Summary

The latest Australian corporate reporting season has unfolded in parallel with Treasurer Jim Chalmers’ productivity summit, creating a timely backdrop to assess how businesses are tackling productivity challenges. While the summit was held behind closed doors, corporate results have been publicly scrutinised, revealing a diverse mix of successes, stumbles, and strategic shifts.

Productivity has emerged as a central theme for many companies. As long-term economic growth projections remain subdued, businesses are seeking internal efficiencies and strategic investments to boost output.

SGH boss Ryan Stokes encapsulated this shift, asserting that productivity is primarily the responsibility of business, not government. His point was backed by the turnaround at Boral, now a profit engine for SGH after improvements in capital allocation and pricing discipline.

Many companies, including AGL, CBA, BHP, Origin, and Telstra, are increasing capital expenditure. This investment is carefully directed at low-risk, strategic projects—like CBA’s tech and AI initiatives or Telstra’s network upgrades rather than speculative ventures. The focus is on sustainable, manageable growth that still delivers dividends, which remain a priority for investors.

Retail has also surprised on the upside, buoyed by stabilising inflation, tax cuts, and multiple interest rate reductions, which have restored household spending power. A chart from CBA highlighted a rare moment where all age groups are simultaneously increasing spending across essentials, discretionary items, and savings. This consumer resurgence has boosted companies like Nick Scali, Baby Bunting, and Super Retail, all of which reported stronger-than-expected results.

Leadership quality has also come under the spotlight. Good management is being recognised and rewarded, while even well-planned successions can cause temporary jitters. JB Hi-Fi shares, for example, dipped after popular CEO Terry Smart announced his retirement, though they later recovered. Conversely, REA Group was positively received after naming Cameron McIntyre as its new CEO, a move seen as strategic and aligned with the business. Investors also continue to back seasoned leaders like Breville’s Jim Clayton, who is navigating tariff challenges with confidence.

However, poor strategic decisions have not escaped punishment. CSL’s plan to spin off its Seqirus vaccine division without a compelling rationale confused investors, contributing to a 20% share price fall. Similarly, James Hardie’s $14 billion acquisition of Azek has backfired, with underwhelming early sales and mounting debt leading to a 28% drop in its stock price. Both cases underscore the risks of straying from core competencies or misjudging market timing.

Finally, lofty expectations have created volatility. Market darlings like CBA and Guzman y Gomez (GYG) were penalised for merely meeting, rather than exceeding, expectations. CBA delivered a solid $10.3 billion profit but still fell 6% due to its premium valuation. GYG plunged nearly 20% after failing to excite with its growth numbers. With Qantas due to report next, its own high-flying share price may leave little room for a mediocre result.

Overall, the season reflects a market that values prudent investment, disciplined execution, and strong leadership but punishes missteps and overreach swiftly.

Caution Warranted

August’s corporate reporting season has boosted Australian share prices, but broader trends suggest caution. While earnings have helped lift equity markets, including Australia’s, analysts are beginning to question the sustainability of this momentum. As a result, some asset managers have tactically reduced exposure to Australian equities, shifting to an underweight position relative to strategic benchmarks.

Although the ASX has delivered solid returns, up 11.8% over the year to July, with three- and five-year averages around 12%, it lags behind global markets. The MSCI All Countries World Index ex-Australia, driven largely by US equities, has significantly outperformed, with annualised returns exceeding 16% over five years.

One key issue is the composition of the Australian market, which is heavily concentrated in financials (35%) and materials (23%), with only 4% exposure to information technology — far behind the US S&P 500, where tech makes up 34%. This imbalance limits growth potential.

Commonwealth Bank (CBA) has driven much of the ASX 200’s performance, contributing 40% of gains this year with a 22% return. Yet, CBA trades at a global premium that many see as unjustified, especially compared to higher-growth international banks.

Meanwhile, many of Australia’s top companies are choosing to list overseas to access higher valuations and growth-focused investors. The US market, for instance, prioritises total return and reinvestment over dividends, while Australia’s system favours high payouts due to franking credits.

Long-term challenges for Australia include stagnant productivity, overregulation, high government spending, and rising energy costs. Despite these headwinds, opportunities exist in underperforming mid-caps, tech, utilities, and globally focused companies. Active stock selection and sector rotation within the ASX 200 will be essential as the broader index shows little growth potential through 2027, according to Capital Economics forecasts.

The big picture

This season was classic “two speeds”: companies with pricing power, structural tailwinds or cost discipline largely delivered, while those exposed to weak discretionary spend or regulatory/reputational headwinds struggled. Results also showed an economy easing but still resilient: travel stayed buoyant, digital advertising improved off stronger listing/activity cycles, and energy utilities benefited from cash generation and capital returns. In contrast, supermarkets diverged sharply, select tech names missed investor hopes despite growth, and healthcare was rocked by one blockbuster move.

Dominant themes emerging so far

- Earnings quality over earnings quantity. The market rewarded companies that paired topline with margin discipline and clear capital-allocation (REA’s dividend uplift; Telstra buyback; Origin’s higher payout). Where beats relied on heavy cost-out or where guidance implied a slower cadence (WTC), multiples compressed.

