By guest contributor Craig Morabito, Portfolio Manager, Global Credit, Colonial First State

Credit spreads, the difference in yield between a bond and a debt security with equal maturities, have tightened towards historically low levels in recent years. This has investors asking, how much further they can go and what will happen if, or more likely when, they start to widen again?

There are a number of factors at hand that may impact both the timing and the magnitude of the widening including the potential unwinding of quantitative easing (QE) globally and tail risk events such as heightened geopolitical unrest.

Before considering these outside factors let’s review the current credit market fundamentals, valuations and technicals.

Corporate leverage is high but stable and earnings are strong

In the March earnings season we saw the increase in leverage, which had been occurring over recent years, finally peak. To date in the June earnings reporting season, leverage has stabilised and earnings have been strong – both of these fundamental facets are positive for credit markets. Importantly, near term risks are limited and defaults are likely to remain low due to easy access to funding, low interest rates, term out maturity profiles and the improving economic backdrop.

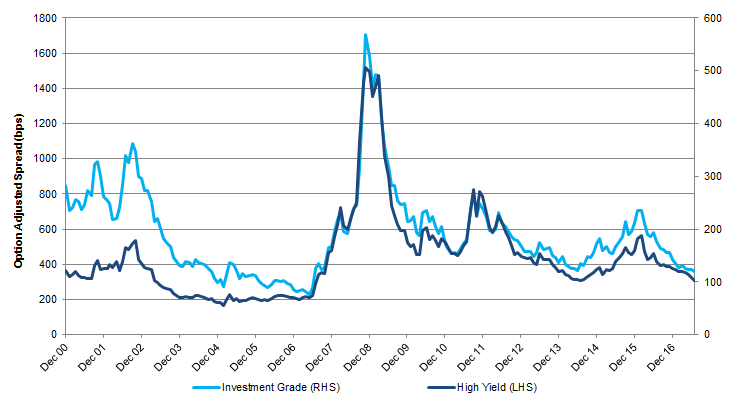

Valuations are tight, but not concerning

Credit valuations are tight but this is unlikely to be a catalyst for widening as valuations can remain at these levels for long periods of times (possibly a number of years). In addition, flows into investment grade credit remain very robust with heightened levels of issuance to meet the insatiable demands in the current low interest rate environment. Hence it’s unlikely that any of these factors will lead to a sudden surge of widening credit spreads.

Fig 1: Credit spreads are reaching historic lows but can stay at this level for a period of time