Summary: GDP forecasts raised significantly; inflation expected to be somewhat higher; jobless rate past peak, expected to continue fall steadily over 2021, 2022; Westpac’s Evans expects more QE.

The Statement on Monetary Policy (SoMP) is released each quarter and it is closely watched for updates to the RBA’s own forecasts.

In November’s SoMP, the opening statement of the “Outlook” section stated, “Following the largest contraction in decades, the global economy is in the early stages of recovery, as is Australia.”

February’s Outlook also opened with a general comment on the global economy. “The outlook for the global economy has improved since the November Statement on Monetary Policy.” It then turned to domestic matters. “The recovery in the domestic economy has been sustained over recent months, supported by better health outcomes and a further expansion in monetary and fiscal policy in the second half of last year.

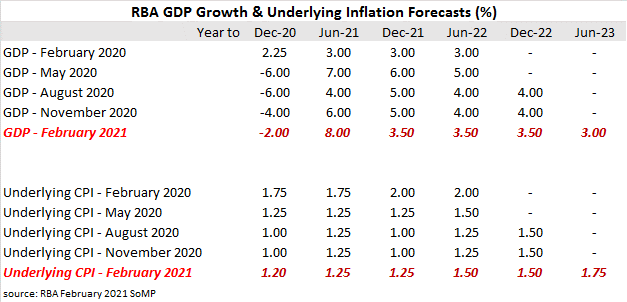

GDP growth rates in the early periods of the forecasts have been raised significantly while later periods’ forecasts have been reined in moderately. The RBA’s forecast GDP growth rate for the year to June 2021 (see table) has been increased by another 2.0% but the following financial year (June 2022) has been trimmed by 0.50% back to 3.50%. The RBA had previously expected a “gradual recovery” but now it expects GDP to reach it pre-pandemic level “over the course of 2021, around 6–12 months earlier than previously expected.”

The RBA’s underlying inflation forecasts have been raised modestly in the 2022 financial year but otherwise they are not all that different. The RBA’s favoured measure of underlying inflation, the “trimmed mean”, turned out to be a little higher in the December quarter than previously expected but it has resisted any pressure to raise its forecasts more than the modest increases made to the year to December 2021 and the year to June 2022. “Spare capacity in the labour market is expected to remain elevated over the forecast period, and both wages growth and underlying inflation are expected to remain below 2.0%.”

The RBA’s underlying inflation forecasts have been raised modestly in the 2022 financial year but otherwise they are not all that different. The RBA’s favoured measure of underlying inflation, the “trimmed mean”, turned out to be a little higher in the December quarter than previously expected but it has resisted any pressure to raise its forecasts more than the modest increases made to the year to December 2021 and the year to June 2022. “Spare capacity in the labour market is expected to remain elevated over the forecast period, and both wages growth and underlying inflation are expected to remain below 2.0%.”