- Geopolitics is disrupting what should have been a positive 2025. The chaos of the Trump administration’s economic policies could soon cause consumers and businesses to delay or cut spending. This uncertainty makes it difficult for investors, with the US consumer at the tipping point. For now, maintain current risk exposures, but reposition into defensive equities and better-valued markets such as Europe and Japan over Australia and the US.

- The global trade war has destroyed equity sentiment, but this can mark the bottom of a correction. Investors positioning for the worst now could get left behind if sentiment improves from these rock bottom levels. The US consumer remained resilient to the Fed’s tightening cycle and the 2022 surge in inflation, so investors should not underestimate its resilience.

- Build defence and diversify into non-US exposure. Our equities preference is Europe and Japan over the US and Australia and this has not changed. EM may also perform well if the US dollar continues to fall and the US economy remains resilient. Japan and Europe have a valuation advantage that the US and Australia do not along with a solid earnings outlook.

- Maintain the overweight in sovereign bonds and underweight in high-yield credit and cash. Move to overweight infrastructure and property from neutral. The global trade war has led to a rally in sovereign bonds on prospects of weaker growth and this will likely snowball if the fallout from the trade war affects the real economy. The market is rightly more concerned about growth than the inflationary consequences of the tariffs, so investors should build a defensive position with assets that benefit from lower bond yields.

Global Economic and Market Context

An otherwise good year for risk assets is being disrupted by geopolitics. The global trade war has begun earlier than we envisaged. The Trump administration has also made aggressive cuts to immigration and Federal government employment. Foreign aid has been cut and US military support for Ukraine was frozen and then reinstated as a negotiation tactic to end the war with Russia. Market-friendly election promises like deregulation in key industries and lower corporate taxes have not yet been pursued.

In our 2025 outlook, we highlighted our big 5 macro factors investors need to navigate this year.

- Geopolitics will play a larger-than-normal role in driving returns.

- The US remains the global economy’s engine of growth.

- Inflation has eased and policy is pivoting to support growth.

- Australia will remain in limbo.

- A lot of good news is priced into US risk assets.

Our worst-case scenario from the pre-election promises is emerging. US Tariffs are being applied at the upper end of our expectations, with no offsetting benefits from deregulation or tax relief on the horizon. The cuts to immigration and government spending will also put downward pressure on growth, but trade policy is the immediate concern.

Global supply chains are already in chaos, with 25% US tariffs on Canada and Mexico goods on and off again or delayed. China saw its tariff increase raised from 10%pts to 20%. The Chinese response thus far has been measured and targeted. The authorities have also indicated a willingness to stimulate domestic demand to fill the void created by the trade war.

Global steel and aluminium suppliers to the US have been dealt a 25% tariff with no exemptions.

One difference between the first Trump administration’s approach to tariff resetting and the current administration is that there was a set-and-forget approach that created more certainty. This time around delays, increases and retaliation make it difficult to estimate the true economic cost.

The administration also moved quickly in attempting to bring the Russia-Ukraine war to an end. At this stage, US military aid and intelligence were frozen initially, then returned while the fighting continued. The Israel-Hamas war has already become a regional conflict that seemed to have no end in sight until the US brokered a ceasefire. A sharp rise in oil prices is the key immediate threat from these conflicts if supply is threatened. For now, the oil market is more concerned about the global economic slowdown from the tariff increases.

All of this creates uncertainty and financial markets don’t like uncertainty.

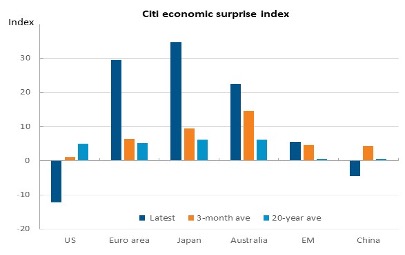

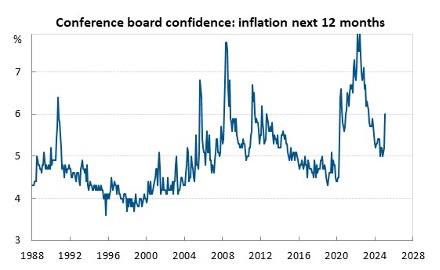

Even central banks are uncomfortable with the uncertainty and have ceased easing policy. Trade policy is also beginning to impact US data with inflation expectations increasing sharply and US and Chinese growth slowing in the past two months. This is disappointing from an investor’s perspective because 2025 could easily have been a year where growth picked up and central banks continued to ease policy, which is an environment that is normally positive for risk assets.

