Summary: Unemployment rate continues rise; May job losses revised up; employment number rises more than expected; participation rate rebounds as former workers begin search; work hours rise more than employment over month; underemployment rate eases for second consecutive month; unemployment expected to rise even without re-introduction of Melbourne restrictions.

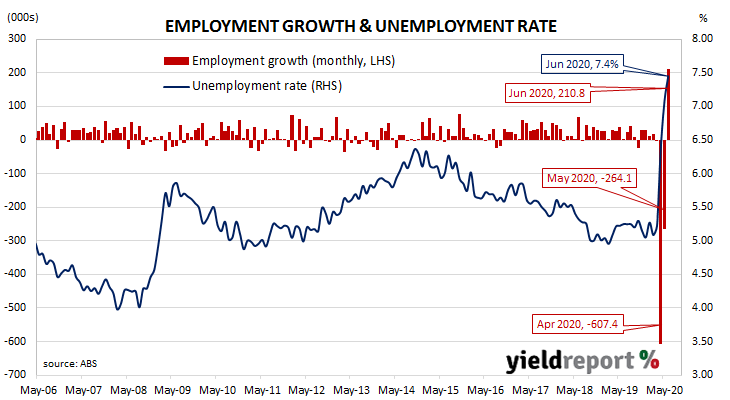

Australia’s period of falling unemployment came to an end in early 2019 when the jobless rate hit a low of 4.9%. It then averaged around 5.2% through to March 2020, bouncing around in a range from 5.1% to 5.3%. Readings of leading indicators such as ANZ’s Job Ads survey and NAB’s capacity utilisation estimate suggested the unemployment rate would rise and it did. Despite recent improvements, they still leave some room for further rises towards Treasury’s forecast of an 8% unemployment rate, although not by the end of June.

The latest Labour force figures have now been released and they indicate the number of people employed in Australia increased by considerably more than economists had expected. The report showed the total number of people who held a job according to ABS definitions rose by 210,800 in June, in contrast to May when 264,100 people lost their jobs after it was revised up from 227,700. However, the unemployment rate rose from May’s 7.1% to 7.4%.

ANZ senior economist Catherine Birch put the increase down to “Australia’s effective management of the first wave of COVID-19 cases and the earlier-than-expected rollback of restrictions…”

Market expectations prior to the report’s release were for about 104,000 positions to be added and for the unemployment rate to remain at 7.1%. Domestic Treasury bond yields rose a touch at the long end of the curve, in line with movements of their US counterparts in overnight trading. By the end of the day, the 90-day bank bill rate and the 3-year ACGB yield both remained unchanged at 0.10% and 0.31% respectively while 10-year and 20-year yields had each crept up 1bp to 0.90% and 1.54% respectively.

In the cash futures market, expectations of a change in the actual cash rate remained fairly stable. By the end of the day, contracts implied the cash rate would remain in a range of 0.13% to 0.14% through to the latter part of 2021.