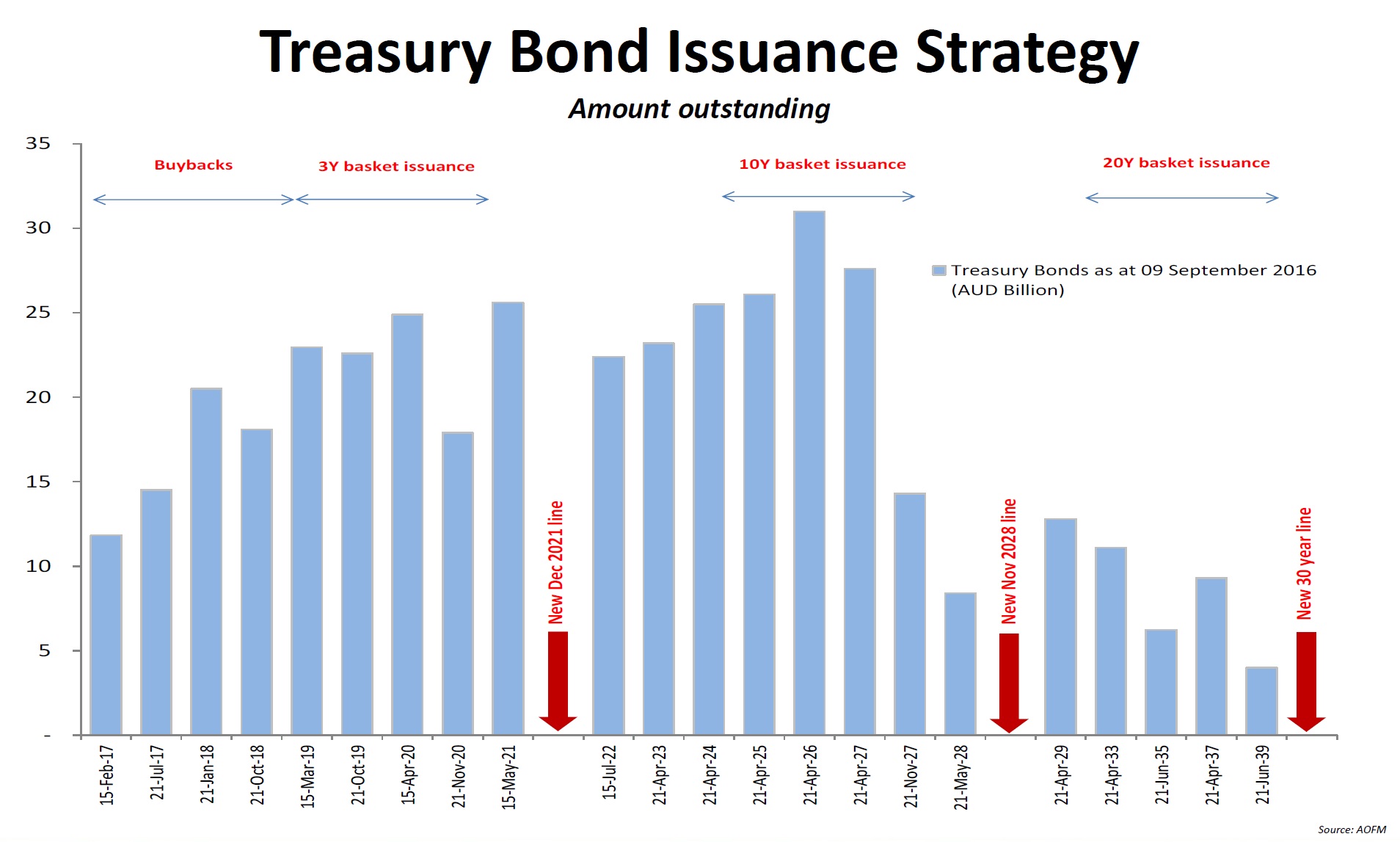

The much talked-about Australian 30 year bond is finally about to become reality. The chief of the Australian Office of Financial Management, Rob Nicholl gave a speech at an Australian Business Economists lunch in Sydney where he covered the Commonwealth’s issuance strategy for the 2016/2017 year. In the speech he had a few things to say about the likely timing for issuance of a 30 year bond, as well as other matters relating both short and long term bond issuance.

The inaugural issue of Australia’s first sovereign 30 year bond will come shortly as the AOFM thinks “…the time is right for this to proceed. We are planning, subject to market conditions, to do this around the second week of October.” It will be via a syndicated offer and it will be a “meaningful volume to meet anticipated broad interest and to establish a maturity of clear benchmark size.”

A 30 year bond would be welcomed by insurance companies and banks with long-term liabilities and assets such as life policies and mortgages. A government 30 year bond creates a pricing benchmark by which other products’ pricing can be reliably set.

The global search for a yield, a term the AOFM chief used in his speech and one seen frequently this year in investment house research, has made the AOFM confident of investor support and the timing is right for the AOFM to seek to extend the yield curve by 7 years. “We are confident that domestic investor support and the so-called ‘global search for yield’ that has underpinned an increased demand for duration will remain sufficient for us to establish a 30-year Australian yield curve.” New 30 year bonds would be issued “every four years, or in the event that sufficient strong interest builds for these maturities another option may be to consider repeating a new issue every second year.”

The day of the speech was one in which bond yields rose and Westpac suggested the announcement of a benchmark-sized 30 year bond had some bearing on the market that day. “While that announcement was probably not a surprise, what did impact markets was that the AOFM wants this to be a “benchmark” size immediately, which takes the expected issuance from $3-4bn to the $5-7bn range.” The announcement has most likely impacted the steepness of the yield curve with investors selling longer dated bonds in advance of the new issue. The yield curve has been steepening in any case due to global ructions associated with the US Fed’s desire to raise interest rates so it isn’t possible to blame this move fully on the AOFM’s plans.

Related Articles : Aust 30y bond back on radar