Summary: Australia’s GDP up 0.2% in December quarter, in line with expectations; Westpac: weakest six-month performance since the GFC excluding COVID years; ACGB yields fall noticeably; rate-fall expectations harden; Citi: household savings ratio rises, consumers spending more on essential goods, services, less on discretionary items; imports, inventories again major influences in quarter.

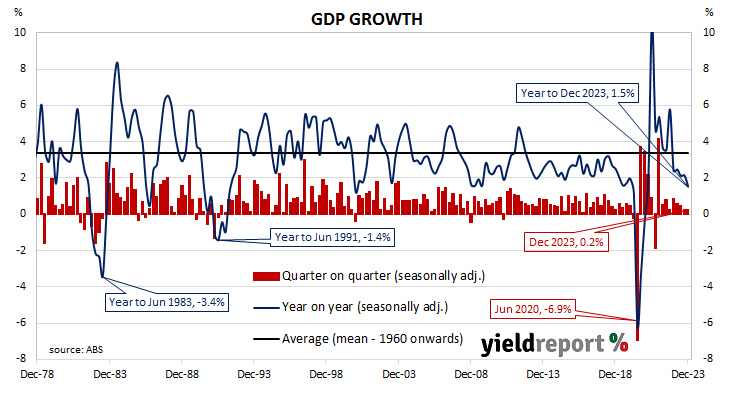

Since the “recession we had to have” as the recession of 1990/91 became known, Australia’s GDP growth has been consistently positive, with only the odd negative quarter here and there. However, Australia’s first recession in nearly thirty years was inevitable in 2020 once governments introduced restrictions which shut businesses and limited people’s movements for an extended period of time. Growth rates have been positive since then, although the September 2021 quarter proved to be the exception after restrictions were reintroduced in eastern states.

The latest GDP figures have now been released by the ABS and they indicate GDP rose by 0.2% in the December quarter. The result was in line with expectations but down a notch up from the 0.3% growth rate in the September quarter after it was revised up from 0.2%. On an annual basis, GDP expanded by 1.5%, down from 2.1%.

“The Australian economy posted a weak finish to 2023, expanding by just 0.2% in the final quarter and annual growth moderating to 1.5%” said Westpac senior economist Matthew Hassan. “The economy tracked a 1% annual growth pace through the second half of last year. Outside of the extremes seen during COVID, this is the weakest six-month performance since the GFC hit fifteen years ago.”

Commonwealth Government bond yields fell noticeably on the day, largely in line with falls of US Treasury yields overnight. By the close of business, the 3-year ACGB yield had lost 6bps to 3.62%, the 10-year yield had shed 9bps to 4.02% while the 20-year yield finished 8bps lower at 4.33%.

In the cash futures market, expectations regarding rate cuts later this year and early next year hardened. At the end of the day, contracts implied the cash rate would remain close to the current rate for the next few months and average 4.315% through March, 4.305% in April and 4.27% in May. However, August contracts implied 4.135%, November contracts implied 3.965% and February 2025 contracts 3.83%, 50bps less than the current rate.

“Household spending growth was weaker than expected, with consumers spending more on essential goods and services and less on discretionary items,” said Citi economist Faraz Syed. “Most surprising was the increase in household disposable incomes which came from rising wages and lower income tax payable. Combined with slower household consumption, this caused the household savings ratio to rise in Q4.”

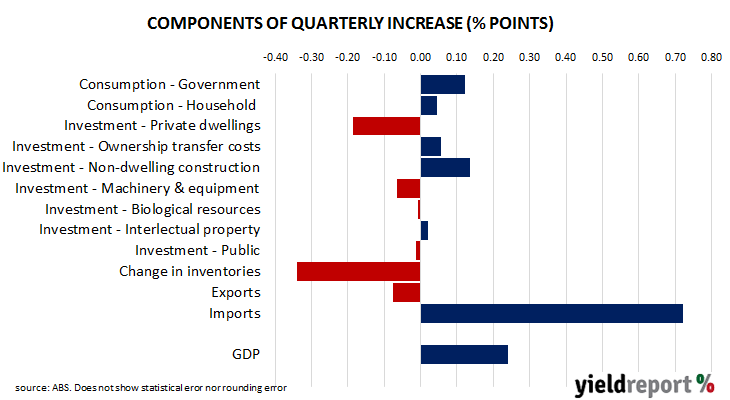

Imports decreased by $4.4 billion, adding 0.72 percentage points to the quarter’s overall result, while a $2.7 billion inventory contraction contributed -0.34 percentage points. Households consumption contributed just 0.04 percentage points.