By Ken Atchison, Principal, Atchison Consultants

Critical for the Australian recovery from the recession, driven by coronavirus, is growth in bank credit. While Australia faces a health crisis and an economic crisis, avoidance of a financial crisis is pre-eminent in the policy. Sustained profitability of the banks is required both for growth in credit and continued dividend distributions for investors.

The RBA and APRA have made it clear that capital and liquidity buffers are available to be drawn down in this period of weakness. Both are members of the Council of Financial Regulators, the body which provides a forum for co-operation by regulators.

Buffers were established during periods of economic strength to provide for periods of economic stress. Now the economic stress has arrived, they stand ready to be drawn down.

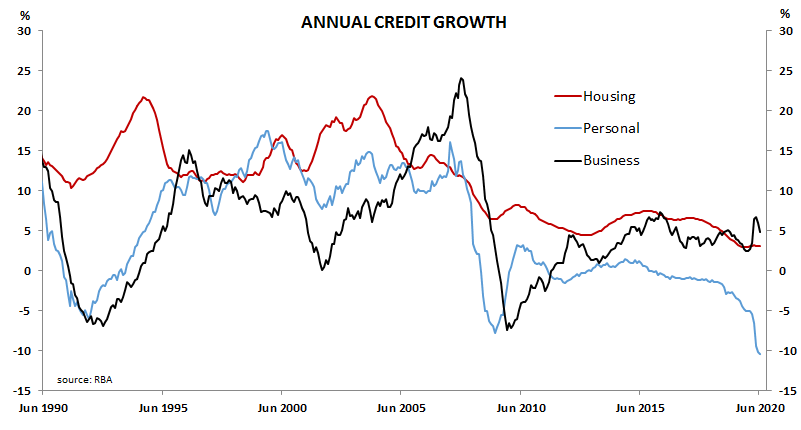

Data to June 2020 shown in Chart 1 indicates private sector credit declined by 0.17% in June following a fall of 0.14% in May. While weak, it is declining primarily in personal credit which contracted by 10.5% over the year to June 2020. Despite this fall in personal credit, total private sector credit data suggests that RBA and APRA are being effective in providing policies ensuring access to a wide range of funding sources, including bank credit.

Chart 1 – Private Sector Credit Growth

APRA guidance for banks regarding dividends has changed. Initially, banks were encouraged to defer dividend payments until the outlook was clearer. Recent guidance now includes prospective dividend payouts of up to 50% of earnings.

Banks now know where they stand in relation to their capital positions. They will have to continue with stress testing to ensure they can deal with any future shock but the existence of the capital buffers will allow banks to support ongoing lending.

In the years following the financial crisis of 2009/2009, banks’ capital requirements were increased, restricting new lending to some degree and thus bank profitability. Bank profitability is now being negatively impacted by the recession and it will suffer further from the disaster in Victoria. Interest rate margins are reduced, loan loss provisions have increased and loan growth is lower.