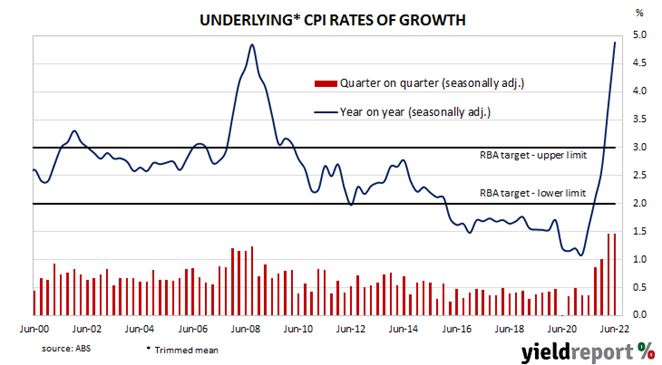

Summary: Annual Inflation rate accelerates to 6.1% in June quarter, in line with expectations; RBA preferred measure rises from 3.7% to 4.9%; housing, food, transport costs again main drivers of result.

In the early 1990s, high rates of inflation in Australia were reined in by the “recession we had to have” as it became known. Since then, underlying consumer price inflation has averaged around 2.5%, in line with the midpoint of the RBA’s target range. However, the various measures of consumer inflation trended lower during the decade after the GFC and hit a multi-decade low in 2020 before rising significantly in the quarters following the September 2021 quarter.

Consumer price indices for the June quarter have now been released by the ABS and the seasonally-adjusted inflation rate posted a 1.7% rise. The increase was basically in line with expectations but less than the March quarter’s 2.1% rise. On a 12-month basis, the seasonally-adjusted rate accelerated from 5.2% to 6.1%.

The RBA’s preferred measure of underlying inflation, the “trimmed mean”, increased by 1.5% over the quarter, in line with market expectations and the March quarter’s rise. The 12-month inflation rate rose from 3.7% to 4.9%.

Commonwealth Government bond yields dropped significantly on the day. By the close of business, the 3-year ACGB yield had shed 13bps to 3.04%, the 10-year yield had lost 9bps to 3.28% while the 20-year finished 10bps lower at 3.53%.

In the cash futures market, expectations of a less steep path for the actual cash rate over time gained ground. At the end of the day, contracts implied the cash rate would rise from the current rate of 1.31% to 1.76% in August and then increase to 2.97% by November. May contracts implied a 3.44% cash rate while August 2023 contracts implied 3.365%.

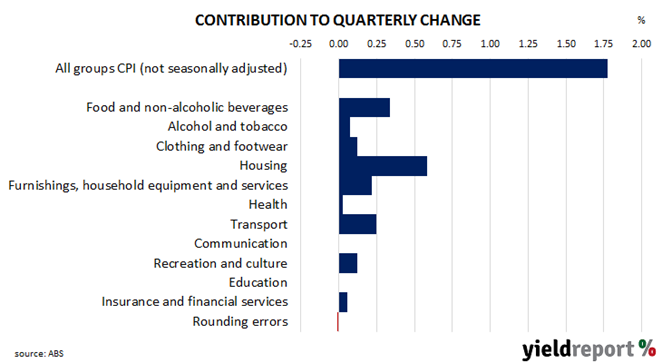

The main driver of the headline inflation figure in the quarter again was a 2.5% rise in housing costs, contributing 0.58 percentage points of the 1.78% (unadjusted) increase. Food and beverage prices also had a significant influence on the quarter, rising by 2.0% and contributing 0.58% percentage points to the quarterly total. Transport prices rose by 2.3% and contributed 0.25 percentage points.

Here’s what a few economists thought about the figures:

Catherine Birch, ANZ

It looks like we’re moving past the peak in quarterly inflation, but it’s a high peak to come down from, with the quarterly result annualising at 7.4% for headline and 6.1% for trimmed mean. This doesn’t change our view on the RBA’s near-term meetings, where we expect 50bps hikes. The target cash rate is still well below the RBA’s estimates of neutral and we expect the labour market to continue tightening. This will prompt the RBA to take the cash rate above the lower bound of what it deems the neutral range.

Chris Read, Morgan Stanley Australia

We continue to expect inflation to rise further in coming quarters, peaking in Q4 at 7.4%. The majority of current inflation is still in goods with services inflation relatively more contained, but we expect this will change in coming quarters, particularly after the wage acceleration that is likely given the minimum wage increase and further acceleration in rents which remain at low levels. Additionally, the sharp increase in utilities costs will also put upward pressure on headline inflation through 2H22.

Justin Smirk, Westpac

The impact of HomeBuilder grants was there but it is less significant than in recent history. The more important story now for new dwelling inflation is the shortages of building supplies and labour, heightened freight costs and strong demand; these factors are also significant for the broader inflationary pulse we are now observing.

Josh Williamson, Citi

To us, this suggests that while inflation pressures are increasing in Australia, they are not as strong as in some other developed countries. Importantly, it means that the RBA should not need to lift the official cash rate as quickly or as high as some other central banks, particularly the US Fed.