- Capital returns are back—selectively. Special or higher ordinary dividends and buybacks signalled confidence (QAN, TLS, ORG). Investors differentiated between one-off returns funded by disposals versus sustainably higher free cash flow.

- Operational execution beats macro. Supermarkets proved execution matters more than category: Coles’ automation/utilisation progress versus Woolworths’ remediation underscored this. In tech, REA’s playbook of pricing + depth + data won out, while WiseTech’s reset showed the cost of falling short against high bars.

- Energy transition is investable—but uneven. Origin’s balanced portfolio and project pipeline drew positive reactions; AGL’s bigger renewables/storage target arrived alongside profit volatility—message received, but show-me execution next.

- Strategic surgery changes narratives. CSL’s Seqirus demerger proposal was the season’s boldest pivot; it may unlock focus and value longer-term, yet introduces short-term uncertainty and index-flow considerations.

Sector breakdown & key trends

Consumer staples (supermarkets & liquor)

- Woolworths (WOW): A shocker. FY25 profit fell ~17–19% with softer-than-expected sales momentum into the new year; margins compressed as it cut prices to rebuild trust. Shares slumped double digits, the dividend was trimmed, and commentary flagged ongoing drags (e.g., tobacco). Execution and reputation repair remain the to-do list.

- Coles (COL): A relative winner. Coles reported profit growth and better supermarket trends, helped by automation in new distribution/fulfilment centres and solid own-brand performance. It still faces shrink/theft pressure, but momentum and execution looked steadier than its rival.

Takeaway: Same sector, two stories: WOW is in rehab mode; COL is grinding out efficiency-led gains. Pricing, promo cadence and trust dynamics will remain decisive over FY26.

Consumer discretionary & travel

- Qantas (QAN): Travel demand stayed robust. Qantas posted ~$2.4bn underlying profit (+15% YoY) with strength across Domestic, International and Jetstar; the market cheered cap-return (special dividend) and fleet/in-product investment signals. Debt ticked up with reinvestment.

- Broader discretionary was mixed (not all majors reported on the same day). Where brands had clear value propositions or could cycle promotions cleanly, results held up; where inventory, rents or wages pinched, the P&L showed it.

Takeaway: Travel still has altitude; the rest of discretionary is a stock-picker’s field, sensitive to wage/lease pressures and price elasticity.

Technology & online platforms

- REA Group (REA): A stand-out. FY25 revenue +15%, EBITDA +18%, NPAT +23%, with a hefty dividend uplift. Strength reflected pricing, depth products and solid Australian listing activity, plus progress offshore (REA India).

- WiseTech (WTC): Grew revenue (~14%) and profit (~17%), but missed elevated expectations; shares fell as guidance and the cadence under a new CEO reset sentiment. The long-term logistics digitisation thesis remains intact, but FY25 reminded investors how tightly valued names need to deliver.

- Media/Comms: Nine (NEC) reported revenue of ~$2.7bn and positive NPAT with a confident outlook commentary, aligning with signs that ad markets are stabilising.

Takeaway: Platforms tied to real-economy cycles (property, logistics) grew, but the market punished any wobble versus lofty expectations. Quality, recurring revenue and disciplined guidance were prized.

Healthcare & biotech

- CSL (CSL): The season’s headline. CSL posted a solid profit increase but unveiled plans to demerge Seqirus (flu vaccines) as a substantial standalone ASX listing by FY26; shares dropped sharply as investors focused on weaker Behring performance and the uncertainty of a carve-out. Strategically, CSL is simplifying its portfolio, but execution risk and timing will be watched closely.

Takeaway: Big strategic moves can swamp the print. CSL’s demerger narrative now becomes a key FY26 watch-item for sector leadership and index flows.

Energy & utilities

- Origin (ORG): Delivered a stronger statutory profit (~A$1.48bn), raised dividends, and guided to improved retail earnings into FY26, with batteries (Eraring, Mortlake) progressing. Shares hit decade highs on the outlook. LNG trading and integrated gas helped offset softer retail energy earlier in the year.

- AGL (AGL): Reported FY25 with a lower earnings base, lifted total dividends to 48c, and set FY26 guidance. It also sharpened decarbonisation goals (6GW renewables/storage by 2030) amid operational noise; investor reaction was mixed given earnings sensitivity to outages and pricing.

- Santos (STO): Industry backdrop featured corporate overhang—Santos flagged another extension to due diligence on ADNOC’s proposed ~$30bn bid while reporting softer profit on lower commodity prices.

Takeaway: Cash generation allowed utilities to pay and invest at the same time; transition capex remains a feature. M&A optionality (Santos) and policy settings continue to matter for valuation.

Telcos

- Telstra (TLS): Full-year commentary emphasised underlying growth, higher mobile ARPU, cost control and shareholder returns (dividend at 19c, buyback). Hikes earlier in the year supported earnings trajectory.

- TPG Telecom (TPG): A “transformative” year as the Optus regional network-sharing deal added ~100k customers and lifted mobile momentum; guidance was reiterated after asset sales reshaped the group toward a mobile-led profile.

