Summary: RBA raises GDP forecasts to June 2022, lowers forecasts further out; underlying inflation forecasts raised; jobless rate expected to fall to 4% by June; headline inflation forecasts increased noticeably in years to June, December 2022, later periods also raised.

The Statement on Monetary Policy (SoMP) is released each quarter and it is closely watched for updates to the RBA’s own forecasts.

In November’s SoMP, the opening sentence of the “Outlook” section stated, “The ongoing rollout of vaccinations and significant policy stimulus has laid the groundwork for a sustained economic recovery.”

As far as Australia was concerned, “Economic activity in Australia contracted sharply in the September quarter…This setback has delayed but not derailed the economic recovery that was underway in the first half of the year.”

February’s Outlook opened with “Global economic growth picked up in the second half of 2021 following the lifting of mobility restrictions and is forecast to remain above trend in 2022. The rapid spread of the Omicron variant of COVID-19 has been disruptive but is not anticipated to have a large or sustained impact on growth. Inflation in many countries has persisted at multi-year highs and has broadened in scope.”

On domestic matters, it stated, “The Australian economy had established solid momentum prior to the Omicron outbreak at the end of 2021. Domestic economic activity bounced back strongly in the December quarter, driven by a surge in household spending as restrictions relating to the Delta outbreak were eased.”

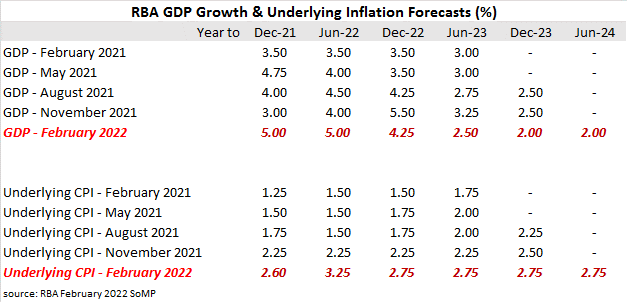

The RBA’s GDP growth forecast for the year to December 2021 (see table below) has been raised by 2.00 percentage points and the forecast for the year to June 2022 has been raised by 1.00 percentage point. However, the growth rate for the year to December 2022 had been lowered by 1.25 percentage points while growth rates for the years to June 2023 and December 2023 have been decreased by 0.75 percentage points and 0.50 percentage points respectively. According to the RBA, Australia is expected to grow at sub-trend rates in the years to June 2023, December 2023 and June 2024.

The GDP growth rate for the forecast period to the end of June 2022 has been raised despite the RBA’s expectation coronavirus infections will be “drag on growth in economic activity during early 2022.” Consumption, by far the largest component of GDP, “is forecast to be supported by strong labour income growth and the large increase in household wealth over recent years.” Dwelling investment is expected “to remain elevated across the forecast period” while business investment is expected to continue its recovery. Government budgets “point to a stronger outlook for public demand than was previously expected” but the current account (imports/exports) “is forecast to drag on growth…”

The RBA’s underlying inflation forecast for the year to June 2022 was raised by 1.00 percentage points while forecasts for the years to December 2022 and June 2023 were each raised by 0.50 percentage points. The forecast for the year to December 2023 was raised by 0.25 percentage points.

Six months ago in the August SoMP, the RBA referred to underlying inflation as having “stabilised”, with the expectation at the time of it remaining “subdued over the next few quarters, given the decline in activity in the September quarter and the absence of broad-based inflationary pressures.”

However, trimmed-mean inflation actually accelerated in the September and December quarters and the RBA now expects “upstream cost pressures” and “a steady pick-up in labour costs in response to strong labour market conditions…to sustain inflation in the top half of the 2% to 3% target range.”

Some economists think the RBA is “behind the curve” when it comes to inflation. “Westpac expects that the Bank’s forecast that supply side pressures will ease markedly by mid-year is somewhat optimistic. We are forecasting that underlying inflation will hold around 3.6% in both June and September quarters and headline inflation will hold around 4.2% prior to slowing in the December quarter,” said Westpac Chief Economist Bill Evans.

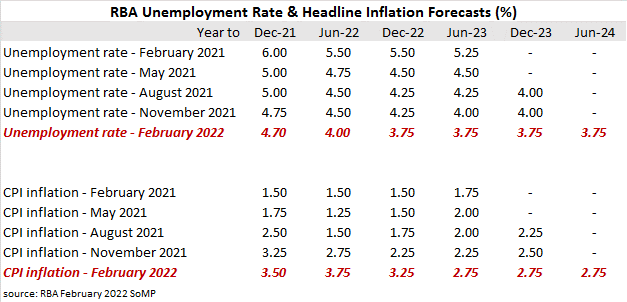

The RBA’s view of the unemployment rate typically follows from its forecasts of GDP growth. The unemployment rate peaked at 7.4% in June 2020 but it has since fallen to 4.2% at the end of December. The RBA now expects it to decline to 4.0% by the end of June and then to 3.75% by the end of 2022. The forecasts then remain unchanged over the remainder of the forecast periods.

“Employment is forecast to grow strongly over the remainder of 2022 before moderating in 2023 in line with growth in activity. Participation in the labour force is forecast to be at a historically high level over the forecast period, supported by the strength in labour market conditions.”

Average hours worked is expected to decline and “bear most of the adjustment to labour supply” in the March quarter but “the spread of omicron is expected to have no lasting impact on labour demand.”

Headline inflation forecasts again have been increased noticeably in the years to June 2022 and December 2022 while forecasts for the years to June 2023 and December 2023 have also been raised by 0.50% percentage points and 0.25 percentage points respectively.

“Headline inflation is forecast to be above trimmed-mean inflation in the near term, mainly due to fuel prices, but to be broadly in line with underlying inflation thereafter.” The RBA referred to “upstream cost pressures, including those caused by temporary disruptions to domestic supply chains” as factors likely to “significantly” boost inflation.

Commonwealth bond yields moved significantly higher on the day of the Statement’s release, outpacing the movements of their US Treasury bond yields overnight. By the end of the day, the 3-year ACGB yield had jumped 8bps to 1.45%, the 10-year yield had gained 9bps to 1.98% while the 20-year yield finished 11bps higher at 2.45%.

“The key takeaways remain that (1) the RBA is “prepared to be patient” (2) there is no strict definition for “sustainably higher inflation” and (3) The RBA’s upgraded inflation forecasts in our opinion remain exposed to upside risk in the near term,” said NAB economist Taylor Nugent.