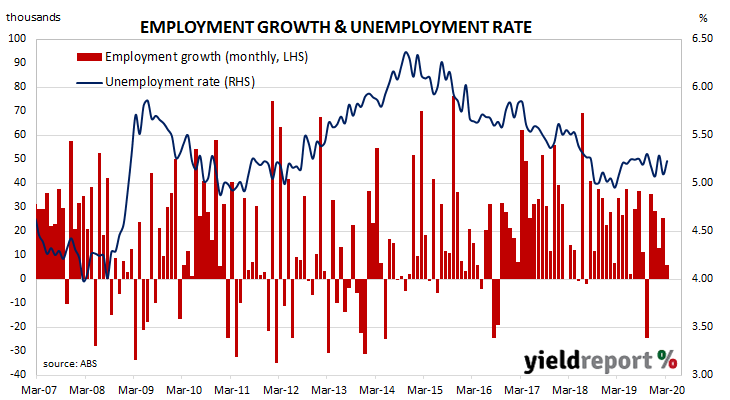

Australia’s period of falling unemployment came to an end in early 2019 when the jobless rate hit a low of 4.9%. Since then, it has averaged around 5.2%, bouncing around in a range which extends from 5.1% to 5.3%. However, recent leading indicators such as ANZ’s March Job Ads survey and NAB’s March capacity utilisation estimate have suggested the unemployment rate will rise substantially soon.

The latest Labour force figures have now been released and they indicate the number of people employed in Australia increased by more than economists had expected. The report showed the total number of people who held a job increased by 5,900 in March, while the unemployment rate ticked up to 5.2% from 5.1%.

ANZ senior economist Catherine Birch said, “We did not expect to see large-scale job losses yet given the timing of the survey, which covered the first two weeks of March, before the shutdown of non-essential services on 23 March.” Market expectations prior to the report’s release were for 30,000 positions to be lost and for the unemployment rate to rise to 5.4%. Domestic Treasury bond yields fell across the curve, although part of the local response was in reaction to lower US treasury yields in overnight trading. By the end of the day, the 90-day bank bill rate had declined by 2bps to 0.12%, the 3-year ACGB yield had shed 3bps to 0.25% while 10-year and 20-year yields each finished 7bps lower at 0.84% and 1.56% respectively.

Market expectations prior to the report’s release were for 30,000 positions to be lost and for the unemployment rate to rise to 5.4%. Domestic Treasury bond yields fell across the curve, although part of the local response was in reaction to lower US treasury yields in overnight trading. By the end of the day, the 90-day bank bill rate had declined by 2bps to 0.12%, the 3-year ACGB yield had shed 3bps to 0.25% while 10-year and 20-year yields each finished 7bps lower at 0.84% and 1.56% respectively.

Prices of cash futures contracts moved to reflect a slight hardening of rate-cut expectations in spite of the commonly-held view the cash rate is already at the “effective lower bound”. By the end of the day, May contracts implied a rate cut down to zero as a 52% chance, up from the previous day’s 50%. June contracts implied a 47% chance of such a move, up from 45%. Contract prices of months later in 2020 and early 2021 implied similar probabilities.