Takeaway: Industry structure is more rational; mobile price discipline and network-sharing economics underpinned improving cash returns.

Industrials & transport infrastructure

- Airports & toll roads were less prominent this fortnight, but traffic-linked names broadly reported steady volumes into winter. The marquee result was Qantas, which captured the “still-travelling” consumer and rewarded holders.

Materials & resources

- Iron ore majors straddle off-cycle dates (Rio reported in July; others later in August), but investor focus remained on payout discipline versus capex pipelines and China pulse checks. Lithium-exposed names continued to wrestle with price resets into the prints. (Broader trend commentary; major specifics varied by name.)

Here’s a refined ~300-word summary on notable small-cap ASX stocks from the August 2025 reporting season—covering standout results, broader small-cap trends, and strategic takeaways.

Broader Small-Cap Landscape & Trends

- Mixed outcomes, with around 20–30 small caps receiving attention this reporting season based on observations from specialist small-cap coverage.

- Earnings surprises at the small-cap end are less about macro trends and more rooted in operational execution and growth clarity.

- Analysts warn that stretched valuations across the broader ASX heighten the risk for small caps—especially where guidance or margins underperform.

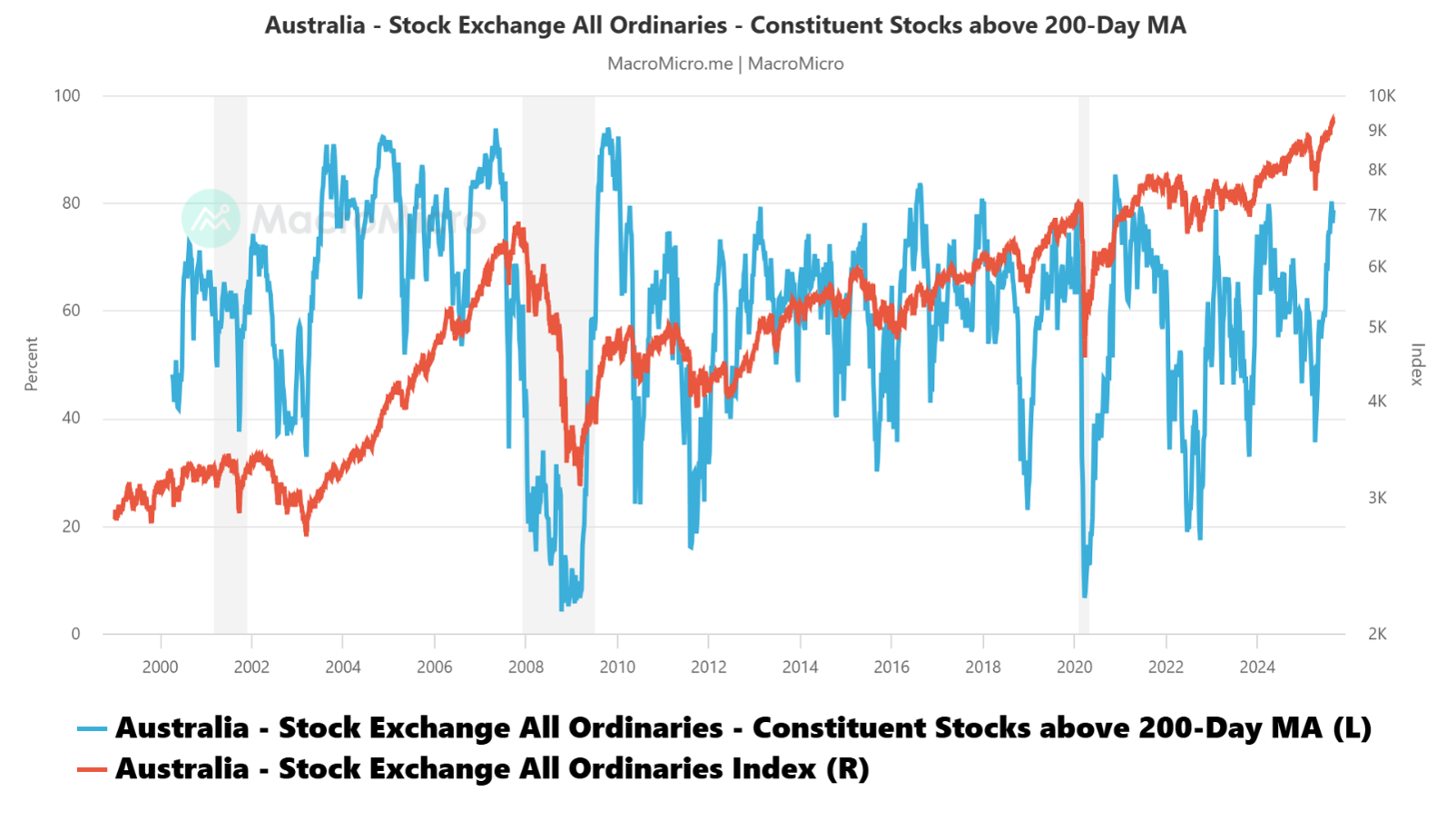

Exhibit 1: Australian Equity Performance – % of Stocks above 200 Day Moving Average Price