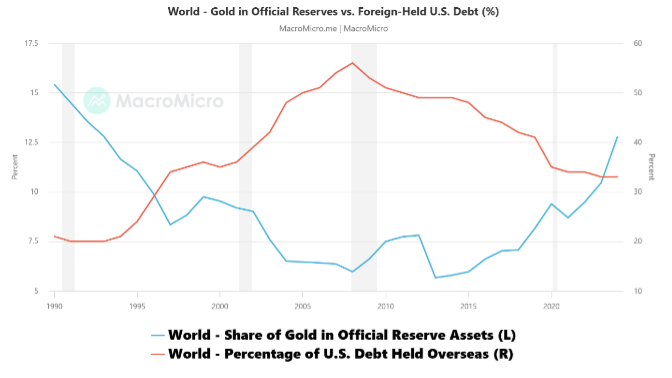

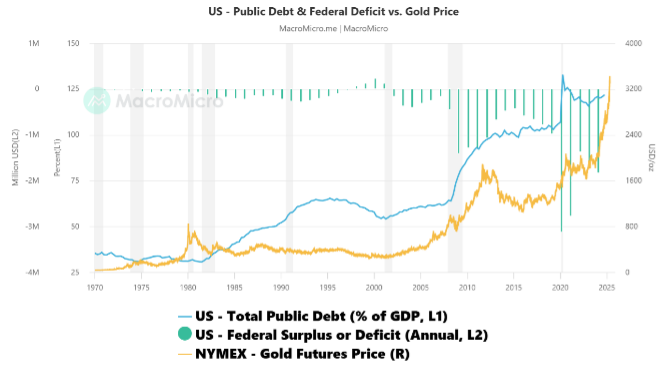

Figure 3: Share of Gold in Official Reserves Figure 4: US Public Debt & Fed Deficit vs Gold

With reference to Figure 3, this chart shows the changing trend of the proportion of gold held by global central banks in official reserve assets (blue line) and the proportion of US Treasury bonds held overseas (red line). Since the 1990s, with the advancement of globalization and the establishment of US dollar hegemony, the proportion of U.S. debt held overseas has increased rapidly, while the proportion of gold reserves has dropped significantly. However, after the 2010s, with events such as China’s promotion of the “Belt and Road Initiative”, Brexit, the US-China trade war and the Russia-Ukraine conflict, the trend of de-dollarization of the global economy has become increasingly apparent, the proportion of gold reserves has rebounded, and the proportion of US debt holdings has tended to decline. Especially in recent years, the Russia-Ukraine war and the escalation of geopolitical risks have accelerated central banks around the world to increase their gold reserves to reduce their dependence on the US dollar, reflecting the structural changes in the international financial system and the shift in risk aversion demand.

With reference to Figure 4, the US Dollar Index (DXY) is inversely proportional to the price of gold. One of the key factors affecting the trend of the dollar is the market for credit and solvency of the US government, which depends on the growth of public debt relative to the economy, as well as the size of the fiscal deficit/surplus. When the US government’s public debt as a share of GDP and fiscal deficit rise, the market will question the credit and solvency of the US, which tends to weaken the dollar and strengthen gold. Conversely, when US public debt as a share of GDP and fiscal deficit decline rapidly, the market has more confidence in US credit and debt repayment ability, which would strengthen the dollar and weaken gold.

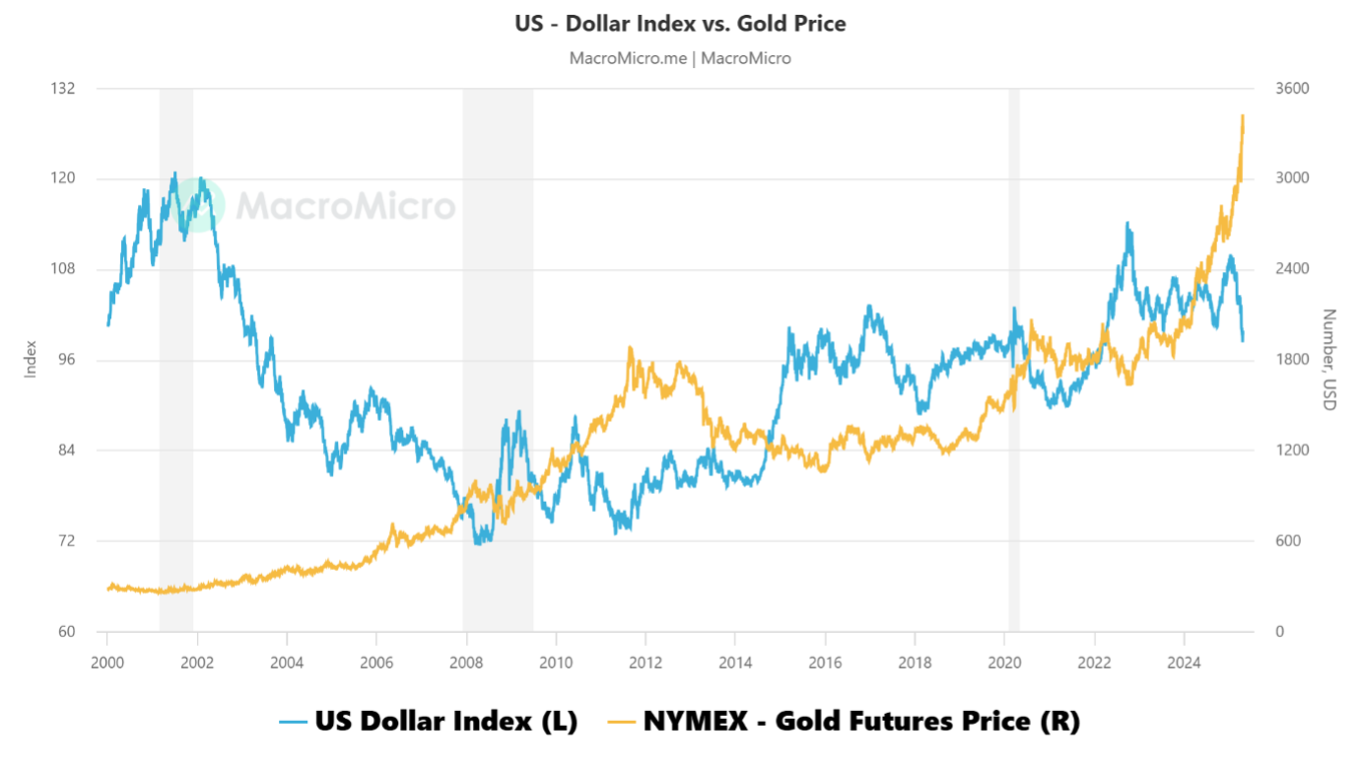

| Figure 5: US Dollar Index vs Gold Price |

With reference to Figure 5, the US Dollar Index (DXY) and gold prices share a negative correlation for two reasons: 1. Gold is USD denominated. When the US dollar appreciates, gold costs more for investors using other currencies. Demand for gold thus decreases, putting downward pressure on gold prices. 2. To some level, gold and USD are substitutes, because they are both used as an international reserve and hedging tool. When the USD strengthens, demand for gold declines.