INVESTMENT BASICS – DURATION by PIMCO

What is duration?

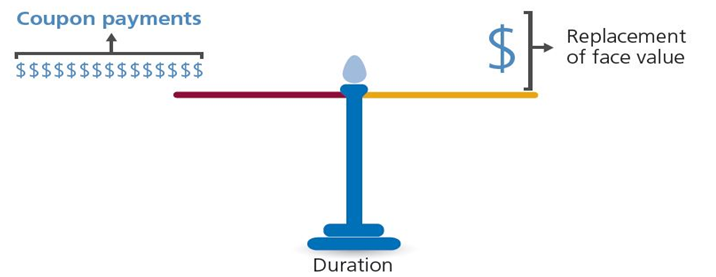

Duration is the most commonly used measure of risk in bond investing. Duration incorporates a bond’s yield, coupon, maturity and call features into one number, expressed in years, that indicates how price-sensitive a bond or portfolio is to changes in interest rates. There are a number of ways to calculate duration, but the term generally refers to effective duration, defined as the approximate percentage change in price for a 100bps change in yield. For example, the price of a bond with an effective duration of two years will rise (fall) 2% for every 1% decrease (increase) in yield, and the price of a five-year duration bond will rise (fall) 5% for a 1% decrease (increase) in rates. The longer the duration, the more sensitive a bond is to changes in interest rates.