Recent Patterns

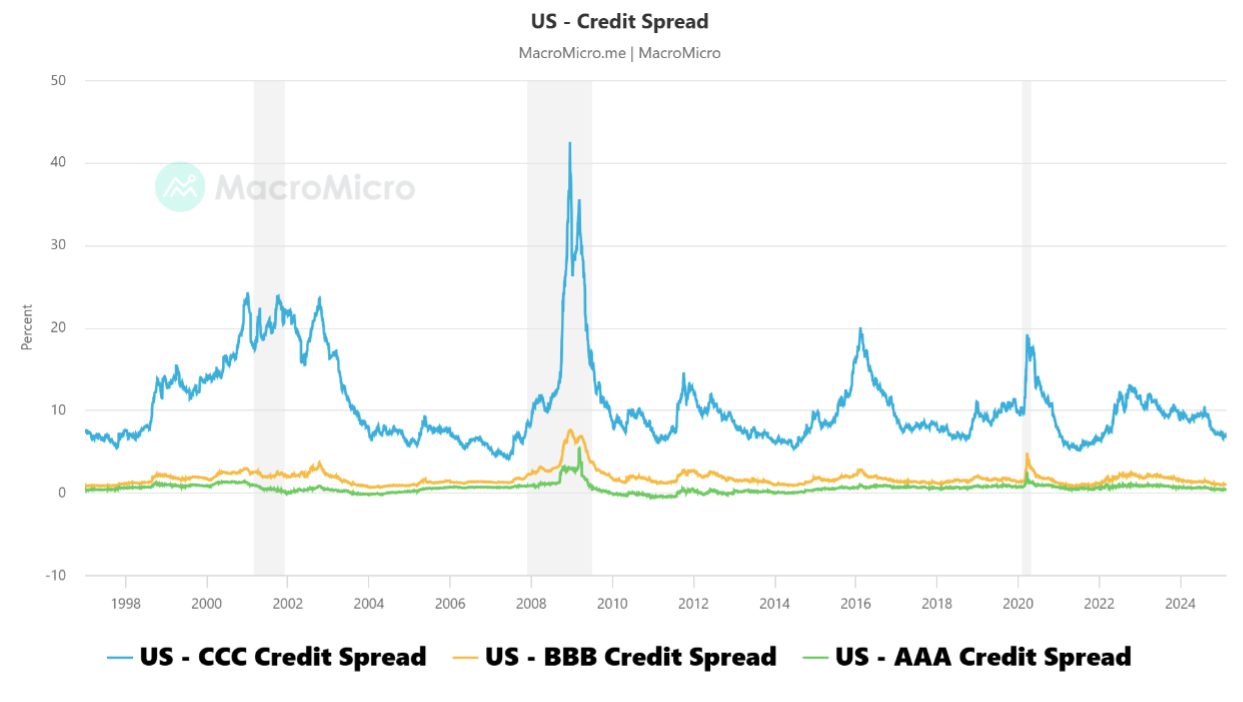

US corporate bonds are seeing less price movement than Treasuries, making the securities in some sense safer than their government counterparts, an unusual turn of events that seems to be stoking high valuations (historically low spreads) for company debt.

Since its mid-January high of 4.8%, the US 10-year treasury note has fallen by more than 50 basis points. Not only that, the decline has also been a story of whiplash. In contrast, US corporate bonds, both IG and HY, have been a relative sea of calm. While spreads are at near historical lows, investors are all in on yields, rationalising that the yields, tied with strong fundamentals and technicals, are attractive enough to more than offset any perceived probable risk of spread widening.

Yes, there are cyclical factors at play regarding balance sheet strength and earnings outlook. But more importantly, there are multi-year structural factors that have shaped the IG and HY markets. Both are combining to suggest that 2025 may indeed be the year of bonds. And guess what? Inverse correlations between bonds and equities have been back for 6-months now after having been absent, effectively, for over 20-years since the beginning of 2003.

