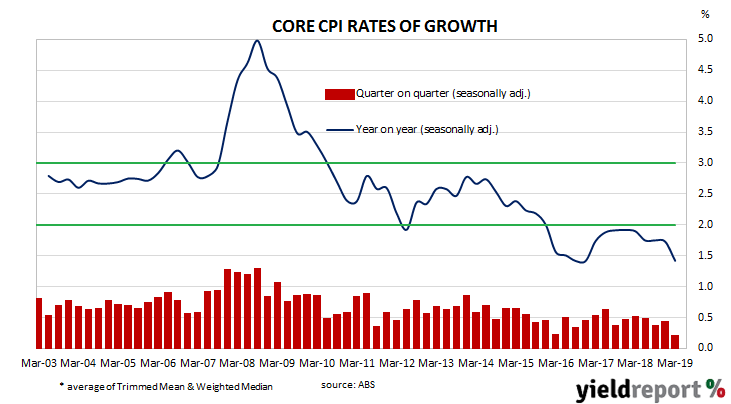

In the early 1990s, entrenched inflation was broken by the “recession we had to have”, as it became known. Since then, “core” consumer price inflation has averaged around 2.6% which, coincidentally, is almost the midpoint of the RBA’s target range of 2%-3%. However, it has trended lower and lower since 2009 and it has not been above 2.0% since late 2015, leading some economists to forecast further official rate cuts.

Figures for the March quarter have now been released by the ABS and both the headline and seasonally-adjusted figures were less than their expected 0.2% increases. The headline inflation rate was 0.0% for the quarter while seasonally-adjusted inflation came in at just 0.1%. On a 12-month basis, both headline and seasonally-adjusted inflation registered 1.3%, both having recorded 1.8% in the December quarter.

Core inflation measures favoured by the RBA, such as the average of the “trimmed mean” and the “weighted median”, both fell on a quarterly and annual basis. The average of the two measures, 0.2%, was less than the market’s expected figures of 0.4% for the quarter. As a result, the 12-month figure of 1.4% was also lower than the expected 1.8% increase.

ANZ economist Hayden Dimes said, “The downward surprise to core inflation in Q1 leaves the RBA will little choice but to cut the cash rate by 25bps at its May meeting, with another 25bps likely to follow in August.”

ANZ economist Hayden Dimes said, “The downward surprise to core inflation in Q1 leaves the RBA will little choice but to cut the cash rate by 25bps at its May meeting, with another 25bps likely to follow in August.”

Financial markets reacted by sending local bond yields significantly lower while the Aussie dollar fell close to 70 US cents. By the end of the day, 3-year ACGB yields had plunged 15bps lower to 1.25%, 10-year yields had shed 11bps to 1.80% and the yield on 20-year ACGBs had lost 8bps to 2.25%. The local currency dropped from 70.90 US cents to 70.40 US cents and then finished the afternoon session at around 70.35 US cents.