Summary: GDP valley less deep but wider; inflation lower for longer; jobless rate expected to peak later, followed by long, slow grind down; 2020 forecast implies RBA “positively surprised” by growth progress of non-Victorian states.

The Statement on Monetary Policy (SoMP) is released each quarter and it is closely watched for updates to the RBA’s own forecasts.

In May’s SoMP, the opening statement of the “Outlook” section stated, “The outlook for the Australian and global economies is being driven by the COVID-19 pandemic. The necessary social distancing restrictions and other containment measures that have been in place to control the virus have resulted in a significant contraction in economic activity…”

August’s Outlook carried on with this theme. “During the first half of the year, the COVID-19 pandemic led to the most severe contraction in global and domestic economic activity in decades.” However, the RBA then points to light at the end of the tunnel. ”Since around May, economic conditions have started to recover as containment measures have been eased and fiscal and monetary policies have provided significant support”.

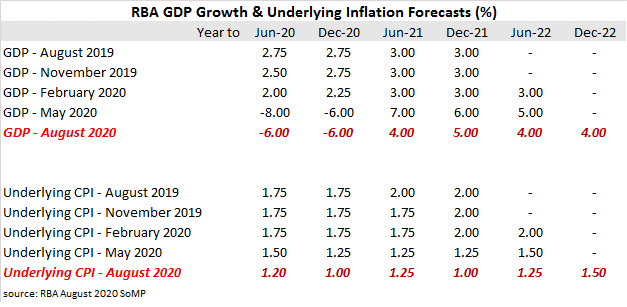

GDP growth rates in the early periods of the forecasts have increased or been maintained but at the cost of later periods. The RBA’s forecast GDP growth rate for the year to June 2020 (see table) has been increased by 2% but the following financial year (June 2021) has been cut by 3.00%. Forecasts of later periods have been noticeably trimmed, albeit from high levels. The RBA has retained its expectation from May of a “gradual recovery” under its baseline scenario but it has added on an assumption Victorian Stage 4 restrictions “are in place for the announced six weeks and then gradually lifted.” It has also allowed for modest tightening of restrictions “for a limited time” elsewhere in Australia.

The RBA’s underlying inflation forecasts were reduced in most forecast periods but not by great amounts. The RBA’s favoured measure of underlying inflation, the “trimmed mean”, had been expected to slow in 2020, then be maintained through 2021 before rising in 2022. Now the RBA expects underlying inflation to see-saw through to 2022 and then rise in the second half of that year. Underlying inflation “is expected to remain subdued over the forecast period, given low wages growth and substantial spare capacity in the economy.”

The RBA’s underlying inflation forecasts were reduced in most forecast periods but not by great amounts. The RBA’s favoured measure of underlying inflation, the “trimmed mean”, had been expected to slow in 2020, then be maintained through 2021 before rising in 2022. Now the RBA expects underlying inflation to see-saw through to 2022 and then rise in the second half of that year. Underlying inflation “is expected to remain subdued over the forecast period, given low wages growth and substantial spare capacity in the economy.”