Summary: Headline Inflation rate increases to 3.8% in June quarter, as expected; RBA preferred measure slows from 4.0% to 3.9%; ACGB yields plunge; rate-cut expectations harden; housing, food & beverages, main drivers of result.

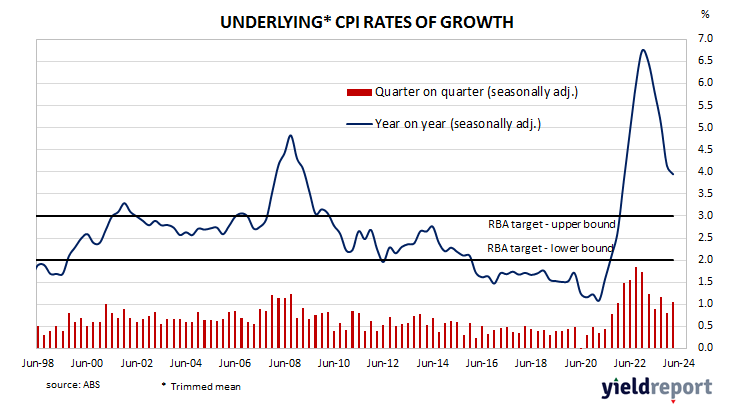

In the early 1990s, high rates of inflation in Australia were reined in by the “recession we had to have” as it became known. Since then, underlying consumer price inflation has averaged around 2.5%, in line with the midpoint of the RBA’s target range. However, the various measures of consumer inflation trended lower during the decade after the GFC and hit a multi-decade low in 2020 before rising significantly in the quarters following September 2021.

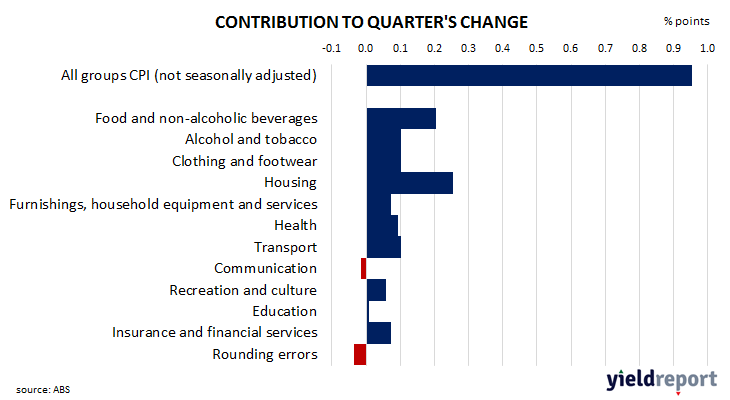

Consumer price indices for the June quarter have now been released by the ABS and the inflation rate came in at 1.0% before seasonal adjustments. The result was in line with consensus expectations ae well as the March quarter’s increase. On a 12-month basis, the inflation rate accelerated from 3.6% to 3.8%.

The RBA’s preferred measure of underlying inflation, the “trimmed mean”, increased by 0.8% over the quarter, less than the 1.0% increase which had been generally expected and the March quarter’s 1.1% rise. The 12-month inflation rate slowed from 4.0% to 3.9%.

Domestic Treasury bond yields plunged on the day, with falls at the short end outpacing movements of longer-term yields. By the close of business, the 3-year ACGB yield had shed 23bps to 3.72%, the 10-year yield had lost 17bps to 4.12% while the 20-year yield finished 12bps lower at 4.51%.

Expectations regarding rate cuts in the next twelve months hardened considerably. Cash futures prices at the end of the day implied the cash rate now has some chance of falling below the current rate of 4.34% in the short-term, with an average of 4.33% in August and 4.255% in November. February 2025 contracts implied 4.145% while May 2025 contracts implied 3.93%, 41bps less than the current cash rate.

The main driver of the headline inflation figure in the quarter were a 1.1% rise in housing costs, while food and beverage prices also made a significant contribution.

Here’s what a few economists said about the figures:

Catherine Birch, ANZ

Annual headline inflation rose 0.2 percentage points and trimmed mean disinflation has slowed. But this won’t be enough to convince the RBA that it cannot return inflation to target by 2026 under current policy settings, particularly given the ongoing slowdown in the broader economy and labour market. While price pressures have picked up a little this year, the underlying trend points to lower inflation. The six-month annualised inflation rates for tradables, non-tradables, goods and services were all lower in Q2 2024 than in Q2 2023.

Justin Smirk, Westpac

The RBA was forecasting CPI inflation to reach 3.8% in the June quarter, in line with today’s result. However for core inflation, the RBA was also forecasting 3.8% for June, so the 3.9% pace was a touch stronger than they were expecting. But with a six-month annualised pace of 3.8%, core inflation is heading in the right direction.

Chris Read, Morgan Stanley Australia

Trimmed mean CPI was the focus going into the Q2 print and it missed expectations. While still stronger than RBA forecasts and showing minimal disinflation this year, it reduces the pressure from the data and so we no longer expect an August hike.

Faraz Syed, Citigroup

Following the Q2 downside CPI surprise earlier, we jettisoned our view of a rate hike next week. Instead we now expect the RBA to leave rates unchanged in 2024 at 4.35%. That said, the fundamentals haven’t changed; inflation remains persistent in some categories, labour market remains tight and there is ongoing fiscal stimulus in H2. Therefore, we expect the RBA to maintain its hawkish bias next week and continue to suggest that it remains vigilant to upside inflation risks.