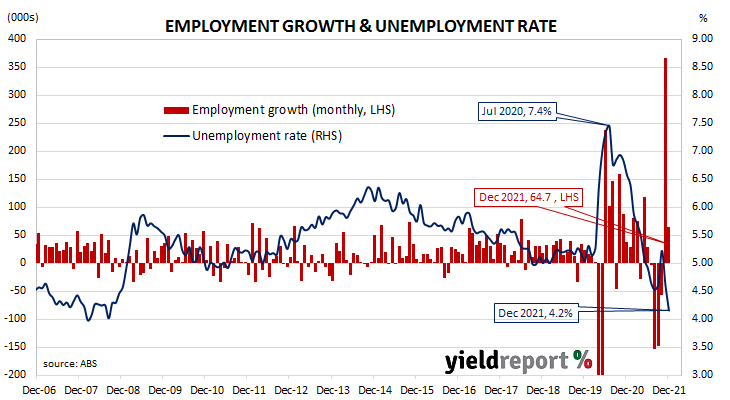

Summary: Total employment up 64,700 in December; rise in line with expected figure; figures “little affected by Omicron”, reference period pre-surge; shows the momentum amid post Delta re-opening “extremely strong”; participation rate steady at 66.1%; fewer jobseekers, slightly larger workforce sends jobless rate to 4.2%; more part-time, full-time jobs; aggregate work hours up 1.0%; underemployment rate down from 7.5% to 6.6%.

Australia’s period of falling unemployment came to an end in early 2019 when the jobless rate hit a low of 4.9%. It then averaged around 5.2% through to March 2020, bouncing around in a range from 5.1% to 5.3%. Leading indicators such as ANZ’s Job Ads survey and NAB’s capacity utilisation estimate suggested the unemployment rate would rise in the June 2020 quarter and it did so, sharply. The jobless rate peaked in July 2020 but fell below 7% a month later. It then trended lower through the remainder of 2020 and into 2021.

The latest Labour force figures have now been released and they indicate the number of people employed in Australia according to ABS definitions increased by 64,700 in December. The rise was essentially in line with the expected 60,000 increase but considerably less than November’s 366,200 jump.

“Today’s labour market data were little affected by Omicron, as the reference period ended before cases surged. Omicron will have an effect on the labour market over coming months but we think any downside will be small and short-lived,” said ANZ senior economist Catherine Birch.

Short-term domestic Treasury bond yields increased on the day while longer-term yields hardly reacted. By the close of business, the 3-year ACGB yield had gained 4bps to 1.46%, the 10-year yield had slipped 1bp to 2.02% while the 20-year yield finished unchanged at 2.52%.

In the cash futures market, expectations of any material change in the actual cash rate, currently at 0.05%, remained fairly soft until May. At the end of the day, contract prices implied the cash rate would not exceed the RBA’s 0.10% target rate until April 2022 and then rise to 0.31% by June. February 2023 contracts implied a cash rate of 1.19%.

“Overall, the labour market shows the momentum amid the re-opening of the economy post Delta was extremely strong. For now, the impact of Omicron is clearly a material negative for activity and adds significant uncertainty to the outlook. However, consumer sentiment remains resilient so far,” said UBS economist George Tharenou.

The participation rate remained unchanged from November’s 66.1%, as the total available workforce increased by just 2,500 to 13.816 million. The number of unemployed persons fell by 62,200 to 574,400; the lower jobless number in conjunction with the slightly larger number of people in the workforce led to a fall in the unemployment rate from 4.6% to 4.2%.

The aggregate number of work hours across the whole Australian economy rose as 23,300 residents gained part-time positions and 41,500 residents gained full-time positions. In percentage terms, the total number of work hours increased by 1.0% after rising by 4.5% in November. On a 12-month basis and after revisions, aggregate hours worked rose by 3.7% as 19,400 more people held part-time positions and 356,600 more people held full-time positions than in December 2020.

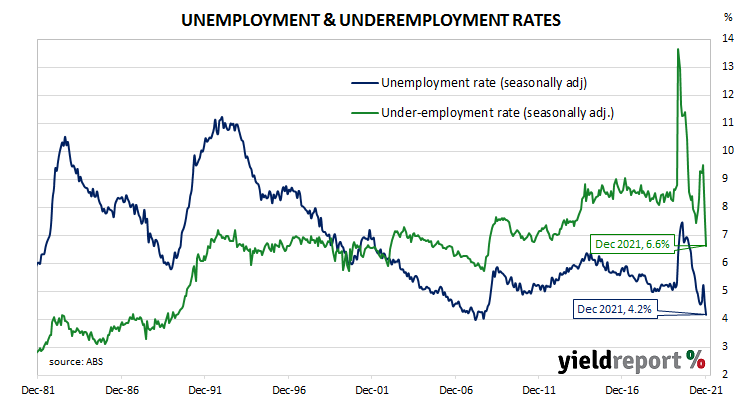

In recent years, more attention has been paid to the underemployment rate, which is the number of people in work but who wish to work more hours than they do currently. December’s underemployment rate fell from 7.5% to 6.6%, making it the lowest reading since November 2008.

The underutilisation rate, that is the sum of the underemployment rate and the unemployment rate, has a strong correlation with the annual growth rate of the ABS private sector wage index when advanced by one quarter. December’s underutilisation rate of 10.8% corresponds with an annual growth rate of about 4.1%.