By guest contributor Ken Atchison

In the latest Intergenerational Report, which has been prepared and released by the Federal Treasurer, Jim Chalmers, an outlook for the economy and the Australian Government’s finances over the next 40 years has been presented. It reflects the views of the Labor government, which was elected in 2022. While interest rate consequences are driven by shorter term influences, a perspective about future interest rates is provided from a review of the report.

It is highly likely that interest rates in Australia will continue the long term trend of being at a premium above interest rates prevailing in major trading partners.

In the report, forces which will shape the economy and fiscal position over the next 40 years are discussed. They are as follows:

Population ageing

Technological and digital transformation

Climate change and the net zero transformation

Rising demand for care and support services

Geopolitical risk and transformation

Changing industrial base

Each of these factors is material and all impact on the government sector. Consequences for the private sector were not addressed through any significant analysis or commentary. Australia is a country with 11.9 million persons, or 85% of the workforce, employed by the private sector. Observations about small business participation in Australia were absent.

Retirement income funding through superannuation will increase, thereby reducing the dependence on age pensions. No consideration of the unfunded liability for age pensions, which is significant, was addressed. The estimated unfunded liability at the Federal level is $5.5 trillion, or 2.2 times Australian GDP.

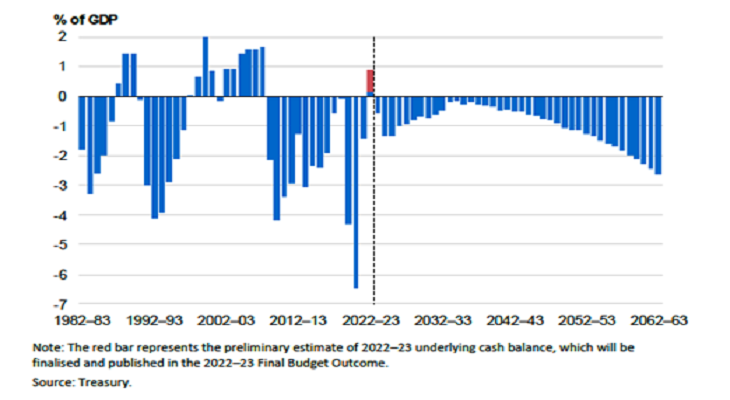

Continued fiscal deficits are projected. As shown in Chart 1 the fiscal deficit is measured by underlying cash balance, which was in surplus in 2022/23, will be in deficit thereafter through to 2063. Historically, surpluses have been achieved as the economic cycles move from growth to recessions and automatic stabilisers, such as unemployment benefits, have come into play. Any notion that fiscal policy should move with the strength and weakness in the economy is absent.

Chart 1 Underlying Cash Balance

Persistent fiscal deficits will shift the primary responsibility for economic policy onto monetary policy and the exchange rate.

Australia has been a net deficit country on balance of payments through much of its history and for considerable periods operated a federal government budget deficit. Persistent high levels of public sector activity implied in the report are a negative for enhanced productivity. A relatively loose economic policy has meant inflation has been higher than trading partners. As a result, interest rates have been at a premium to those of major trading partners.

Excessive increases in debt by the Australian states has not been considered in the report. Any policy requiring budget discipline by the states is not on any agenda; without some restraint, borrowings will add to upward pressure on interest rates

As the US dollar is the reserve currency globally, it is the global benchmark for interest rates. Persistent substantial US fiscal deficits will ensure US interest rates stay high. Emergence of a BRICS-based currency as an alternative to the US dollar has momentum. However, it will not replace the US dollar in the near future so US interest rates will remain the benchmark. (BRICS are Brazil, Russia, India, China and South Africa plus some other emerging market countries.)

There is no indication in the report that government policies might address the issue of continued interest- rate premium on borrowings. Australia, by following the narrative in the intergenerational report, will persist with an interest-rate premium to high US interest rates on a growing debt level.