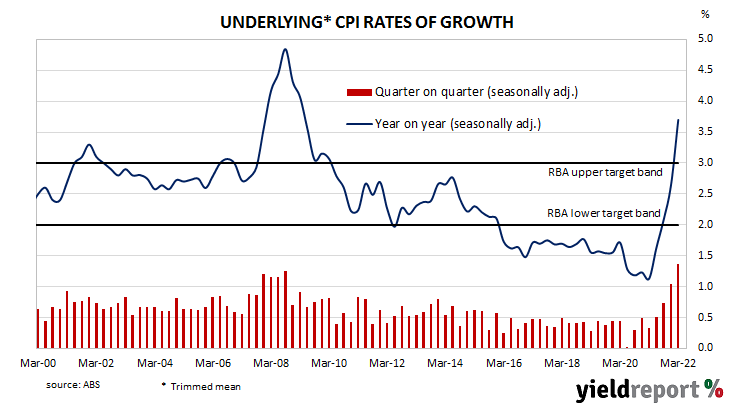

Summary: Annual Inflation rate accelerates to 5.2% in March quarter, above market expectations; RBA preferred measure rises from 2.6% to 3.7%, above expected; housing, food, transport costs main drivers of result.

In the early 1990s, high rates of inflation in Australia were reined in by the “recession we had to have” as it became known. Since then, underlying consumer price inflation has averaged around 2.5%, in line with the midpoint of the RBA’s target range. However, the various measures of consumer inflation trended lower during the decade after the GFC and hit a multi-decade low in 2020, despite the efforts of the RBA to increase them through historically low cash rates.

Consumer price indices for the March quarter have now been released by the ABS and the seasonally-adjusted inflation rate posted a 2.0% rise. The increase was higher than the generally expected figure of 1.7% and the December quarter’s 1.3%. On a 12-month basis, the seasonally-adjusted rate accelerated from 3.6% after revisions to 5.2%.

The RBA’s preferred measure of underlying inflation, the “trimmed mean”, increased by 1.4% over the quarter, above market expectations of a 1.2% increase as well as the December quarter’s 1.0% rise. The 12-month inflation rate rose from 2.6% to 3.7%.

Commonwealth Government bond yields increased at the short end on the day but fell further out along the yield curve. By the close of business, the 3-year ACGB yield had added 2bps to 2.83% while 10-year and 20-year yields both finished 5bps lower at 3.10% and 3.43% respectively.

In the cash futures market, expectations of any material change in the actual cash rate, currently at 0.06%, hardened in favour of rate rises over the next twelve months. At the end of the day, contract prices implied the cash rate would rise next month to 0.25% and then increase to 1.33% by August. February 2023 contracts implied a cash rate of 2.68%.

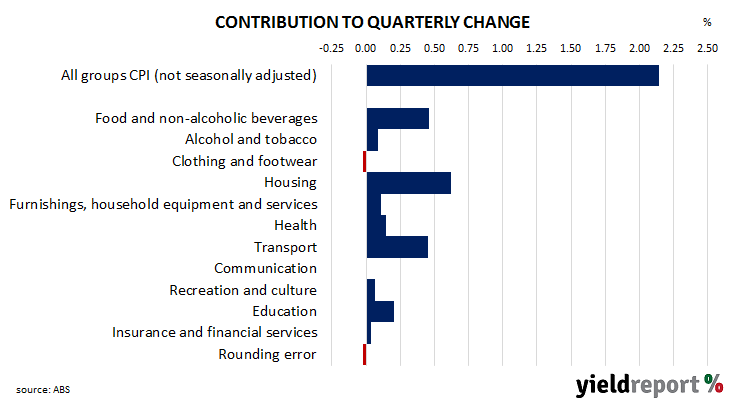

The main driver of the headline inflation figure in the quarter again was a 2.7% rise in housing costs, contributing 0.62 percentage points of the 2.14% (unadjusted) increase over the quarter. Food and beverage prices also had a significant influence on the quarter, rising by 2.8% and contributing 0.48% percentage points to the quarterly total. Transport prices rose by 4.2% and contributed 0.45 percentage points.

