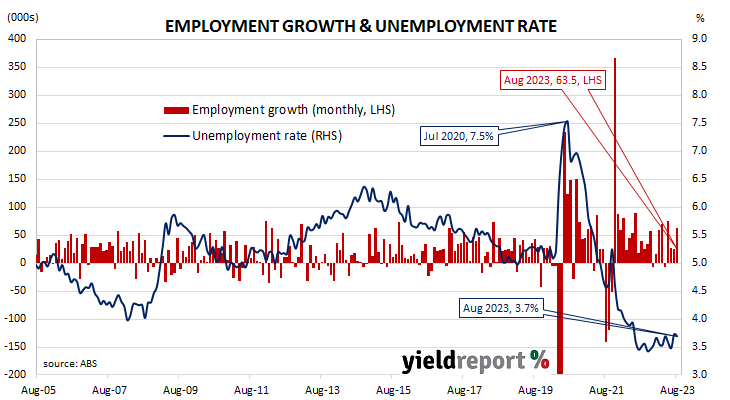

Summary: Employment up 64,900 in August, greater than expected; MSA: gradual softening from strong levels; ANZ: more “mixed” than headline gain suggests; participation rate ticks up to 67.0%; jobless rate steady at 3.7%; more part-time, full-time jobs; aggregate work hours down 0.5%; underemployment rate up from 6.4% to 6.6%.

Australia’s period of falling unemployment came to an end in early 2019 when the jobless rate hit a low of 4.9%. It then averaged around 5.2% through to March 2020, bouncing around in a range from 5.1% to 5.3%. Leading indicators such as ANZ-Indeed’s Job Ads survey and NAB’s capacity utilisation estimate suggested the unemployment rate would rise in the June 2020 quarter and it did so, sharply. The jobless rate peaked in July 2020 but fell below 7% a month later and then trended lower through 2021 and 2022.

The latest Labour force figures have now been released and they indicate the number of people employed in Australia according to ABS definitions increased by 64,900 in August. The result was greater than the 25,000 increase which had been generally expected and in contrast to July’s 1,400 fall after revisions.

“Labour market conditions were stronger than expected in August, with higher jobs growth and the unemployment rate flat, said Morgan Stanley Australia economist Chris Read. “Looking through the monthly volatility, the trend still looks to be one of gradual softening from strong levels, although some forward indicators have improved recently.”

Domestic Treasury bond yields declined on the day, somewhat following overnight movements of US Treasury yields. By the close of business, the 3-year ACGB yield had lost 2bps to 3.83%, the 10-year yield had shed 3bps to 4.11% while the 20-year yield finished 2bps lower at 4.45%.

In the cash futures market, expectations regarding further rate rises hardly changed. At the end of the day, contracts implied the cash rate would change little from the current rate of 4.07% and average 4.08% through October, 4.13% in November and 4.16% in December. February 2024 contracts implied a 4.18% average cash rate and May 2024 contracts implied 4.175%, 10.5bps more than the current rate.

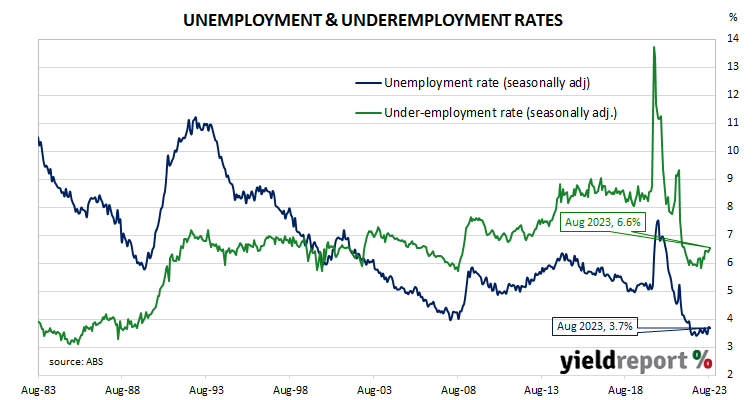

“This is a more mixed labour force survey than the headline 64,900 gain in employment suggests,” said ANZ Head of Australian Economics Adam Boyton. “In particular, the unemployment rate holding at 3.7%, the vast bulk of jobs growth being part-time, and hours worked falling in the month takes the gloss off the impressive headline jobs print. Yes, the labour market is still very solid but slack is creeping in; witness the increase in the underemployment rate to 6.6% in August from 6.4% in July.”

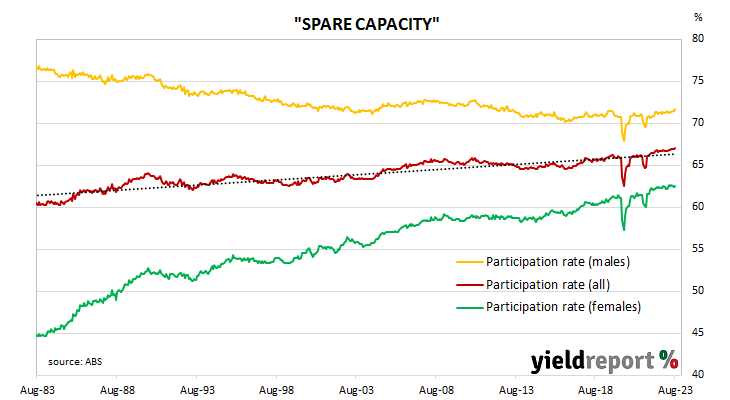

The participation rate ticked up from July’s revised figure of 66.9% to 67.0% as the total available workforce increased by 62,200 to 14.648 million while the number of unemployed persons declined by just 2,700 to 540,500. As a result, the unemployment rate remained steady at 3.7%.

The aggregate number of hours worked across the Australian economy decreased by 0.5% even as 62,100 residents gained part-time positions and 2,800 residents gained full-time positions. On a 12-month basis and after revisions, aggregate hours worked increased by 3.7% as 92,700 more people held part-time positions and 318,100 more people held full-time positions than in August 2022.

More attention has been paid to the underemployment rate in recent years, which is the number of people in work but who wish to work more hours than they do currently. August’s underemployment rate rose from 6.4% to 6.6%, 0.8 percentage points above this cycle’s low.

The underutilisation rate, that is the sum of the underemployment rate and the unemployment rate, has a strong correlation with the annual growth rate of the ABS private sector wage index when advanced by two quarters. August’s underutilisation rate of 10.3% corresponds with an annual growth rate of about 4.1%.