Summary: RBA leaves GDP forecasts unchanged; underlying inflation forecasts rise again; jobless rate expected to rise modestly later this year; some headline inflation forecasts increase, others cut; ANZ: RBA “less confident” regarding normalisation of speed underlying inflation.

The Statement on Monetary Policy (SoMP) is released each quarter and it is closely watched for updates to the RBA’s own forecasts.

In November’s SoMP, the opening sentence of the “Outlook” section stated, “The prospects of a significant slowing in the global economy have intensified over the past three months, fuelled by persistently high inflation and rising policy rates, the energy crisis in Europe, and the various headwinds affecting China’s recovery.”

As far as Australia was concerned, “The Australian economy is forecast to grow solidly over the second half of 2022, before slowing next year as higher consumer prices, rising interest rates and declining housing prices weigh on growth.”

February’s Outlook opened with “Global growth is forecast to remain well below its historical average over the next two years.”

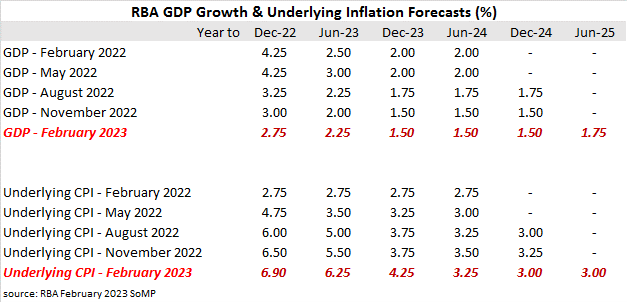

On domestic matters, it stated, “The outlook for GDP growth is little changed from three months ago.”

Accordingly, the RBA’s GDP growth forecasts have not changed for any of the periods out to December 2024 (see table below). Sub- trend GDP growth is still expected by the RBA to continue in the periods which now include the year to June 2025.

“While the incoming data on domestic demand for the second half of 2022 was a little weaker than expected, the overall implications for the growth outlook have been broadly offset by stronger population growth, which is being driven by higher net overseas arrivals.”

The RBA’s underlying inflation forecast have been raised again in the years to June 2023 and December 2023. The forecast for the year to June 2023 was raised by 0.75 percentage points while the forecast for the year to December 2023 was raised by 0.50 percentage points. However, the RBA has also trimmed it forecasts for subsequent periods each by 0.25 percentage points.

“The near-term outlook for underlying inflation has been revised higher as a result of the stronger-than-expected December quarter underlying inflation outcome and an upward revision to labour costs.”

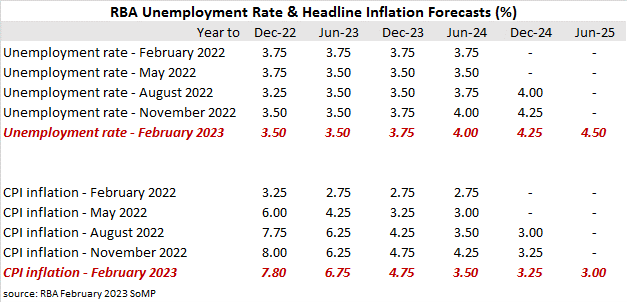

The RBA’s view of the unemployment rate typically follows from its forecasts of GDP growth. The unemployment rate had fallen to 3.50% at the end of December 2022 and the RBA now expects it to remain steady until the second half of 2023 when it is forecast to rise to 3.75%. Further modest increases are then expected in the subsequent periods.

“The labour market is very tight; the recent pick-up in net arrivals following the reopening of the international border has supported robust growth in employment and is helping to alleviate shortages in some areas.”

The headline inflation forecast for the current financial year has been increased by 0.50% but the forecast for the year to June 2024 has been reduced by 0.75%.

“The easing in global price pressures already underway is expected to flow through to domestic prices over time. In addition, slower growth in domestic demand and a moderation in labour market conditions are expected to reduce domestic inflationary pressures.”

Commonwealth bond yields moved higher, especially at the short end. By the end of the day, the 3-year ACGB yield had gained 8bps to 3.43% while 10-year and 20-year yields both finished 4bps higher at 3.72% and 4.08 respectively.

“The RBA’s forecast for trimmed mean inflation is 4.3% in Q4 2023, up 0.5 percentage points from the previous forecast of 3.8%. This suggests the RBA are less confident than before about the speed at which underlying measures of inflation will normalise,” said ANZ economist Adelaide Timbrell.