Summary: RBA cuts GDP forecasts for periods out to June 2024; underlying inflation forecasts rise again; jobless rate expected to fall to 3.25% by December then rise gradually; headline inflation forecasts increase significantly again; economists concerned RBA is “taking significant risk”.

The Statement on Monetary Policy (SoMP) is released each quarter and it is closely watched for updates to the RBA’s own forecasts.

In May’s SoMP, the opening two sentences of the “Outlook” section stated, “Global economic growth is forecast to be slower and inflation higher than forecast a few months ago. Inflation has been persistently high because many advanced economies are at or close to full employment, commodity prices have risen sharply and there are ongoing supply disruptions.”

As far as Australia was concerned, “A strong expansion in the Australian economy is underway. This is expected to continue over the forecast period, despite the slowdown in global growth.”

August’s Outlook opened with “Forecasts for global growth in 2022 and 2023 have been revised down since the May Statement, in response to the weaker outlook for real incomes and faster increases in policy rates.”

On domestic matters, it stated, “The Australian economy is expected to grow strongly over 2022, before slowing next year.”

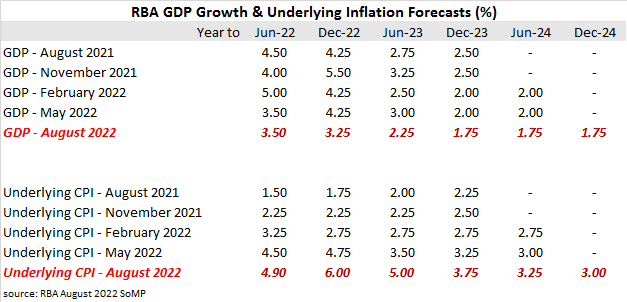

The RBA’s GDP growth forecasts have been lowered for all periods out to June 2024 (see table below). GDP growth for the year to December 2022 has been reduced by 1.00 percentage point while the forecast for the year to June 2023 has been reduced by 0.75 percentage points. Years to December 2023 and June 2024 have each been lowered by 0.25 percentage points.

“The slowing is anticipated to be broadly based, with slower growth in household consumption, weaker dwelling investment as housing prices decline, a stabilisation of public demand at high levels after recent rapid growth and slower growth in exports as the recovery in services exports nears completion.”

The RBA’s underlying inflation forecast have been raised again. The forecast for the year to December 2022 was raised by 1.25 percentage points while forecasts for the years to June 2023, December 2023 and June 2024 were raised by 1.50 percentage point, 0.50 percentage points and 0.25 percentage points respectively.

“Absent additional supply shocks, some cost pressures will wane over time. Further increases in labour costs in response to the tight labour market are expected to become the primary driver of inflation outcomes later in the forecast period. Headline and underlying inflation are expected to return to the top of the inflation target range by late 2024.”

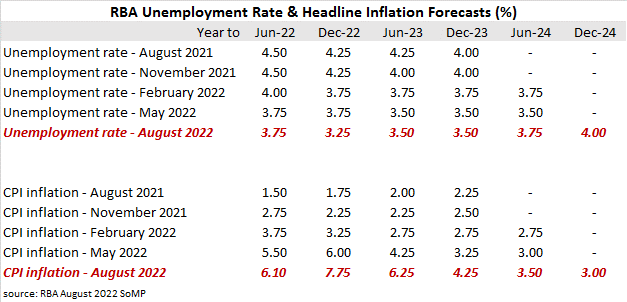

The RBA’s view of the unemployment rate typically follows from its forecasts of GDP growth. The unemployment rate has fallen to 3.50% at the end of June. The RBA now expects it to decline to 3.25% by the end of December but then increase to 3.50% by June 2023. The forecasts then flag an increase to 4.00% through 2024.

“Since the start of this year, labour market outcomes have been robust and leading indicators of labour demand suggest this will continue in the near term. Participation in the labour force is expected to be sustained at historically high levels over the forecast period, supported by the cyclical strength in labour market conditions and the longer term trend toward increased participation among females and older Australians.”

Headline inflation forecasts again have been increased significantly. The years to December 2022 and June 2023 have had their respective forecasts raised by 1.75% and 2.00%. The forecasts for the years to December 2023 and June 2024 have also been raised but by quite as much.

“Inflation is high and is expected to increase further in the second half of the year. The forecast for headline inflation has been revised up substantially compared with a few months ago, reflecting broad-based pricing pressures that are not expected to ease until early next year, as well as expectations of large increases in retail electricity and gas prices over the coming year.”

Commonwealth bond yields moved lower on the day, generally in line with the movements of their US Treasury bond yields overnight. By the end of the day, the 3-year ACGB yield had shed 3bps to 2.90%, the 10-year yield had lost 6bps to 3.11% while the 20-year yield finished 4bps lower at 3.46%.

Economists were somewhat concerned by what they saw.

“The detailed forecasts in the Statement on Monetary show that the Bank is taking a significant risk of allowing a damaging inflationary psychology becoming imbedded in Australians’ thinking,” said Westpac Chief Economist Bill Evans.

As for what the RBA has in mind for its end point, the assumption of a 3% cash rate in the Statement on Monetary Policy is interesting,” said ANZ Head of Australian Economics David Plank. “Even with the cash rate at 3% by the end of this year, inflation is at best expected to be at the very top of the RBA’s target band at the end of 2024. In time we think the RBA will conclude that this creates too much risk that inflation expectations move higher.”