Summary :

Overall GDP growth forecasts have been revised up to 1.9% in 2025 and to 2.4% in 2026, with 2027 unchanged at 2.6%. Upside risks include stronger-than-expected consumer spending and population growth, but a renewed slowdown in public outlays could dampen household spending and delay private investment recovery.

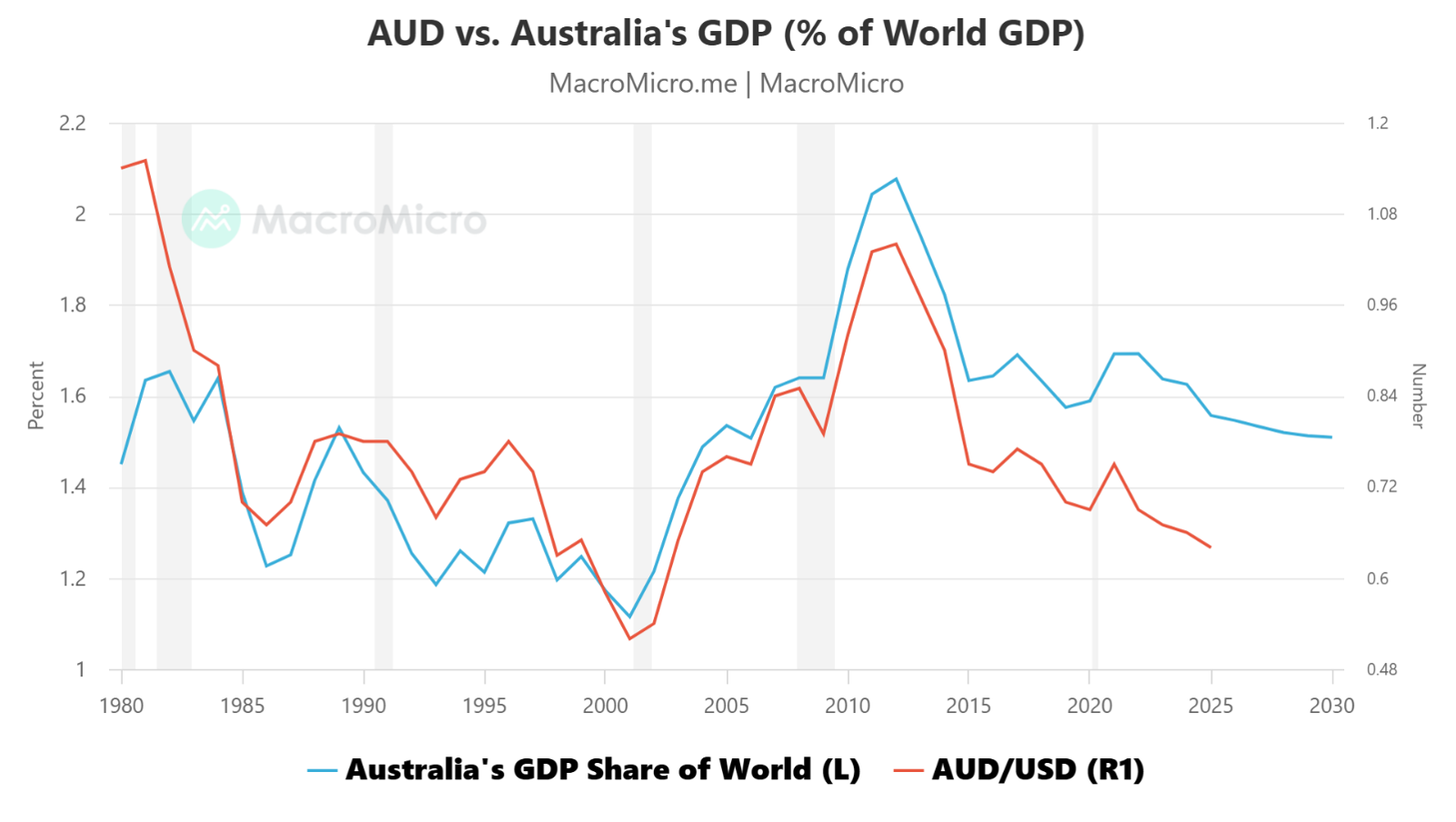

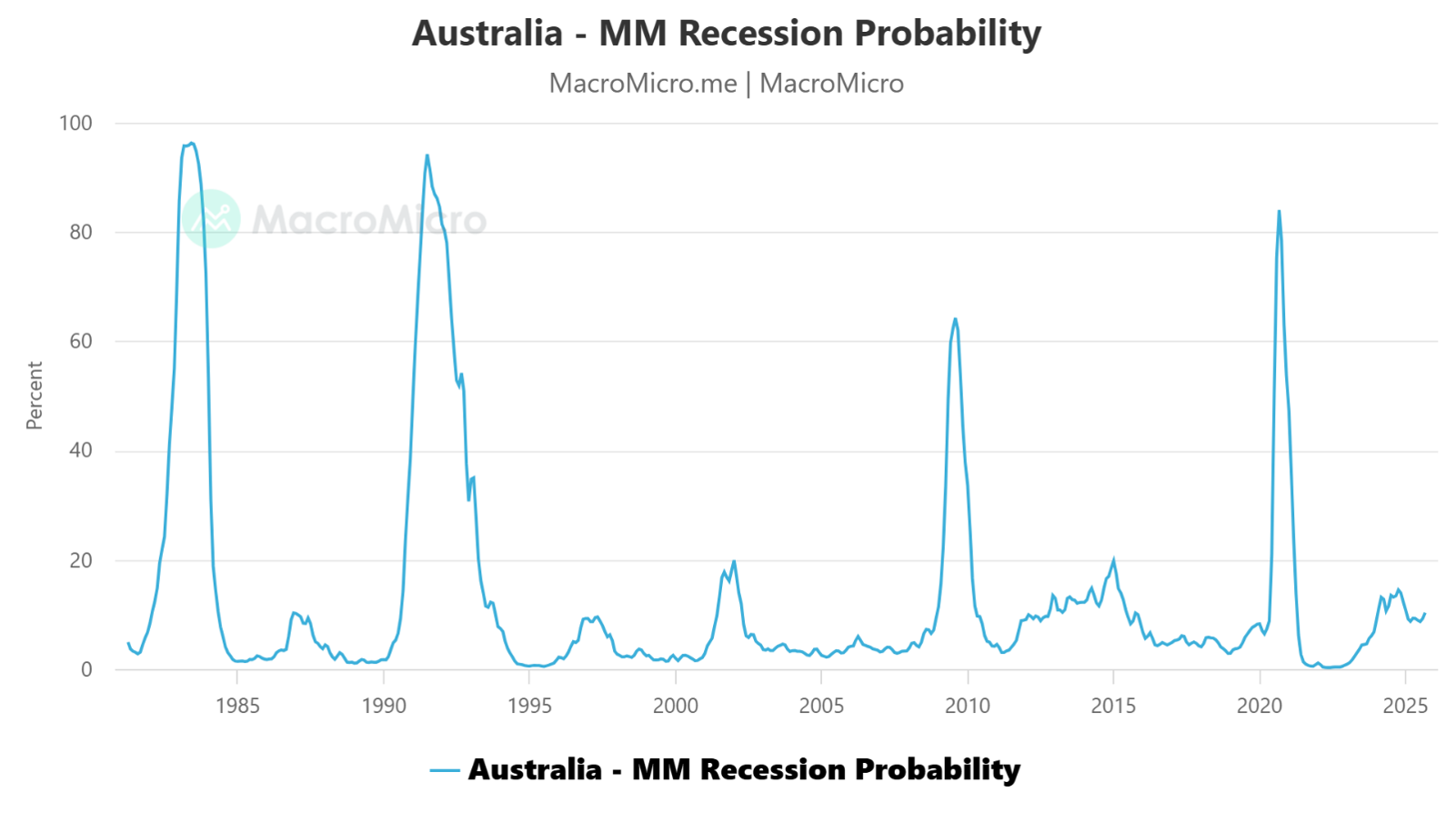

Australia’s Macro-Micro Probability of Recession indicator shows less than a 20% chance of a downturn, using six economic variables and research from the University of Melbourne and OECD to track GDP, unemployment, and equity trends. Australia’s global GDP share has declined from 2.1% in 2011 to 1.5% today, reflecting weaker relative economic performance and negative impact on AUD/USD.

