29 January 2025

Summary: Headline inflation up 0.2% in Sep quarter, less than expected; annual rate of RBA preferred measure slows from 3.6% to 3.2%; ACGB yields fall; rate-cut expectations firm; recreation/culture prices main driver of result.

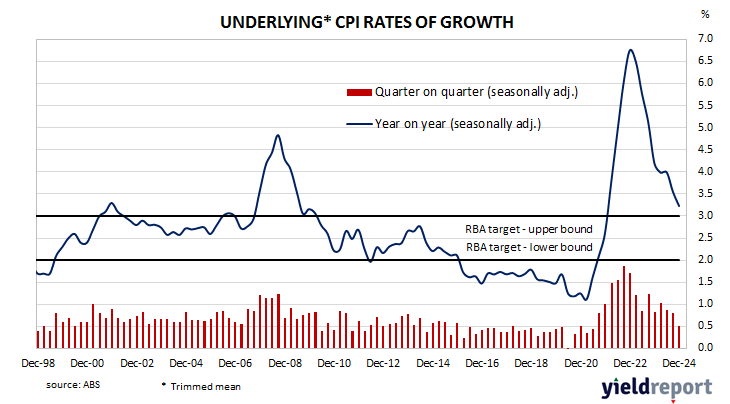

In the early 1990s, high rates of inflation in Australia were reined in by the “recession we had to have” as it became known. Since then, underlying consumer price inflation has averaged around 2.5%, in line with the midpoint of the RBA’s target range. However, the various measures of consumer inflation trended lower during the decade after the GFC and hit a multi-decade low in 2020 before rising significantly in the quarters following September 2021.

Consumer price indices for the December quarter have now been released by the ABS and the “headline” inflation rate came in at 0.2% before seasonal adjustments. The result was less than 0.4% rise which had been generally expected but in line with the September quarter’s increase. On a 12-month basis, the inflation rate slowed from 2.8% to 2.4%.

The RBA’s preferred measure of underlying inflation, the “trimmed mean”, increased by 0.5% over the quarter, slightly less than the 0.6% increase which had been generally expected and down from the 0.8% in the September quarter. The 12-month inflation rate slowed from 3.6% after revisions to 3.2%.

Domestic Treasury bond yields fell moderately across a slightly flatter curve on the day, in contrast with the modest rises of US Treasury yields on Tuesday night. By the close of business, the 3-year ACGB yield had shed 6bps to 3.78%, the 10-year yield had lost 5bps to 4.40% while the 20-year yield finished 4bps lower at 4.83%.

Expectations regarding rate cuts in the next twelve months firmed, with a February 2025 rate cut viewed as highly likely. Cash futures contracts implied an average of 4.255% in February, 3.92% in May and 3.645% in August. December contracts implied 3.49%, 85bps less than the current cash rate.

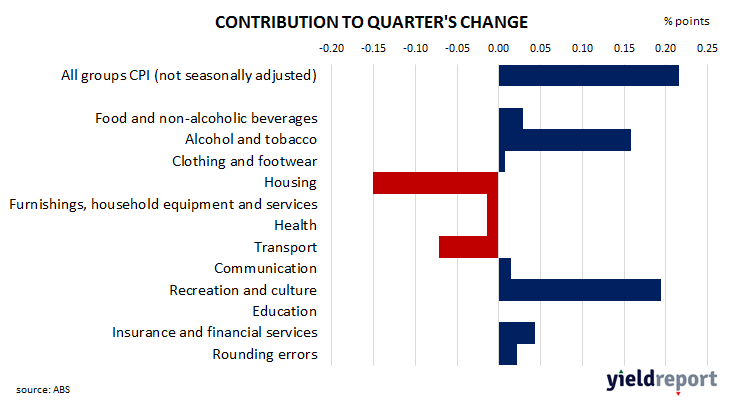

The largest single effect of the headline inflation figure in the quarter came from a 1.5% rise in “Recreation and culture” prices, contributing 0.19 percentage points to the total. A 2.4% increase in alcohol and tobacco prices and a 0.7% fall in housing costs also had significant effects on the outcome.

