By Chris Owens, analyst, Atchison Consultants

Australian real estate investment trusts (AREITs), as represented by the S&P/ASX 200 AREIT Index, returned -8.7% in the month ending 31 May 2022. AREITs underperformed the S&P/ASX 200 return of -2.6% over the month.

Over the 12 months to May 2022, AREITs posted a total return of 3.3%, underperforming the S&P/ASX 200 return of 4.8%

Sector Performance

Table 1 below shows the performance of AREITs for various periods ending 31 May 2022.

Over the 3 years and 5 years to the end of May, the sector produced total returns of 2.5% and 5.7% per annum respectively.

Sector return falls were led by Industrial AREITs at -14.3%, followed by Diversified AREITs at -8.1%, Office AREITs at -6.3% and Retail AREITs at -3.5%.

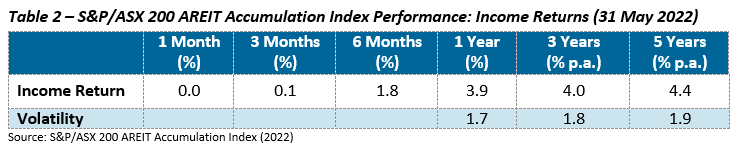

Table 2 below shows the income performance of AREITs for various periods ending 31 May 2022.

The income component of the total return was 3.9% for the 12-month period to May. Annual volatility of income returns was 1.7%, which is low when compared with other asset classes.

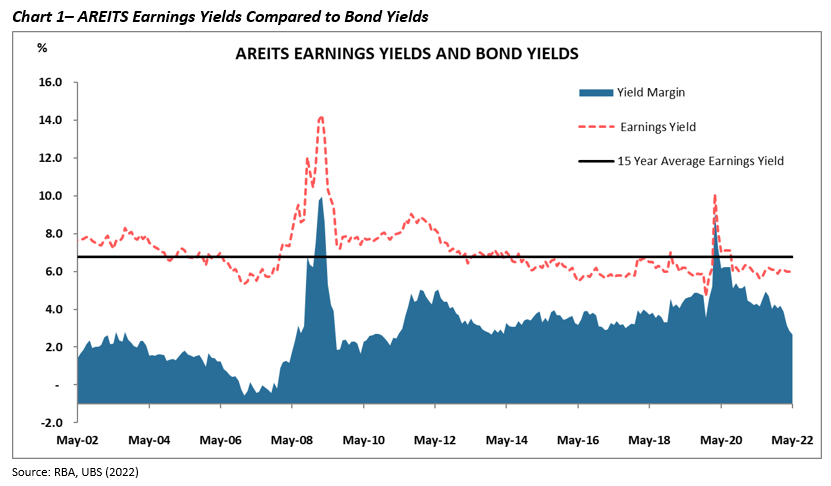

AREITs were trading at an earnings yield of approximately 6.0% at the end of the month, higher than yields of both cash and Commonwealth Government bonds. However, the spread of the earnings yield over the 10-year government bond yield fell from 2.9% to 2.7% as bond yields rose substantially.

Changes over time of the spread between the earnings yield of AREITs and the 10-year government bond yield are shown in Chart 1.

Market Review

The AREIT 200 index is currently down 25% year to date. On average UBS has sliced its price targets on Australian property stocks by 15%, arguing that the AREIT sector has never been more exposed to interest rate rises.

UBS lays its concerns with low debt hedging levels, increasing costs of capital and residential property exposures. The investment bank is forecasting debt costs to exceed 6% by 2026. This would take interest coverage ratios (ICR) for AREITs to 3.2 times and push several AREITs below 3 times. The sector now averages an ICR of 5.6 times. To increase ICRs, UBS is forecasting $3.5 billion in asset sales and has cut the sector forecast earnings by 5% over the next four years.

Mirvac and Stockland carry residential property exposures that will likely moderate with increased interest rates. UBS is forecasting Mirvac and Stockland stocks to fall 7% to 8% in 2024 due to lower sales volumes.