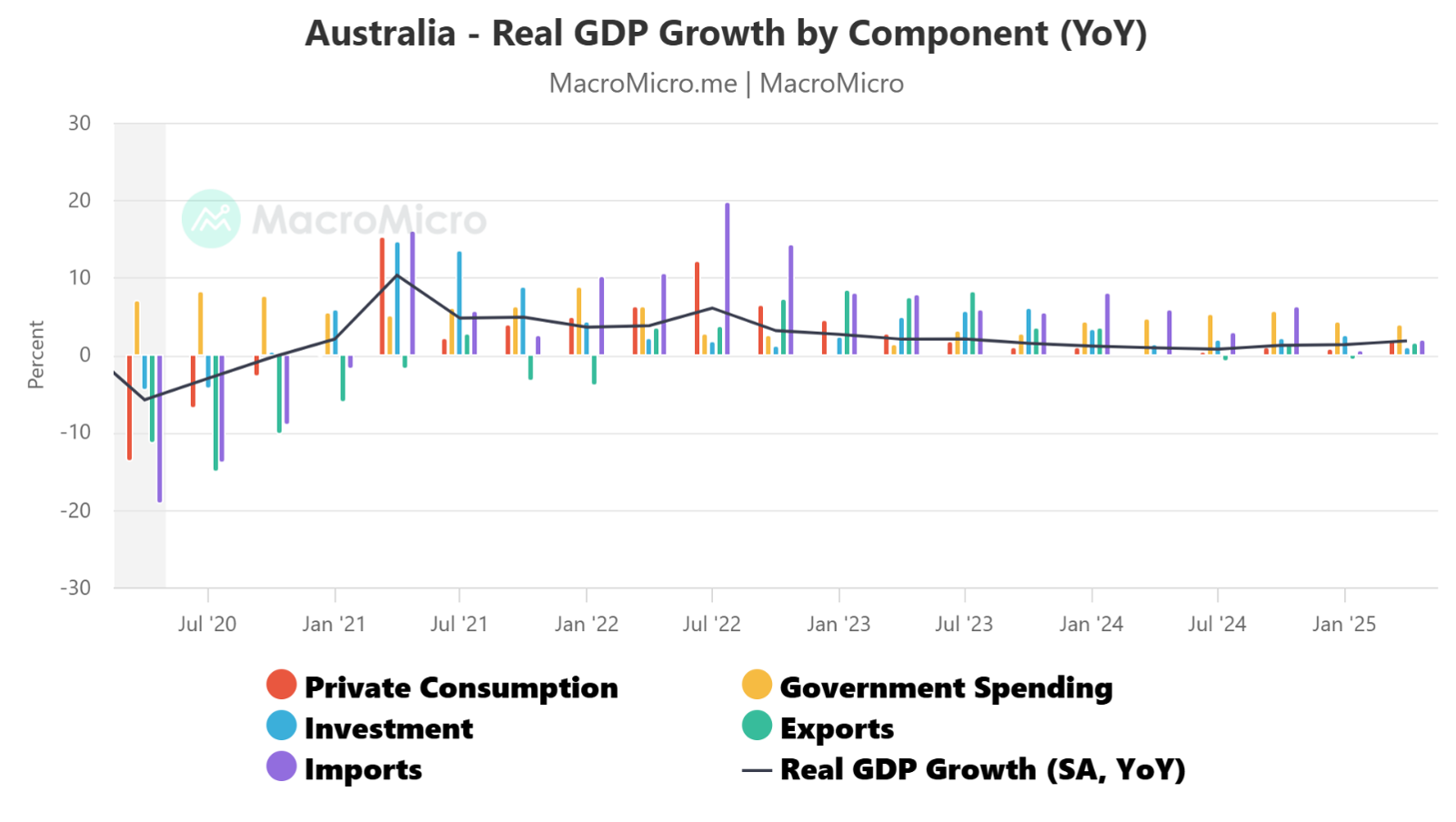

Cyclical Upswing Driven By Household Consumption

Australia’s GDP rose 0.6% in the June quarter of 2025 and 1.8% year-on-year, driven by the first annual increase in GDP per capita since March 2023. Other living-standards measures likewise showed improvements after two consecutive years of decline.

