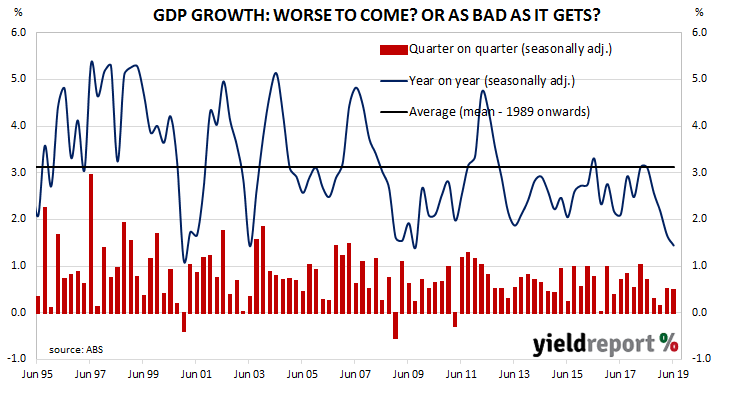

Since the “recession we had to have” as the recession of 1990/91 became known, Australia’s GDP growth has been consistently positive, with only the odd negative quarter here and there. Even during, and immediately after, the GFC, Australia managed to avoid two consecutive quarters of negative growth. However, the annual rate of growth fell below 2% in the March quarter and forward-looking indicators have been weakening, so much so the RBA felt the need to cut the official rate in June and again in July.

The latest figures released by the ABS indicate June quarter GDP grew by 0.5%, in line with the market consensus figure and the same rate as in the March quarter. On an annual basis, GDP increased by 1.4%, down from the March quarter’s comparable figure of 1.7% after revisions.

Westpac senior economist Andrew Hanlan said, “The economy lost considerable momentum from mid-2018, led by the turning down of the housing sector…and by the consumer.” Westpac’s chief economist, Bill Evans, said the figures “further strengthen the case for a rate cut in the very near-term.”

The local bond market ignored falls in US Treasury yields and sent yields at the front of the curve a little higher. By the end of the day, 3-year Treasury bond yields had increased by 2bps to 0.72% while 10-year and 20-year yields each remained unchanged at 0.94% and 1.35% respectively.