Figure 1: Growth is slowing in the US, but picking up in Europe and Japan

Source: LSEG, Macro Strategy Advisors

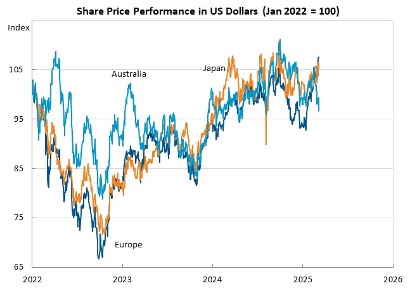

The speed of developments in key areas of US economic policy saw our expectation of US underperformance bought forward. Europe, Japan, and Emerging Europe have all outperformed the other markets. Trump also mentioned that a 25% tariff will soon be applied to European exports so European outperformance may be on borrowed time.

Figure 2: The Australian and US markets have underperformed.

Source: Refinitiv, Macro Strategy Advisors

We think the bond market’s reaction to the global trade disruption has been directionally correct, and investors should look to it as a sense check on growth and inflation. The market seems to be more concerned about weaker growth rather than higher inflation from tariffs. Tariffs are also a concern for earnings because firms may find it difficult to pass on costs, given monetary policy is still relatively restrictive. Developments in the labour market are more important for inflation than tariffs on goods.

The US 10-year yield has rallied by about 40bp since mid-January on fears that America First policies could sharply slow the economy. While tariffs remain in place, there is likely to be weaker growth, and the bond market rally could easily extend further.

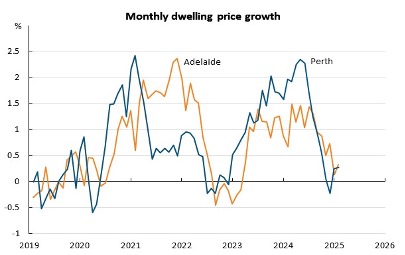

Australia remains dependent on government spending, and trade. The tax cuts that came into effect after last year’s budget boosted consumer spending during Q4. The RBA interest rate cut in February should see this modest pickup in momentum continue for the remainder of the first quarter. However, the RBA needs to see more disinflation before cutting rates again, with the next opportunity to lower rates in May following the release of the Q1 CPI. Dwelling prices rose in Sydney and Melbourne in January and the first increase in these markets for many months.

Figure 3: Sydney and Melbourne prices on the rise again

Source: LSEG, Macro Strategy Advisors

US risk assets entered the current period of uncertainty with the highest 12-month forward EP since the dotcom boom of the late 1990s. This has left the market exposed to cracks in the earnings outlook. However, until the past month or two, the economy and stock market earnings maintained their resilience to inflation and high interest rates. More importantly, the consensus earnings outlook seems consistent with current financial conditions.

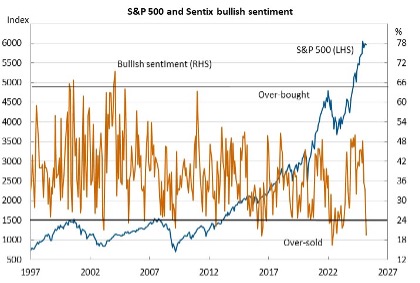

Sentiment indicators suggest the US equity market is oversold, but that will depend on how long the uncertainty persists. Sentiment at current levels is normally the precursor to a rally, but whether it develops for or not will depend on how the US consumer weathers higher tariffs.

