The Statement on Monetary Policy (SoMP) is released each quarter and it is closely watched for updates to the RBA’s own forecasts.

In February’s SoMP, the opening statement of the “Outlook” section stated, “The outlook for the Australian economy is for growth to pick up over the next two years, supported by accommodative monetary policy, a pick-up in mining investment and a turnaround in dwelling investment.”

May’s Outlook is vastly different. “The outlook for the Australian and global economies is being driven by the COVID-19 pandemic. The necessary social distancing restrictions and other containment measures that have been in place to control the virus have resulted in a significant contraction in economic activity…”

The RBA’s forecasts are dependent “on how long social distancing remains in place and its effects on economic activity.” It is also mindful of the period of time in which “uncertainty and diminished confidence weigh on households’ and businesses’ spending, hiring and investment plans.”

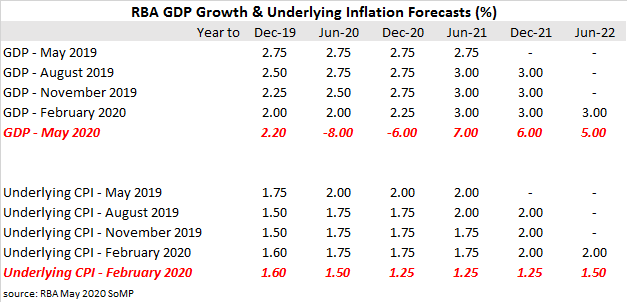

GDP growth rates in the early periods of the forecasts have been slashed. The RBA’s forecast GDP growth rate for the year to June 2020 (see table) has been cut by 10% and the calendar year to December 2020 has been cut by 8.25%. Forecasts of later periods have been increased significantly, with an expectation various sectors “gradually recover” under the RBA baseline scenario. These forecasts were flagged in the statement accompanying the RBA Board’s policy decision on Tuesday.

The RBA’s underlying inflation forecasts were reduced in all forecast periods but not by great amounts. The RBA’s favoured measure of underlying inflation, the “trimmed mean”, had been expected to rise in 2021 but now no rise is expected until 2022. In the RBA’s baseline scenario, “inflation expectations remain anchored to pre-existing levels.” However, the RBA notes a dependency on responses by the business and household sectors “to the large relative price adjustments over the period ahead.” Consumer sensitivity to higher import prices from an expected exchange-rate depreciation are also considered a factor.