Here’s what a few economists said about the figures:

Luci Ellis, Westpac

Normally it should not come down to one number. This round, however, the CPI has been the deciding factor because the message from other available data has been so mixed. With trimmed mean inflation at 0.5% in the quarter, we have just enough evidence to conclude that disinflation has proceeded faster than the RBA expected, so the Board will have the required confidence to start the rate-cutting phase in February.

Catherine Birch, ANZ

There are positive signs that housing disinflation will continue into 2025, reflecting the softening market. In December, rent inflation slowed to 0.3% rather than maintaining the 0.6% trend. And new dwelling construction costs were largely steady, rather than rebounding from the 0.6% fall in November which reflected builder discounts. Given these two expenditure classes account for 14.4% of the CPI basket, this will help bring underlying inflation sustainably into the target band in 2025.

29 January 2025

Summary: Headline inflation up 0.2% in Sep quarter, less than expected; annual rate of RBA preferred measure slows from 3.6% to 3.2%; ACGB yields fall; rate-cut expectations firm; recreation/culture prices main driver of result.

In the early 1990s, high rates of inflation in Australia were reined in by the “recession we had to have” as it became known. Since then, underlying consumer price inflation has averaged around 2.5%, in line with the midpoint of the RBA’s target range. However, the various measures of consumer inflation trended lower during the decade after the GFC and hit a multi-decade low in 2020 before rising significantly in the quarters following September 2021.

Consumer price indices for the December quarter have now been released by the ABS and the “headline” inflation rate came in at 0.2% before seasonal adjustments. The result was less than 0.4% rise which had been generally expected but in line with the September quarter’s increase. On a 12-month basis, the inflation rate slowed from 2.8% to 2.4%.

The RBA’s preferred measure of underlying inflation, the “trimmed mean”, increased by 0.5% over the quarter, slightly less than the 0.6% increase which had been generally expected and down from the 0.8% in the September quarter. The 12-month inflation rate slowed from 3.6% after revisions to 3.2%.

Domestic Treasury bond yields fell moderately across a slightly flatter curve on the day, in contrast with the modest rises of US Treasury yields on Tuesday night. By the close of business, the 3-year ACGB yield had shed 6bps to 3.78%, the 10-year yield had lost 5bps to 4.40% while the 20-year yield finished 4bps lower at 4.83%.

Expectations regarding rate cuts in the next twelve months firmed, with a February 2025 rate cut viewed as highly likely. Cash futures contracts implied an average of 4.255% in February, 3.92% in May and 3.645% in August. December contracts implied 3.49%, 85bps less than the current cash rate.

The largest single effect of the headline inflation figure in the quarter came from a 1.5% rise in “Recreation and culture” prices, contributing 0.19 percentage points to the total. A 2.4% increase in alcohol and tobacco prices and a 0.7% fall in housing costs also had significant effects on the outcome.

Here’s what a few economists said about the figures:

Luci Ellis, Westpac

Normally it should not come down to one number. This round, however, the CPI has been the deciding factor because the message from other available data has been so mixed. With trimmed mean inflation at 0.5% in the quarter, we have just enough evidence to conclude that disinflation has proceeded faster than the RBA expected, so the Board will have the required confidence to start the rate-cutting phase in February.

Catherine Birch, ANZ

There are positive signs that housing disinflation will continue into 2025, reflecting the softening market. In December, rent inflation slowed to 0.3% rather than maintaining the 0.6% trend. And new dwelling construction costs were largely steady, rather than rebounding from the 0.6% fall in November which reflected builder discounts. Given these two expenditure classes account for 14.4% of the CPI basket, this will help bring underlying inflation sustainably into the target band in 2025.