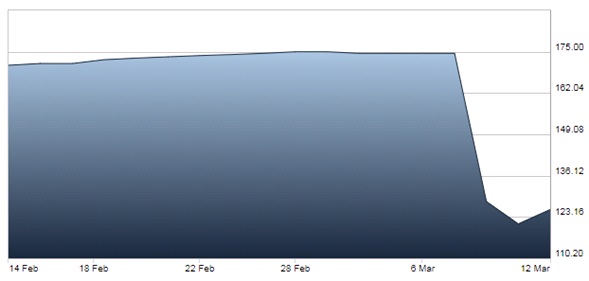

A metaphorical bomb hit the UK preference share market last week when insurance company Aviva announced, on the back of strong profits and the proceeds of asset sales, that that it would consider cancelling its “expensive” preference shares. Nothing unusual in that, you might say, except the particular preference shares referred to were issued in 1992 as “cumulative and irredeemable” and they have a coupon rate of 8.75% per annum.

Most investors would interpret this as meaning the preference shares will pay a high rate of interest in perpetuity, with the word “irredeemable” (in the ordinary meaning) indicating the securities will never be redeemed by the company. However, “irredeemable” or “cancellation” or “return of capital” may technically be different things and this pedantry saw the price of the securities plunge from around £175 per security to around £118 before they recovered above £120.

Aviva’s 8.75% preference share price over the last month:

source: LSE