Household consumption grew 0.9% for the quarter—the strongest since December 2022—and was the first year-on-year increase in per-person spending in two years. Consumer sentiment turned decisively positive in Q2 as real disposable incomes rose 4.1% over the prior year, the fastest pace since 2011 outside the COVID period. Tax relief, interest-rate cuts and disinflation have all supported stronger purchasing power.

Some unusual factors underpinned activity. End-of-financial-year discounting prompted heavy retailer markdowns, inventories were run down, and corporate profits fell despite higher sales volumes. A 3.9% quarterly jump in consumer-goods imports—led by vehicles, clothing and leisure items—likely reflects early shipments rerouted to the US ahead of tariff hikes.

Goods spending (+1.0% quarter) outpaced services (+0.8%), marking the strongest quarterly growth in goods since June 2018 outside the pandemic. Discretionary services benefited from an Easter–Anzac holiday boost.

Residential construction remained subdued, up just 0.4% for the quarter (4.8% year-on-year), despite ample project pipelines. New private business investment declined overall, with intellectual property products the sole segment recording growth. Public investment has fallen roughly 7.0% over the past three quarters, weighing on construction services and real estate activity.

Underlying momentum in consumer spending has now more than offset the drag from slowing public investment. Stronger feedback loops—rising disposable incomes, gains in household net worth and improving optimism and improved GDP Growth forecasts by 0.2 percentage points to 2.2% in 2025 and to 2.6% in 2026. Per-capita consumption is projected to grow 0.8% in 2025, 1.2% in 2026 and 1.5% in 2027, compared with a 20-year pre-pandemic average of 1.8%.

Business investment is expected to remain sluggish, with private CAPEX forecasts cut by 0.7 points to 1.6% in 2025, by 0.5 points to 4.1% in 2026 and by 0.2 points to 4.7% in 2027 amid delays in large renewable projects. New public demand forecasts remain modest at 1.3% in 2025, 2.6% in 2026 and 2.5% in 2027, well below the 5.0% annual average since 2020.

Exhibit 1: Australian GDP Contributors

Government spending also played a pivotal role, contributing around 0.2 percentage points. Increased expenditure on health, aged care, and social services, alongside continued infrastructure investment, provided a stabilising effect against softer private-sector momentum.

Net exports added modestly to growth. A rebound in services exports, particularly tourism and international education, offset softer resource exports amid fluctuating global commodity demand.

Business investment made a positive, albeit smaller, contribution. Non-mining sectors expanded capital spending on equipment and machinery, though mining investment was more subdued, reflecting cautious sentiment around global demand.

Conversely, inventories detracted from growth, subtracting around 0.2 percentage points as businesses drew down stockpiles in response to slower goods demand.

Taken together, the June quarter data signals that Australia’s growth is being underpinned by services-driven consumption, public demand, and exports, while private investment and inventory cycles remain patchy. The composition of growth underscores the economy’s resilience but also highlights ongoing imbalances, with household spending tilted heavily towards essentials and reliant on government support.

Recession Probability is less than 20%

Based on the Macro-Micro Probability of Recession indicator, currently there is less than 20% chance of economic recession in Australia. The indicator for Australia uses a Dynamic Logistic Regression Model based on six key economic variables, including the Westpac Leading Index, employment metrics, and its own Economic Expectations Index.

It draws on research from institutions like the University of Melbourne and the OECD to define recession conditions, typically marked by falling GDP, rising unemployment, and sharp equity declines.

Exhibit 2: Australian Recession Probability is Very Low

Australia’s GDP Share is now 1.5% of the Global Economy

Australia’s share in the global gross domestic product (%) = Australian GDP (USD) / Global GDP (USD). When Australia’s share in the global GDP increases, it means that the Australian economy is performing better than the entire world, and the Australian dollar has upward momentum.

From a longer-term perspective, Australia’s global GDP share peaked at 2.1% in 2011 and has been declining since then to settle at 1.5% today.

Exhibit 3: Australia’s relative GDP growth is a Headwind for AUD