By Chris Owens, analyst, Atchison Consultants

Australian real estate investment trusts (AREITs), as represented by the S&P/ASX 200 AREIT Index, returned -13.6% in the month ending 30 September 2022. AREITs underperformed the S&P/ASX 200 return of -6.2% over the month.

Over the 12 months to September 2022, AREITs posted a total return of -21.5%, underperforming the S&P/ASX 200 return of -7.7%.

Sector Performance

Table 1 below shows the performance of AREITs for various periods ending 30 September 2022.

Over the 3 years and 5 years to the end of September, the sector produced total returns of -5.3% and 2.6% per annum respectively.

Sector returns were led by Diversified AREITs which produced a return of -10.2%. Retail AREITs were next with a return of -11.8% while Office AREITs returned -11.9% and Industrial AREITs returned -19.6%.

Table 2 below shows the income performance of AREITs for various periods ending 30 September 2022.

The income component of the total return was 3.9% for the 12-month period to September. Annual volatility of income returns was 1.6%, which is low when compared with other asset classes.

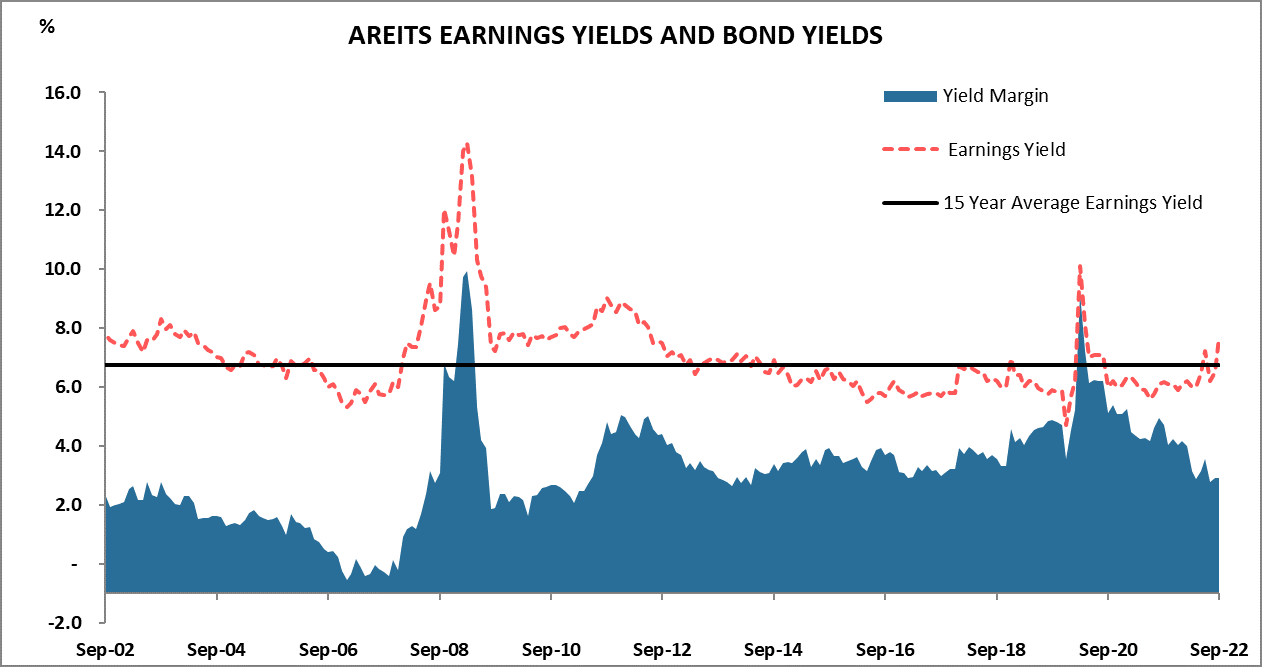

AREITs were trading at an earnings yield of approximately 7.7% at the end of the month, higher than yields of both cash and Commonwealth Government bonds. However, the spread of the earnings yield over the 10-year government bond yield rose to 3.8%.

Changes over time of the spread between the earnings yield of AREITs and the 10-year government bond yield are shown in Chart 1.

source: RBA, UBS (2022)

Market Review

Industrial AREITs have returned -19.6% for the month of September on the back of fears that central banks will push the global economy into recession. However, vacancy rates for industrial property are at an all-time low with rents increasing 30% across Sydney and 20% across Melbourne over the 12 months to September.

According to the CBRE, the six months to June saw the national average vacancy rate for industrial property slip to just 0.8%, compared to the 2.7% global average. In Sydney, vacancy rates were even lower, falling to just 0.3%. Low vacancy rates have stemmed from construction delays and rising costs due to labour shortages, wet weather and material shortages, with some projects delayed for up to one year.

Future demand for industrial space does not look like it will be satisfied in the short term. An additional 2.1 million square metres of industrial property was forecast to be built in the year to December 2022 but only 600,000 square metres have been constructed to date.