Summary

The Australian labour market added 2000 jobs in June, missing to the downside of consensus estimates at 20,000. As a result, the unemployment rate increased 21 bps to 4.3% from last month’s 4.1% level. Underemployment ticked to 6%.

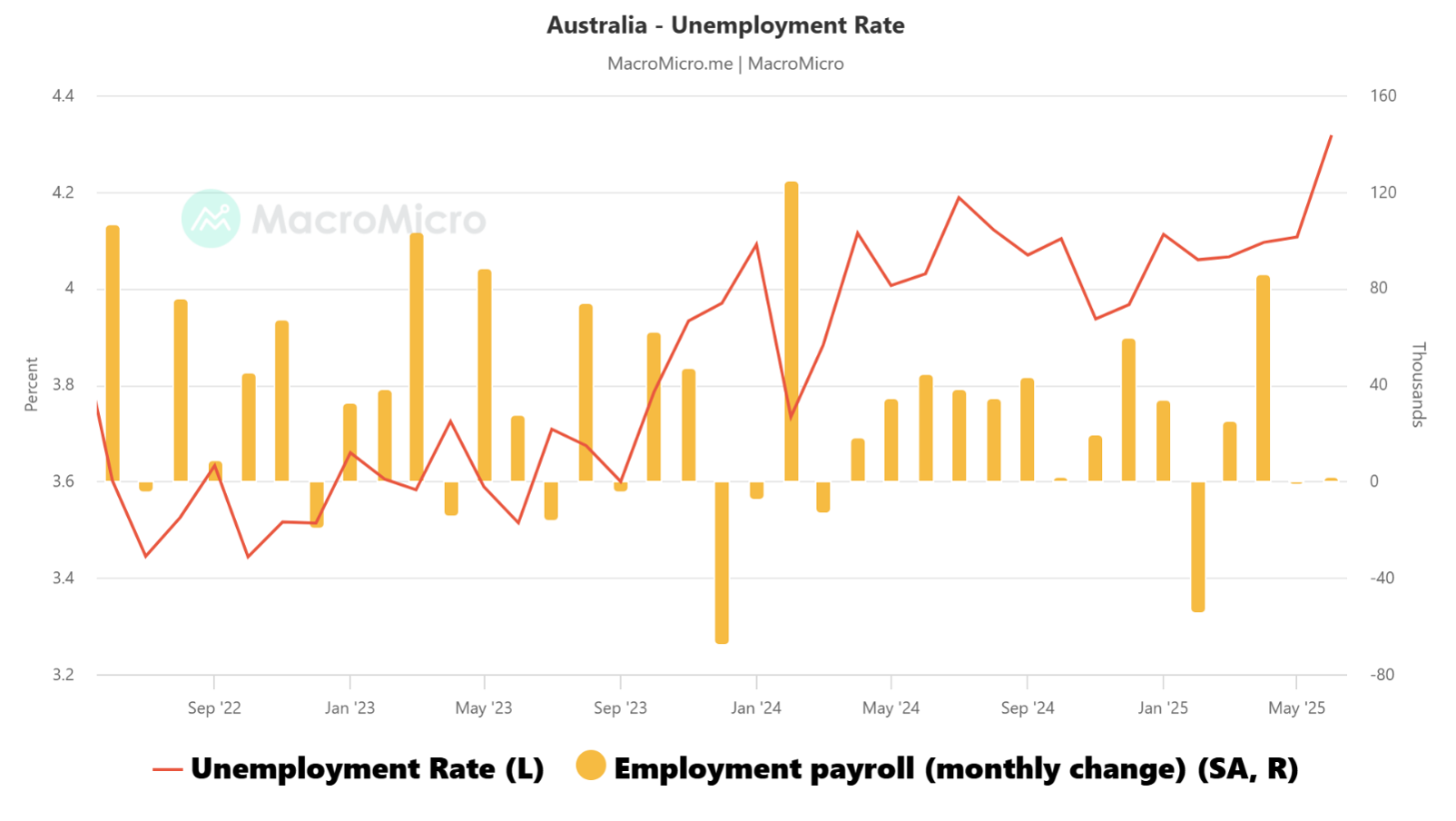

Exhibit 1 shows the gradual increase in UR over the past 3 years. This is despite the Government sector driving majority of the job growth over the past few years as the private sector has been on consolidation mode and cautious on business investments.

The participation rate rose 10 bps to 67.1% while the employment-to-population ratio was relatively steady around 64.2%.

Growth is still coming off a high base though, annual growth holding at 2.3% year on a three-month average basis. However, it is also revealing that average hours worked posted a significant decline (–1.0%), falling short of the long-run trend and providing an explanation for why underemployment ticked up to 6.0%.

The most notable and surprising development in the report was the unemployment rate’s 0.2ppt increase to 4.3% after five consecutive months at 4.1%. This looks to have been driven by a material increase in youth unemployment (ages 15-24), up 0.9ppts to 10.4% in June. While there is likely some noise in the data, moves of this quantum in the past have often preceded a grind higher in total unemployment.

The May and June labour market updates suggest a gradual softening in conditions may be resuming after the recent period of resiliency. Having remained on hold in July, this data adds weight to the already-strong case for a 25bp rate cut at the RBA’s August meeting.

Also of note for Australia this week, the Westpac-MI Consumer Sentiment index highlighted households’ disappointment with the RBA’s July decision. The responses received prior to the decision equated to a reading of 95.6, while those surveyed after came in at 92.0. The net result was a modest rise in overall sentiment, up 0.6% to 93.1 in July. This ‘cautiously pessimistic’ reading reflects the enduring impact of earlier cost-of-living pressures on real incomes and consumption.

On the back of this data, Australian government bonds rallied strongly with rate cut expectations firming further. Three-year government bond yields fell 9 bps while the ten-year government bond yields dropped 6 bps immediately after the data was released, holding most of these gains into the days close. The Futures Market is pricing in a near 100% probability of an August rate cut by RBA, and then another cut in November, down to 3.35%. The data release last week gives the RBA flexibility to cut, however inflation is arguably more a focus at this stage given the crosscurrents from Trump Tariffs. The next inflation data is June quarter CPI, which is scheduled for July 30th, well ahead of the next RBA meeting (August 12th).

Exhibit 1: Australian Unemployment Rate Grinds Higher

About YieldReport – Your Income Advantage

YieldReport is Australia’s leading online data and research platform for interest rate markets, securities and products that focus on fixed income and yield generation. YieldReport provides advice, reviews, analysis and insights on what’s shaping the yield curve and fixed income markets. It’s a key reference for pricing and performance data on yield-generating investments — from cash, term deposits, and bonds to hybrids, ETFs, and more.

Its insights help individuals and institutions make informed decisions — whether managing their own portfolios or acting in fiduciary roles.

Explore more via the website: www.yieldreport.com.au

Follow daily updates on LinkedIn, X, Instagram & Facebook.

Contact us: contact@yieldreport.com.au or call 0408 266 713.