By Chris Owens, analyst, Atchison Consultants

Australian real estate investment trusts (AREITs), as represented by the S&P/ASX 200 AREIT Index, returned +5.3% in the month ending 30 April 2023. AREITs outperformed the S&P/ASX 200 return of -0.2% over the month.

Over the 12 months to April 2023, AREITs posted a total return of -9.9%, underperforming the S&P/ASX 200 return of +2.8%.

Sector Performance

Table 1 – S&P/ASX 200 AREIT Accumulation Index Performance: Total Returns (30 April 2023)

Over the 3 years and 5 years to the end of April, the sector produced total returns of 10.7% and 4.9% per annum respectively.

The Industrial segment again was the best performer after it returned 3.4%. Diversified AREITs returned 3.3%, Office AREITs returned 2.6% and Retail A-REITs returned 1.0%.

Table 2 – S&P/ASX 200 AREIT Accumulation Index Performance: Income Returns (30 April 2023)

The income component of the total return was 4.4% for the 12-month period to April. Annual volatility of income returns was 1.8%, which is low when compared with other asset classes.

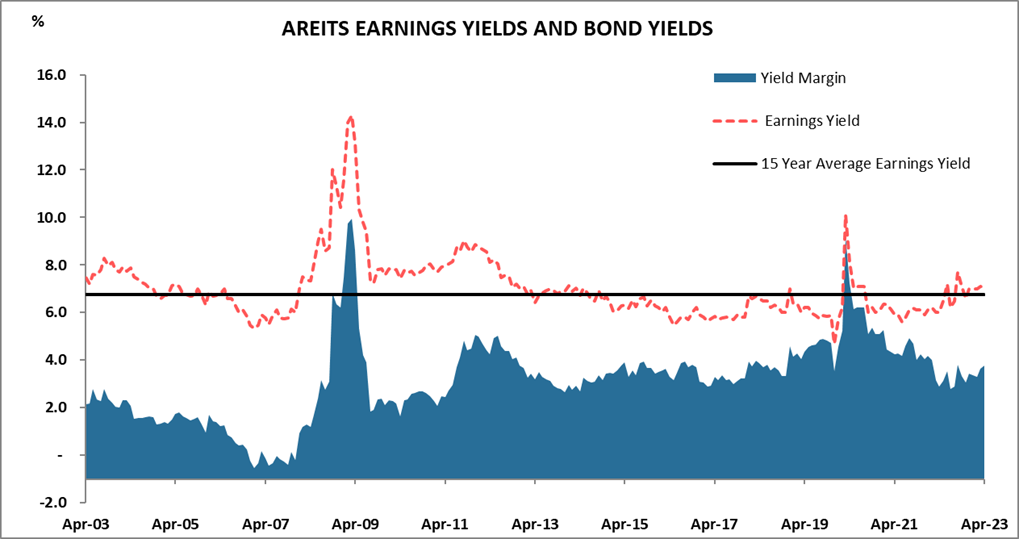

AREITs were trading at an earnings yield of approximately 7.0% at the end of the month, higher than yields of both cash and Commonwealth Government bonds. The spread of the earnings yield over the 10-year government bond yield remained unchanged at 3.8%.

Changes over time of the spread between the earnings yield of AREITs and the 10-year government bond yield are shown in Chart 1.

Market Review

The market for neighbourhood malls has experienced a resurgence as Coles and Woolworths have successfully sold properties worth $161 million in Sydney, Melbourne, and southeast Queensland. This signifies a fresh consensus in valuations, as prices are adjusted in response to rising rates.

These deals mark a breakthrough in a market where few convenience retail assets of significant size have been traded in the past 18 months. Vendors had been hesitant to adjust their price expectations despite the steep increase in borrowing costs. The sales were made at an average capitalization rate of approximately 5.5%, establishing new pricing benchmarks for this highly sought-after asset class. These rates align with the adjustments made by prominent convenience mall landlords, Region Group and Charter Retail REIT, who collectively own nearly $9 billion worth of supermarket-anchored properties.

In February, Region Group raised its weighted average capitalization rates by 23 basis points to 5.67% to reflect declining valuations. Similarly, the Charter Hall fund increased its cap rates by 7 basis points to 5.52%.

For the supermarket giants, selling newly-developed malls through their property arms, complete with long leases, has been a means to inject funds into their operating businesses and supply chains. This includes the development of state-of-the-art automated distribution centres. Woolworths has spearheaded this trend, successfully finding buyers for three neighbourhood centres in southeast Queensland and Melbourne, resulting in total sales of $108 million.