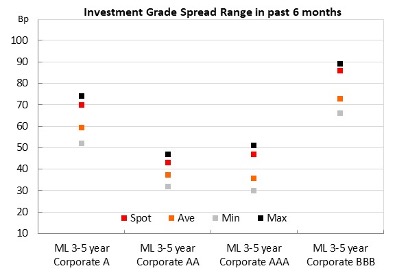

Investment grade credit spreads have reached their highest level in 6 months. High-yield credit spreads are about 60bp higher than at the start of the year and are similarly at their highest level in 6 months. We will continue to monitor the widening in credit spreads to check on equity performance. Sometimes equities and credit assess risk differently, with credit markets often providing a more accurate assessment.

The geopolitical landscape in Gaza and Ukraine has shifted, with implications for China’s ambitions in the Asia Pacific. US military support for Ukraine is on tenterhooks and Europe needs to increase its military support if Ukraine is to endure. Similarly, negotiation of a two-state solution in Gaza has stalled, with President Trump insisting the US owns and rebuilds it. The US administration’s reluctance to support traditional allies such as Europe, and impose tariffs on other long-term allies such as Canada, implies it would probably be reluctant to defend Taiwan from Chinese attack. This issue simmers in the background but it’s one that markets need to be cognisant about.

Global Bonds

The bond market has priced the downside risks to growth from US tariffs rather than the inflationary consequences. There are signs that US growth is under downward pressure and unless there is more certainty about trade policy it could easily fall onto a slippery downward slope. For most of this year, we think there are only downside risks to interest rates at bond yields.

- At the end of last year, we expected inflation and monetary policy to ease but growth was expected to remain resilient. We will need to see more evidence of a slowdown in growth before we become more positive on global sovereign bonds.

Inflation limits the ability of central banks to respond to the risks of slower growth, and signs are emerging

Australian Bonds

Australian sovereign bonds score 6.8.

The RBA has lagged other central banks in easing policy and the domestic economy remains weak. OIS markets expect the RBA to ease policy by 63bp, as of 17 March. However, the RBA will be guided by the room it has with inflation and the risks to global growth from the global trade war. It has become a difficult balancing act. The Australian steel and aluminum industries did not gain an exemption from US tariffs and need to absorb the 25% increase in their landed cost in the US like all other producers. However, the main risk of damage to Australia is second order. Australia will feel the pain from the slowdown in global steel demand but via weakness in the price of iron ore. The Aussie 10-year yield has been trading at the top of its range for the past 18 months and provided inflation continues to ease then yields should follow inflation lower. Wages growth is also easing, but needs to slow further for the RBA to gain more confidence to ease policy.

Source: LSEG, Macro Strategy Advisors

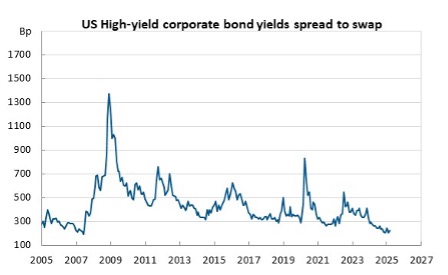

US Credit Markets

Our scores for US credit markets are unchanged since our last TAA/DAA update. US investment grade credit scores 3.0 while high-yield scores 1.5pts. Despite some widening in spreads over the past couple of months, investment grade spreads are generally tight. However, they could easily widen further given the increase in global economic and geopolitical risk.Similarly, high-yield credit spreads also remain historically tight, after narrowing during January and then widening as equities have sold off in February/March. Both grades of credit are expensive relative to swaps, government bonds, and equities with only limited risk being priced into these markets.

