By guest contributor Marc Hollenstein, analyst, Atchison Consultants

In the current low interest rate environment, investors continue to look for high dividend paying stocks and “cash-rich” companies that, having reduced debt, are being pressured by corporate activists to increase dividend payouts.

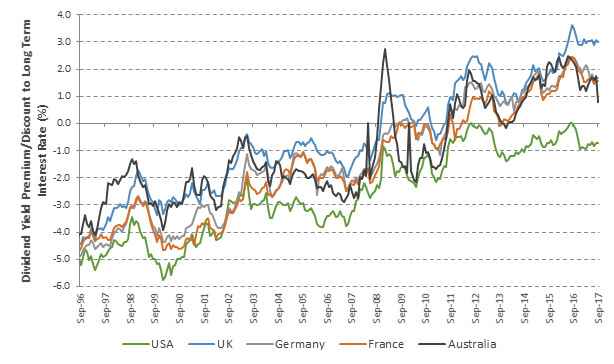

High dividend paying stocks continue to be bid up, particularly in Germany, France and Japan where long term interest rates remain near zero or marginally in positive territory (refer to Figure 1).

Source: MSCI, OECD

In Europe, this trend is expected to continue until December 2017 as the ECB continues with its asset purchase programme of a total of €60 billion. The U.S, however, may see some reversal on the back of the Federal Reserve’s announcement to reduce its balance sheet – initially by USD$10 billion commencing in October and gradually increasing it to USD$50 billion a month.

In absolute terms, historical dividend yields (refer to Table 1) for international shares are generally lower than dividend payouts from Australian listed entities. In particular, listed companies on mainland Europe and in the U.S.A have historically not rewarded investors with significant income streams. The substantial difference to Australia is partially due to the benefits of Australia’s imputation system which prevents double taxation of profits at a company and investor level. Consequently, domestic companies are more inclined (and pressured by investors) to issue higher dividends. The ratio of profits paid out as dividends by Australian listed entities is at around 73% while the average listed-company around the world currently only returns 44% of profits to shareholders.

Table 1: Dividend Yields to 30 September 2017