Here’s what a few economists thought about the figures:

David Plank, ANZ

The increase in non-tradables inflation signals that this is partly due to the momentum on wages and not just disruptions in the global economy.

We now expect the RBA to hike by 15bps next week. Inflation pressures have momentum and have broadened. A cash rate target of 0.10% is inappropriate against this backdrop. We don’t think the RBA needs to wait for more data on wages, given that its own liaison program indicates that “wages growth had continued to pick up in the March quarter.” The move in May will likely be followed by an increase of 0.25% in June, taking the cash rate to 0.50%.

We are conscious the RBA’s April meeting minutes highlighted the desire to be “consistent with its announced framework” and wait for data on “the evolution of labour costs” before it moves. So the RBA could still hold out for the labour market data and makes its first move in June. In which case we think the first move will be 40bps. Regardless of whether the RBA’s first move is in May or June, we expect the cash rate target to be at 0.50% by the early June. The CPI data so likely brings forward the time the cash rate target reaches 2%, possible to the first half of 2023. We still look for an eventual move into the 3’s.

NAB, Ivan Colhoun

NAB’s view is that the scale of the misses in today’s CPI relative to RBA forecasts as recently as February, together with indications of ongoing input and retail price pressures, will make it too difficult for the RBA to follow its April plan to wait to see the wages print in May before hiking rates in June. We now expect the first interest rate increase to be announced next week. Previously, we had the first rise at the June Board meeting.

The RBA will need to revise up their inflation track substantially, with the important trimmed-mean forecast scenarios beginning from an uncomfortably high 3.7% starting point. Key will be the Bank’s assessment of when and how much inflation will slow, given many likely non-persistent factors are driving much of the elevated prints even as the detail shows a lift in broader inflationary pressure. The trimmed mean measure has been skewed higher than the weighted median measure due to outsized price increases in goods and homebuilding which are unlikely to be a source of ‘sustainably higher’ inflation. Inflation pressures though of clearly broadened with 65% of the basket is now running above the mid-point of the RBA’s band. When viewed in the context of the strong labour market, it is an inflationary environment that is at odds with a policy to continue to keep the Central Bank’s foot firmly on the accelerator while it waits for lagging the labour cost story to fall into place.

Justin Smirk, Westpac

While the unwinding of the HomeBuilder grants continues to be part of the story behind the boost in inflation it is the shortages of building supplies and labour, heightened freight costs and ongoing strong demand [which] also contributed to price rises for newly built dwellings, as well as a broader inflationary pulse.

This broad spread inflationary pulse was captured by 1.4% gain in the trimmed mean, both the market and Westpac were expecting 1.2%, which the ABS reports as the largest quarterly rise since the beginning of the series in 2002. The ABS reports the lift in core inflation “reflected the broad-based nature of price rises, as the impacts of supply disruptions, rising shipping costs and other global and domestic inflationary factors flowed through the economy.”

This widespread nature of this inflationary pulse was further emphasised by the rise in the share of components of the CPI running faster than a 2.5%yr pace. The share lifted to 66% from 32% in March, the largest share of the CPI components running faster than 2.5%yr since December 2001 (post the introduction of GST).

Gareth Aird, Commonwealth Bank

Today’s data marks the first time that the trimmed mean CPI has printed above the RBA’s 2-3% target band since Q1 2010. Australia had several years where core inflation was below the RBA’s target band, notably 2016 to mid-2021. But it has been more than a decade since underlying inflation has been above the RBA’s target range. In that context it is not surprising that the RBA has been ‘patient’ to commence a tightening cycle.

Here we remind readers of what RBA Governor Lowe said in February 2022, “The approach that we are running at the moment, waiting for the evidence, does run the risk that inflation will be above 3% for a period of time and that risk is acceptable-we think running that risk is an appropriate thing to do.” The data today coupled with our expectation for underlying inflation to sit above the target range over the rest of 2022 means that risk has been realised.

There was evidence of broad-based inflation in today’s data, as we had anticipated. And the overall message is not positive for households because inflation is running well ahead of wages growth. Indeed, non-discretionary annual inflation was higher than the CPI and more than twice the rate of discretionary inflation. Put another way, the prices of goods and services that households need to purchase are running well ahead of price increases for non-essential goods and services.