By Jeremy Jiang, Property Analyst, Atchison Consulting

Australian real estate investment trusts (AREITs), as represented by the S&P/ASX 200 REITs Index, returned 2.6% in July, underperforming the S&P/ASX 200’s return of 2.9% over the month.

Over the 12 months to July 2019, AREITs posted an impressive total return of 21.2%, which was 7.9% higher than the S&P/ASX 200 (13.3%). One of the forces responsible for this return was a fall in market interest rates. On 2nd July, RBA Governor Lowe announced the cash rate been cut by 25 basis points to a new record low 1.00%, after cutting 25bps in the previous month to 1.25%. The RBA cited their decision to cut was to “support employment growth and provide greater confidence that inflation will be consistent with the medium-term target”. In a speech on July 25, RBA Governor Lowe noted “the board is prepared to provide additional support by easing monetary policy further, it is reasonable to expect an extended period of low interest rates”. The Australian 10-year government bond yield fell 14bps from 1.35% to 1.21% over the month. Compared to the same time in 2018, the Australian 10-year government bond yield has decreased by 147bps.

AREIT prices appreciated strongly as bond yields fell but, in doing so, they have “overshot” and a gap has opened up between prices and valuations. This is a result of lower bond yields being viewed as positive for underlying property valuations.

At the end of July, AREIT sectors were trading on a 54.8% premium to net tangible assets (NTA) on an index-weighted basis. This measure implies the sector is expensive, with a limited upside in asset valuations remaining in this cycle. However, AREITs’ earnings yields continued to be attractive relative to interest rates.

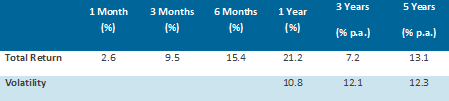

Sector Performance

Table 1 below shows the performance of the AREIT sector for various periods ending 31 July 2019.

Table 1

Source: S&P/ASX 200 AREIT Accumulation Index (2019)