Summary: Annual Inflation rate slows to 7.1% in March quarter, below expectations; RBA preferred measure falls from 6.9% to 6.6%; housing costs main drivers of result.

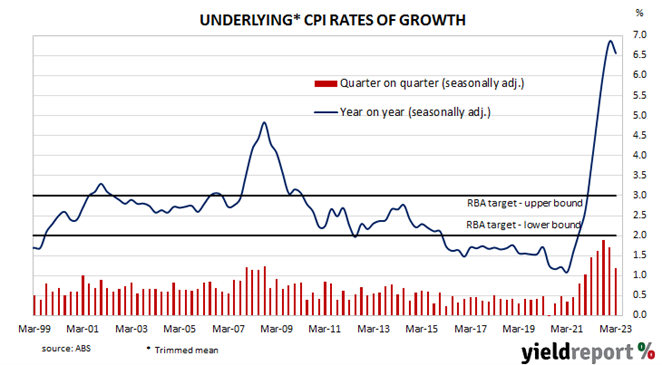

In the early 1990s, high rates of inflation in Australia were reined in by the “recession we had to have” as it became known. Since then, underlying consumer price inflation has averaged around 2.5%, in line with the midpoint of the RBA’s target range. However, the various measures of consumer inflation trended lower during the decade after the GFC and hit a multi-decade low in 2020 before rising significantly in the quarters following September 2021.

Consumer price indices for the March quarter have now been released by the ABS and the seasonally-adjusted inflation rate posted a 1.3% rise. The increase was below consensus expectations of a 1.4% rise and well down from the December quarter’s 1.9%. On a 12-month basis, the seasonally-adjusted rate slowed from 7.8% to 7.1%.

The RBA’s preferred measure of underlying inflation, the “trimmed mean”, increased by 1.2% over the quarter, less than the 1.4% increase which had been generally expected as well as the December quarter’s 1.7% rise. The 12-month inflation rate fell from 6.9% to 6.6%.

Domestic Treasury bond yields moved substantially lower on the day following large falls of US Treasury yields overnight. By the close of business, the 3-year ACGB yield had shed 17bps to 2.92%, the 10-year yield had lost 14bps to 3.31% while the 20-year yield finished 11bps lower at 3.76%.

In the cash futures market, expectations regarding another 25bps rate rise softened considerably. At the end of the day, contracts implied the cash rate would remain close to the current rate of 3.57% to average 3.585% in May and then creep up to an average of 3.635% in August. November contracts implied a 3.545% average cash rate while May 2024 contracts implied 3.31%, 26bps below the current cash rate.

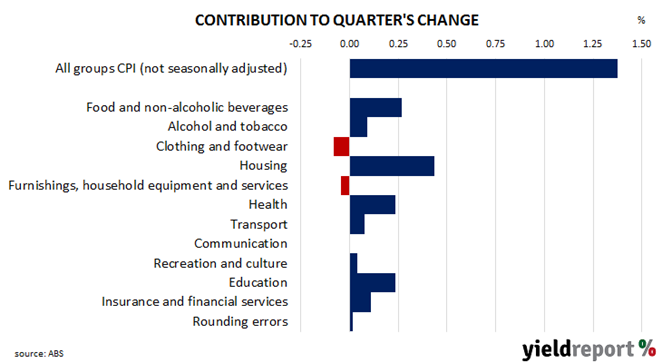

The main driver of the headline inflation figure in the quarter was a 1.9% rise in housing costs, contributing just under 0.45 percentage points of the 1.4% (unadjusted) increase. Food, health and education costs also had noticeable influences on the quarter’s reading, each contributing around 0.25% percentage points to the quarterly total.

Here’s what a few economists thought about the figures:

Chris Read, Morgan Stanley Australia

Q1 CPI was broadly in line and confirmed a peak in inflation. Goods inflation fell and services rose, a dynamic which could slow inflation declines later in the year. We expect this will see RBA eventually act on a tightening bias but the pause is likely to be extended at next week’s meeting.

Adelaide Timbrell, ANZ

Trimmed mean inflation and the monthly CPI indicator were both lower than expected, supporting our view that the RBA will keep the cash rate at 3.6% in May. Looking further ahead, though, persistently strong services inflation, reflecting excess demand in the economy, suggests that more RBA tightening will be needed in coming months

Justin Smirk, Westpac

The more modest rise in the Trimmed Mean is highlighting that the current disinflationary force, particularly for goods, appears to be greater than we thought. For while services inflation is holding up and is likely to prevent inflation falling back within the band in 2023…it is not enough to prevent goods disinflation taking the annual pace of inflation back to close to the band by the first half of 2024.

George Tharenou, UBS

Overall, Q1 headline CPI was ~0.2% points below the RBA’s implied forecast for a second quarter. But the Trimmed Mean was close to, or slightly higher, than the RBA’s profile. ‘Domestic’ inflation also remains relatively sticky. Hence, the RBA’s May SOMP will likely largely keep its hawkish inflation outlook intact, with headline ‘too high’ this year, and projected to stay above target in 2024.

Indeed, the RBA’s ‘reaction function’ to Q4 focussed on underlying and domestic inflation. Hence, we still expect the RBA will probably hike rates by another 25bps, to 3.85%, with the most likely timing at their next meeting in May. However, the slower Trimmed Mean [inflation] does ‘open the window’ for the RBA to extend its pause from April and makes May a closer call. Nonetheless, the RBA’s April meeting minutes were on the hawkish side, and clearly raised the risk of a ‘later hike’, after the minimum wage decision due by June.