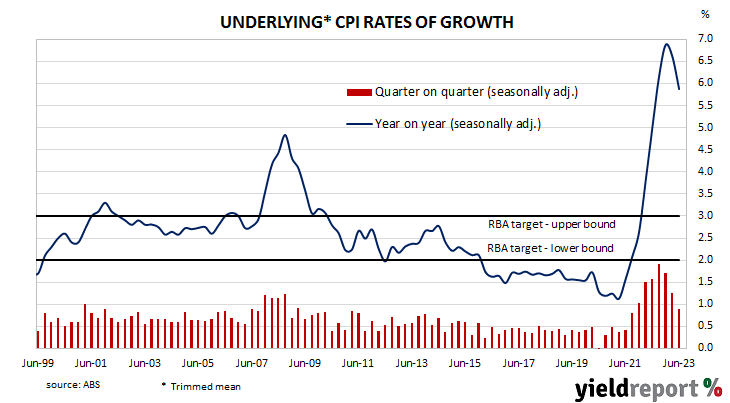

Summary: Annual Inflation rate slows to 6.1% in June quarter, below expectations; RBA preferred measure slows from 6.6% to 5.9%; food, non-alcoholic beverage prices main drivers of result.

In the early 1990s, high rates of inflation in Australia were reined in by the “recession we had to have” as it became known. Since then, underlying consumer price inflation has averaged around 2.5%, in line with the midpoint of the RBA’s target range. However, the various measures of consumer inflation trended lower during the decade after the GFC and hit a multi-decade low in 2020 before rising significantly in the quarters following September 2021.

Consumer price indices for the June quarter have now been released by the ABS and the seasonally-adjusted inflation rate posted a 0.9% rise. The result was below consensus expectations of a 1.1% rise as well as the March quarter’s 1.3% increase. On a 12-month basis, the seasonally-adjusted rate slowed from 7.0% after revisions to 6.1%.

The RBA’s preferred measure of underlying inflation, the “trimmed mean”, increased by 0.9% over the quarter, less than the 1.1% increase which had been generally expected as well as the March quarter’s 1.3% rise. The 12-month inflation rate slowed from 6.6% to 5.9%.

Domestic Treasury bond yields generally moved lower on the day following similar movements of US Treasury yields overnight. By the close of business, the 3-year ACGB yield had shed 7bps to 3.89%, the 10-year yield had lost 2bps to 4.01% while the 20-year yield finished 1bp higher at 4.28%.

In the cash futures market, expectations regarding further rate rises softened. At the end of the day, contracts implied the cash rate would rise from the current rate of 4.07% to average 4.135% in August and then to 4.175% in September. February 2024 and May 2024 contracts both implied a 4.32% average cash rate, 25bps more than the current rate.

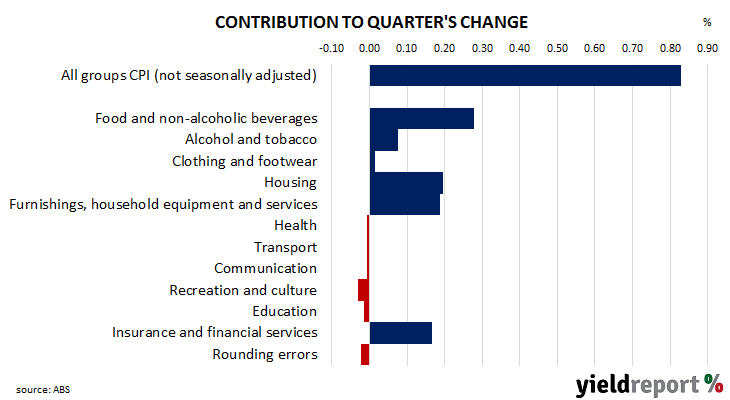

The main driver of the headline inflation figure in the quarter was a 1.6% rise in food and non-alcoholic beverages prices, contributing just under 0.30 percentage points of the 0.8% (unadjusted) increase. Housing costs and prices of furnishings and household equipment also had noticeable influences on the quarter’s reading, each contributing around 0.20% percentage points to the quarterly total.

Here’s what a few economists said about the figures:

Adelaide Timbrell, ANZ

The RBA recently highlighted that the cash rate is “clearly restrictive” and that it remained to be seen if more cash rate increases are required. The sharp drops in headline and core CPI and in non-tradables and services inflation, the latter two both printing 0.8% in Q2, highlight that a 4.1% cash rate may be restrictive enough to bring inflation down. This is particularly the case given monetary policy operates with a considerable lag.

Faraz Syed, Citi

The Q2 CPI report showed that inflation remains sticky; with both headline and underlying inflation running at 6% and 5.9%, respectively. Although this was a downside miss versus consensus and the RBA’s forecast, it was largely driven by some volatile items and administrative prices that fell because of subsidies.

Services inflation continues to accelerate and this is evidenced across a variety of household categories such as rents or personal services. Wages growth could continue to fuel further pick-up in services inflation in H2.

Chris Read, Morgan Stanley Australia

More broadly, there continues to be a divergence across goods and services inflation trajectories with the latter now higher for the first time since mid-2021. Rents remain an important driver of this services strength and increased to the highest annual rate since 2009. The slower quarterly pace in this print suggests a clear path for headline inflation to ease over 2H23, although we see less scope for sequential slowing in core inflation over the same period, given rent, wage and electricity inflation are all likely to be higher over this period.

Justin Smirk, Westpac

The more modest-than-expected rise in the headline and core measures highlight disinflationary forces greater than we had thought. So, it is clear that while we continue to see most prices continuing to rise, many of these increases continue to get smaller than they have been in recent quarters.