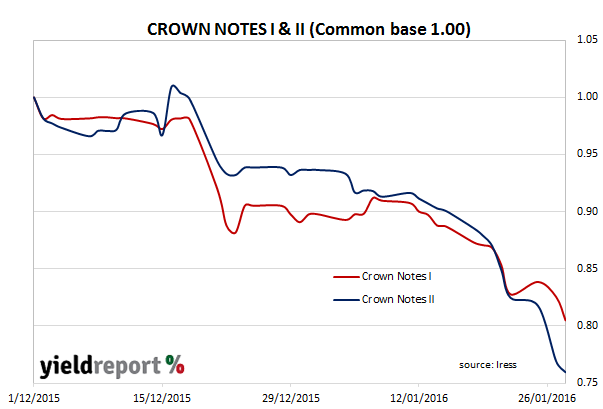

Last week (21 January) YieldReport published an article on James Packer’s potential privatisation of Crown Resorts Ltd and the effect the speculation was having on Crown’s two hybrid securities. Over the course of the previous month, the price of Crown Notes I (ASX code CWNHA) and Crown Notes II (ASX code CWNHB) had fallen from $93.25 and $87.00 to $86.50 and $78.24 respectively, which meant the trading margins* of each had increased considerably.

Just over a week later, the trading margins have gone even higher as prices of each of the two series has declined further. Reports of a tie up between Packer interests and Blackstone Real Estate may have exacerbated the selling in the notes as such a deal would help fund a possible privatisation. It would represent another box ticked in the privatisation process and therefore increase the likelihood of note holders facing a scenario not of their liking. Sellers have been keen to get out and thus the price of the series I notes fell to $81.60 while the series two notes fell to $70.00