Equity Markets

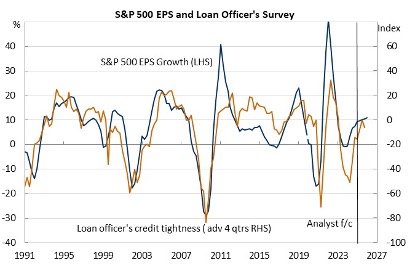

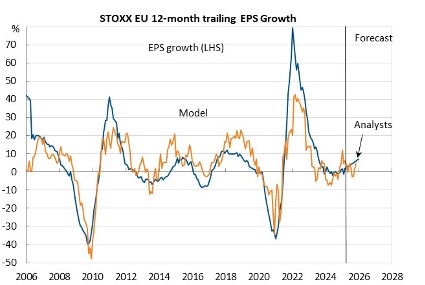

The main difference between Australia and the US is that the US earnings outlook is significantly more positive, with consensus US earnings expected to increase by 13% this year vs just 5.3% for Australia. Consensus expects European earnings to increase by 8% over the next year and Japanese earnings to increase by 9% over the same period. Both forecasts are consistent with our modelling, which uses financial conditions, business survey data, and exchange rate movements as inputs. Tariff increases and costs associated with forced supply chain adjustments will be reflected in business surveys, but it is too early to quantify the full impact. Exchange rate movements are also important, and the US dollar has been depreciating after peaking in mid-January, probably because of expectations that the Fed may need to ease more than anticipated to preserve growth. More positively, our score for Europe increased from 4.2pts to 4.4pts.

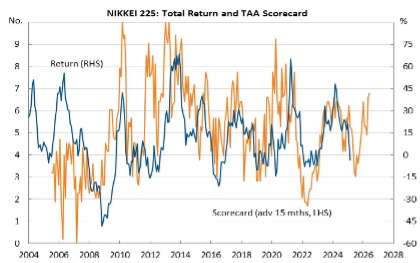

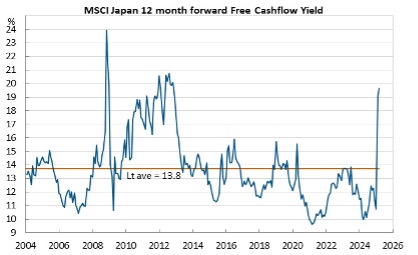

Japanese earnings are leveraged to fundamentals affecting export growth such as US tariff increases and movements in the US dollar/Yen exchange rate.The market benefitted from the strength of the US dollar leading up to the change in administration and it has valuation support with a relatively positive earnings outlook. We expect investors will be willing to pay for cheap earnings growth this year over markets where there is uncertainty about the earnings. Our scorecard suggests upside risk to Japanese equity returns over the next 15 months

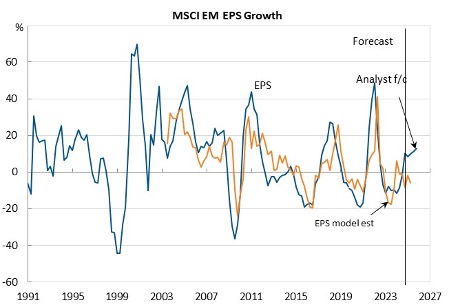

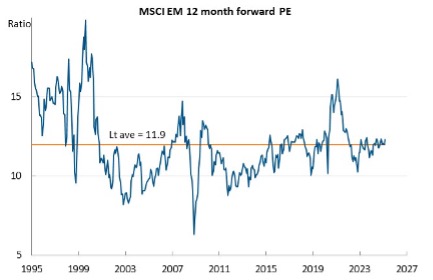

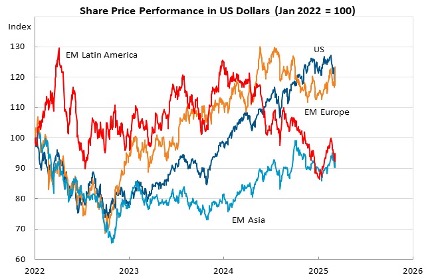

The size of US tariff increases on China is the key issue for EM equities. Once US tariffs rise, we expect Chinese au The US raised its tariffs on Chinese goods by 20% after China retaliated to the initial 10% tariff. Over the weekend, China announced policies designed to lift consumer spending via means such as childcare subsidies, housing reform, an increase in the aged pension, and an expansion of tourism. There wasn’t much detail at this stage, but history shows that announcements like these materialise and hit their target over time. EM equities have also been supported by the recent weakness of the US dollar, but more will be needed if the asset is to outperform.