Strong Fundamentals (aka, Credit Risk)

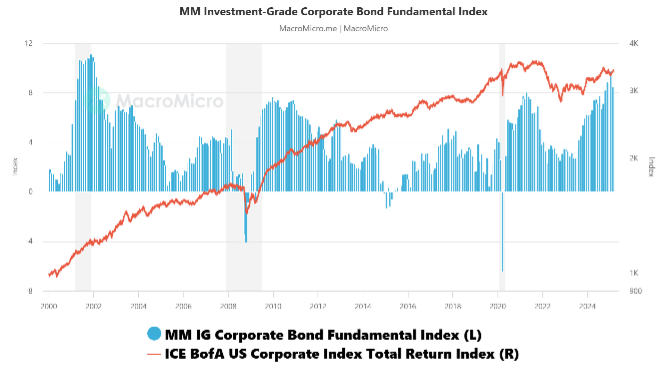

On the whole, US corporates have engaged in balance sheet improvement since the pandemic. Credit quality improved in 2024 on margin expansion and stabilizing leverage. The IG issuer trimmed mean EBITDA margin in 2024, approaching 31%, is higher than over the last 10-years. Leverage has stabilized at the higher end of the range but is low on a net basis due to high cash.

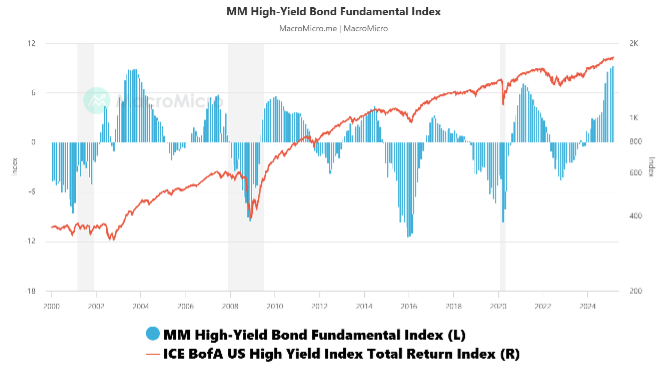

Within the high yield spectrum, the fundamentals of high yield have been converging up to meet their investment grade peers in certain subsets. That is, the fundamentals are strong, particularly the BB portion. Defaults remain below long-term averages, with a continued decline in the US high yield bond default rate to a three-year low of 1.5% by 2024 year-end. The fact that leverage has not meaningfully picked up and interest coverage has experienced only mild deterioration from its highs in 2021-2022 is testament to the resourcefulness that many high yield companies have shown in adapting to a higher interest rate environment.

But structurally, both the IG and HY markets have been migrating up the credit ratings spectrum. In IG, Triple B’s are at a much lower percentage than it used to be while single A’s have increased. In HY, today’s market consists of 53% in BBs, compared to 38% pre–Global Financial Crisis. The transition to higher quality credit has been a multi-year dynamic, with lower quality credits generally transitioning to either private credit and/or leveraged loans. Additionally, due to the rapid growth of private credit, today’s high yield market is also composed of public companies to a much greater extent, increasing overall transparency as to balance sheet health due to more stringent reporting requirements for public companies.

| Exhibit 1: IG Corp Bond Fundamental Index |

| Exhibit 2: HY Corp Bond Fundamental Index |

The Technicals – Supply vs Demand

The technicals in corporate debt are particularly strong. This is despite spreads being exceptionally tight. But there a several key reasons why spreads are historically tight and likely to remains so.

Firstly, the liquidity of the bond market is better than it’s ever been. The invention of the portfolio trade, the easy way to move baskets of bonds back and forth between investors and dealers and ETFs has enhanced liquidity and reduced the enhanced premium that investors need to own credit.

Secondly, as noted above, credit quality is higher than it’s ever been or better than it’s been recently, and particularly at the lower end of the market.

Thirdly, the duration of the bonds is significantly shorter than it has been in the past and by about two years. The shorter the bonds, the less spread an investor should require in order to be compensated out of treasuries.

We note that calls for wider high yield spreads in 2024 did not materialise, just as in 2023. Although there’s no denying spreads are tight relative to long-term averages, an argument can be made that they remain justifiably expensive – given the benign default rate and strong fundamental and technical environment. With these trends still very much in play, there are reasons why spreads remain supported at current levels and why any widening due to macro or geopolitical events could be viewed as a potential buying opportunity. In fact, due to the structural shifts in the corporate bond market, you could make an argument that the average spread over the next 15 years may well be lower than the previous 15 since the GFC.