Australian government sovereign debt by Rob Nicholl, CEO, AOFM

An insight into how the AOFM thinks about certain issues in terms of sovereign debt market development.

We were initially cautious in our approach to extending the yield curve because we were unsure about the level of demand for our paper longer than required for supporting the 10y futures contract … Having extended the nominal and linker (CPI linked bonds) yield curves to around 15 years I recall us feeling pretty pleased with our efforts – but issuance programmes weren’t reducing – they were still growing. This prompted us to plan for further yield curve extensions. Last year I said that our aim was to consolidate a 20y benchmark and with successive launches of the 2033, 2037 and 2035 maturities I would argue we have now demonstrated an ability to do just that.

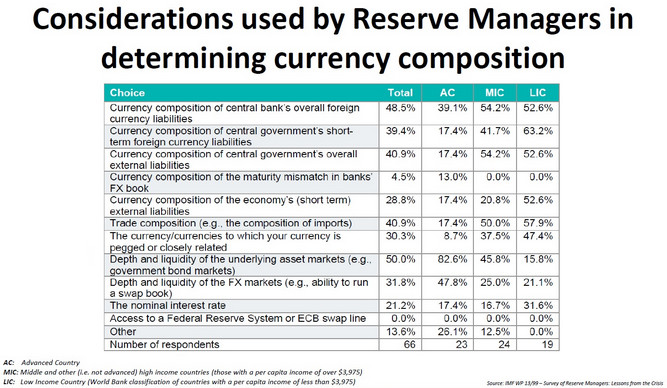

While we don’t typically have access to documented insights of investor preferences, a few years ago the IMF sought to identify those of central banks when considering the currencies they hold.

With regard to the range of choice there are, as mentioned, the number of bond lines on offer and length of the yield curve. The recent announcement by the ASX of its intention to introduce a 20 year futures contract offers, from our perspective as the issuer, a positive development opportunity for the AGS market.