As the first call date of any hybrid listed on the ASX approaches, speculation typically turns to the likelihood of some sort of replacement security. Experience over the years suggests hybrids are usually redeemed or “resold” and not converted into ordinary equity. In order to maintain balance sheet ratios, additional equity capital must be raised. In recent years, most companies in this situation have chosen to issue another hybrid. Commonwealth Bank (CBA) has several hybrid securities currently listed on the ASX and one of them, CBA PERLS 6 (ASX code: CBAPC) is fast approaching its first call date in mid-December.

CBA has just announced it will issue another hybrid security. It plans to raise $750 million worth of PERLS 11 Capital Notes (ASX code: CBAPH), with the ability to raise more or less than this amount. The new securities will be perpetual, convertible, subordinated, unsecured notes and the proceeds will be used to “fund CBA’s business”. CBA intends to redeem its PERLS 6 notes and, given there are $2 billion PERLS 6 outstanding, one could say the new issue really is only to fund their redemption.

The new notes have some features in common with equities and some features in common with debt securities. Distributions are at the discretion of directors but they are calculated according to a set formula with reference to the $100 face value of the securities. The notes will qualify as Additional Tier 1 (AT1) capital under the Basel III bank regulatory framework, which means they have the now-standard “trigger event” clauses which may lead to early conversion into ordinary shares or a write-off of the capital notes should APRA require it. In the event CBA were wound up (and APRA had not already forced a write-off), its hybrids would rank above ordinary shares but below ordinary debt securities and other liabilities.

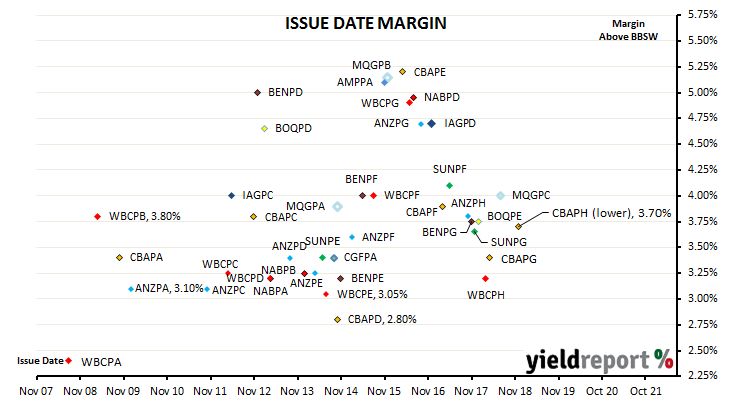

The new PERLS have an indicative distribution rate equivalent to 3 month BBSW plus a margin of 370bps to 390bps. The final margin will be determined by a “book build” on 8 November 2018. A book build is a tender process managed by investment banks on behalf of the issuer in which investment institutions each place bids for a set volume at a price/yield. (This is the same way as the AOFM holds tenders to sell government bonds each week). If recent history is any guide, then the margin is likely to be set at the lower end. Distributions will be non-cumulative, at the discretion of CBA directors and paid quarterly in arrears. At the prevailing level of interest rates and if the margin is at the lower end of the range, the new notes will initially pay a little under around 6.00% (annualised) inclusive of franking credits. *As interest rates change, specifically the bank bill swap rate, quarterly payments will also change.

The new PERLS have an indicative distribution rate equivalent to 3 month BBSW plus a margin of 370bps to 390bps. The final margin will be determined by a “book build” on 8 November 2018. A book build is a tender process managed by investment banks on behalf of the issuer in which investment institutions each place bids for a set volume at a price/yield. (This is the same way as the AOFM holds tenders to sell government bonds each week). If recent history is any guide, then the margin is likely to be set at the lower end. Distributions will be non-cumulative, at the discretion of CBA directors and paid quarterly in arrears. At the prevailing level of interest rates and if the margin is at the lower end of the range, the new notes will initially pay a little under around 6.00% (annualised) inclusive of franking credits. *As interest rates change, specifically the bank bill swap rate, quarterly payments will also change.