Summary: Australia’s GDP up 0.1% in March quarter, slightly below expectations; up 1.1% over year; Westpac: total spending on domestic production flat except for statistical discrepancy; ACGB yields fall moderately; rate-cut expectations firm; ANZ: sees little which would change view on RBA, general outlook; imports, inventories again major influences in quarter.

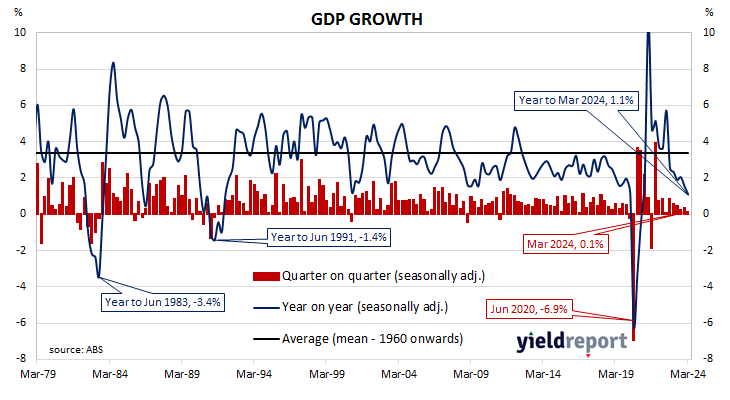

Since the “recession we had to have” as the recession of 1990/91 became known, Australia’s GDP growth has been consistently positive, with only the odd negative quarter here and there. However, Australia’s first recession in nearly thirty years was inevitable in 2020 once governments introduced restrictions which shut businesses and limited people’s movements for an extended period of time. Growth rates have been positive since then, although the September 2021 quarter proved to be the exception after restrictions were reintroduced in eastern states.

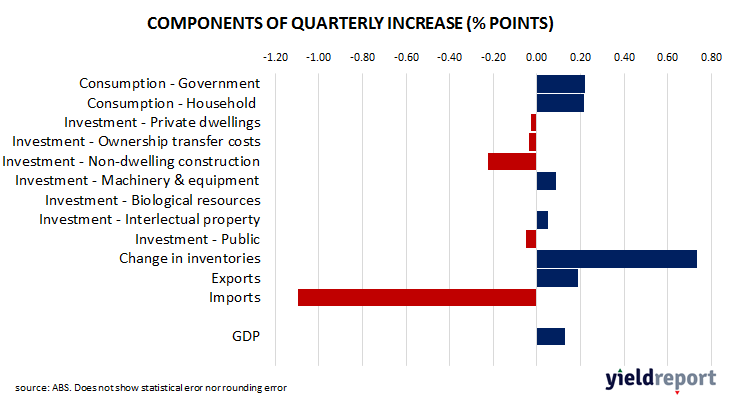

The latest GDP figures have now been released by the ABS and they indicate GDP rose by just 0.1% in the March quarter. The result was slightly below the 0.2% rise which had been generally expected and down from the December quarter’s 0.3% after it was revised up from 0.2%. On an annual basis, GDP expanded by 1.1%, down from 1.6% in the previous quarter.

“The Australian economy continued to limp along in the March quarter, edging just 0.1% higher,” said Westpac senior economist Matthew Hassan. “In fact, total spending on domestic production…was flat over the quarter, the small gain of 0.1% was driven by a positive statistical discrepancy.”

Commonwealth Government bond yields fell moderately on the day, in line with falls of US Treasury yields overnight. By the close of business, the 3-year ACGB yield had lost 4bps to 3.93% while 10-year and 20-year yields both finished 6bps lower at 4.26% and 4.56% respectively.

Expectations regarding rate cuts in the next twelve months firmed by the end of the day. In the cash futures market, contracts implied the cash rate would remain close to the current rate for the next few months and average 4.315% through June, 4.31% in July and 4.325% in August. November contracts implied 4.295%, February 2025 contracts implied 4.225% while May 2025 contracts implied 4.115%, 21bps less than the current cash rate.

“Overall, we see little in this release that would change our view on the RBA or the general outlook for the economy,” said ANZ senior economist Blair Chapman. “The pace of GDP growth over the past six months is a little weaker than we anticipated but labour market conditions have only eased slowly over the same period while recent inflation data have shown some stickiness.”

Imports increased by $6.7 billion, subtracting 1.10 percentage points from the quarter’s result, while a $4.5 billion inventory expansion contributed 0.73 percentage points. Households consumption contributed 0.22 percentage points.