Elstree Investment Management is a Melbourne-based fund manager which specialises in ASX-listed hybrid securities and notes. In its latest review it thought it may be interesting to examine what happened to corporate credit in the 1970s given the latest predictions about inflation. Even though they view the 1970s as a rogue decade which is highly unlikely to be repeated, they think it is the only decade in living memory with sustained inflation and therefore a good example of what happens when inflation is ongoing.

Inflation increased in the early 1970s due to an explosion in oil prices and a combination of lax fiscal and monetary policies. By the late 1970s high inflation was endemic. Monetary policy was tightened and a recession occurred.

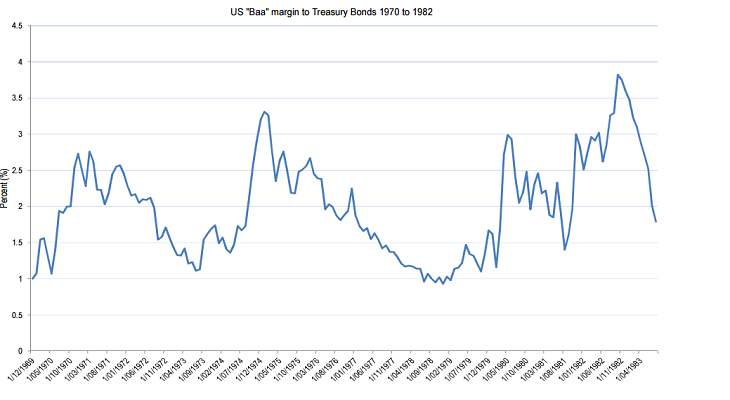

One would expect a sudden spike in inflation which is then sustained to produce an initial surge in corporate defaults, which would then be followed by lower defaults over time as the value of the debt is eroded. According to Elstree, this is roughly what happened. During the 1970s, defaults by investment grade issuers were very low. With “Baa”/”BBB” credit margins at the start of the decade at 1%, there was a noticeable 0.75% higher return (after default costs) for investing in corporate bonds. In a high inflation environment, corporate bonds performed well, at least at first glance.

However, while the fundamental outlook was healthy, margins over Treasurys increased. The chart below shows margins of Baa-rated bonds over Treasurys from the start of the 1970s to the early 1980s.

US inflation peaked in early 1980 at 14% and bonds peaked in late 1981 at 15.1%. “Baa” bond margins peaked in late 1982 but were consistently hitting 3% between 1979 and 1982. This led to capital losses for corporate bond portfolios, although returns were bolstered by coupon income. The extent of the capital loss was commensurate with the duration of the portfolio. The question is, would margins increase this time around if inflation were to rise?