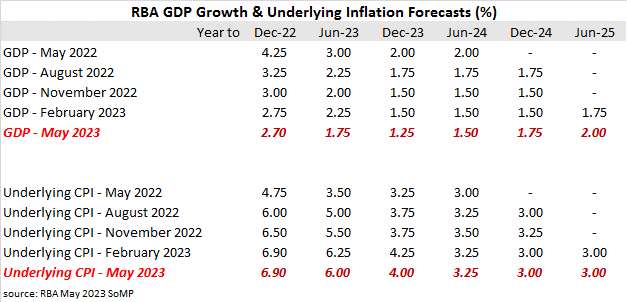

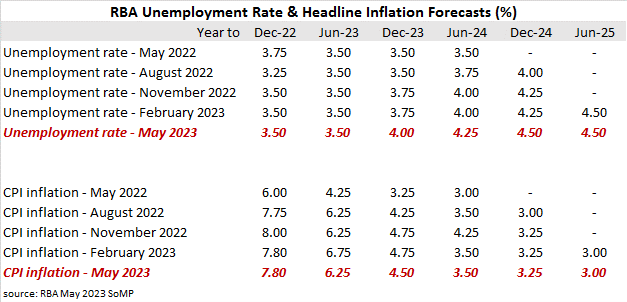

Summary: RBA trims 2023 GDP forecasts, raises forecasts for later periods; underlying inflation forecasts lowered; jobless rate expected to rise this year; some headline inflation forecasts reduced; Westpac: key theme of this SOMP is inflation outlook risk.

The Statement on Monetary Policy (SoMP) is released each quarter and it is closely watched for updates to the RBA’s own forecasts.

In February’s SoMP, the opening sentence of the “Outlook” section stated, “Global growth is forecast to remain well below its historical average over the next two years.”

As far as Australia was concerned, “The outlook for GDP growth is little changed from three months ago.”

May’s Outlook opened with a statement which is pretty much a repeat of February’s opening sentence. “Global growth is forecast to remain well below its historical average over the next two years, as high inflation and tighter monetary policy settings are expected to continue to weigh on demand.”

On domestic matters, it stated, “Growth in Australian economic activity is expected to have slowed in the March quarter and is forecast to remain subdued through this year as higher interest rates, the higher cost of living and earlier declines in household wealth continue to weigh on growth.” However, it then went on to say, ”The pace of growth is expected to increase gradually over the remainder of the forecast period as these headwinds fade.”

Accordingly, the RBA’s GDP growth forecasts have been trimmed for the periods out to December 2023 while the years to December 2024 and June 2025 have each been raised by 0.25 percentage points (see table below). Sub- trend GDP growth is expected to continue in the periods out to June 2025.

“Household consumption growth is expected to remain sluggish through this year as inflation and higher interest rates weigh on real disposable income. Consumption growth is expected to increase to around its pre-pandemic trend over 2024 as the effect of the earlier monetary policy tightening wanes and the cash rate decreases, inflation moderates, household wealth recovers and tax cuts support disposable income.”

The RBA’s underlying inflation forecasts have been lowered in the years to June 2023 and December 2023, each by 0.25% percentage points. Other periods’ forecasts remain unchanged. The RBA’s target band for underlying inflation is 2%-3%, so underlying inflation is expected by the RBA to be back to the top of this target range in the second half of next year.

“Underlying inflation is expected to decline over coming years to be around the top of the inflation target range by mid-2025…On the one hand, lower goods prices from the resolution of supply chain issues could come through sooner and swifter than anticipated. On the other hand, domestic price pressures may be stronger and more persistent than expected.”

The RBA’s view of the unemployment rate typically follows from its forecasts of GDP growth. The unemployment rate had fallen to 3.50% at the end of December 2022 and the RBA still expects it to remain steady until the second half of 2023 when it is forecast to rise to 4.00%, six months earlier than previously expected. Further increases are then forecast in the years to June 2024 and December 2024.

“Labour market spare capacity remains around multi-decade lows. Labour underutilisation…is expected to gradually increase as a result of subdued economic growth over coming years; the unemployment rate is nonetheless expected to remain below pre-pandemic levels.”

The headline inflation forecast for the current financial year has been lowered by 0.50 percentage points and the forecast for the year to December 2023 has been reduced by 0.25 percentage points.

“Consumer price inflation in Australia eased in the March quarter, confirming that inflation has passed its peak. Goods price disinflation has driven most of the moderation in inflation outcomes in early 2023, consistent with but a little later than the experience overseas. Nonetheless, inflation remains high and broadly based and services inflation continues to pick up.”

Commonwealth Government bond yields slipped at the short end while longer-term yield rose modestly. By the close of business, the 3-year ACGB yield had lost 2bps to 2.94% while 10-year and 20-year yields both finished 1bp higher at 3.32% and 3.80% respectively.

In the cash futures market, expectations regarding rate cuts in 2024 firmed. At the end of the day, contracts implied the cash rate would remain essentially steady at the current rate of 3.82% to average 3.83% in June and 3.85% in July. February 2024 contracts implied a 3.54% average cash rate while May 2024 contracts implied 3.35%.

“So, the key theme in the SOMP is the risks around the inflation outlook given the evidence both domestically and offshore that services inflation is slow to fall,” said Westpac Chief Economist Bill Evans. “That can be explained by the ongoing tightness of the labour market holding up wages growth and poor productivity in the market services sector which is boosting unit labour costs.”